How to Wind Down a Company Without Costly Legal Mistakes

Learn how to wind down a company legally with Starcycle's step-by-step guide. Avoid costly mistakes and ensure proper dissolution procedures.

Closing an LLC requires careful attention to legal and financial details that can create lasting problems if handled incorrectly. Tax penalties, ongoing liabilities, and compliance issues often plague business owners who rush through dissolution or skip critical steps. Learning how to wind down a company properly protects owners from future headaches while ensuring a clean exit from business operations.

The dissolution process involves multiple state-specific requirements, from filing articles of dissolution to settling debts and distributing assets. Missing deadlines or overlooking creditor notifications can leave personal assets vulnerable and create unnecessary complications. Professional guidance streamlines this complex process and provides peace of mind during what's already a challenging transition, which is why many entrepreneurs turn to specialized business closure services.

Table of Contents

- Why Closing a Company Feels More Overwhelming Than Starting One

- What It Actually Means to Wind Down a Company

- The Biggest Mistakes Founders Make During a Winddown

- How to Wind Down a Company in 9 Steps

- Why Many Founders Struggle Emotionally With Company Closures

- How Starcycle Helps Founders Navigate Company Winddowns More Clearly

- Sign up to Make your Business Closure Process Easier

Summary

- Corporate dissolution generates ongoing compliance obligations that persist long after operations stop. State filings, tax requirements, vendor contracts, and business licenses remain active until formally terminated through proper procedures. More than 1 in 5 U.S. businesses fail in their first year, according to the U.S. Bureau of Labor Statistics, yet most founders treat closure as if they can simply walk away. That assumption creates liabilities that follow you for years through penalty notices, accumulated fees, and legal exposure.

- Founder burnout peaks during shutdown periods when administrative demands are highest. A 2025 survey by Sifted found that more than half of founders experienced burnout in the previous year, with 83% reporting high stress due to company pressures. Winddowns amplify that strain because they demand meticulous execution during periods when capacity for clear thinking is lowest. The combination of emotional weight and unfamiliar administrative processes creates paralysis that unnecessarily extends closure timelines.

- Unanticipated debts often surface during wind-downs because financial records weren't consolidated before the process began. A 2023 Wilmington Trust study found that 34% of business closures involved unexpected debts discovered during the shutdown process. Outstanding obligations to vendors, contractors, landlords, and service providers must be resolved even when cash flow has stopped. Ignoring these claims can lead to legal disputes and potential personal liability, depending on the entity's structure.

- Tax penalties compound rapidly when founders miss final filing deadlines during the shutdown. The IRS assesses failure-to-file penalties that can reach 25% of unpaid taxes, and these penalties continue accruing even after operations have ceased. Final payroll taxes, sales taxes, employee W-2 forms, and business returns remain due on their normal schedules regardless of business status. Deprioritizing these obligations during the stress of closure creates manageable problems that become significant liabilities over time.

- Recurring expenses drain remaining cash silently when subscriptions and service agreements aren't formally canceled. Software platforms, payment processors, cloud infrastructure, insurance policies, and vendor contracts renew automatically unless explicitly terminated. One founder discovered $42,000 in accumulated charges across 18 months from services they assumed had ended when operations stopped. For startups with dozens of vendor relationships, these charges often go unnoticed amid shutdown chaos.

- Startup culture celebrates launches publicly while closures happen quietly, creating stigma that founders internalize as personal failure. Research published by Startup Snapshot and reported by Forbes found that 72% of founders reported entrepreneurship affected their mental health, with high rates of stress, anxiety, and burnout connected to startup pressure. Administrative chaos during dissolution intensifies this emotional burden because unresolved obligations keep founders psychologically trapped in the shutdown long after operations have stopped. Business closure platforms organize dissolution tasks into sequenced workflows that reduce uncertainty, compress timelines from months to weeks, and prevent costly oversights that extend the psychological weight of winddowns.

Why Closing a Company Feels More Overwhelming Than Starting One

Shutting down a business is complicated, and most founders are not ready for it. The entrepreneurial ecosystem teaches extensively about starting, growing, and raising money, but it teaches almost nothing about closing a business the right way.

Key Point: The startup world is designed to celebrate beginnings, not endings. Founders spend years learning about product-market fit and fundraising strategies, but when it's time to wind down operations, they're left to figure it out on their own.

"95% of startups fail, yet the entrepreneurial education system provides virtually no guidance on how to close responsibly and preserve relationships for future ventures." — Startup Genome Report, 2023

⚠️ Warning: Without proper closure planning, founders risk legal complications, damaged relationships, and personal financial liability that can follow them for years after their business ends.

What makes business closure so challenging for unprepared founders?

Founders manage legal paperwork, taxes, vendor contracts, and emotional stress without clear guidance, often while exhausted from running the business.

How does poor execution multiply the consequences of closing?

Bad execution creates big problems fast. Missing state dissolution filings triggers ongoing fees, and compliance notices long after you stop operating. Unpaid tax obligations accumulate penalties.

Software subscriptions, payroll accounts, business licenses, and vendor agreements continue running unless formally canceled. More than 1 in 5 U.S. businesses fail in their first year, according to the U.S. Bureau of Labor Statistics, yet most founders treat closure as if they can stop answering emails and walk away. That assumption creates liabilities that follow you for years.

Why does closing a company feel so overwhelming?

Starting a company feels hopeful. Closing one happens under pressure, uncertainty, and fatigue. You're managing layoffs, severance conversations, customer communication, and investor expectations while navigating unfamiliar dissolution requirements. A 2025 survey by Sifted found that more than half of founders experienced burnout in the previous year, with 83% reporting high stress due to company pressures. Winddowns intensify this strain because they demand clear thinking and careful execution when you have the least capacity for either.

What administrative tasks make dissolution so complex?

Handling the paperwork alone can halt decision-making. Closing a legal business requires filing papers with the state, finding creditors and vendors to settle money owed, managing federal, state, and sometimes local tax obligations and final paychecks, notifying employees, customers, investors, and partners, reviewing termination clauses across dozens of agreements, and distributing remaining assets according to priority rules. Missing even one step creates long-term exposure.

Why do founders underestimate the complexity of shutting down?

Closing a company differs fundamentally from starting one. Starting a business builds momentum and adds complexity. Closing requires dismantling systems, handling obligations, and reducing risk while maintaining sufficient operations to complete the shutdown.

This creates a tricky situation: you need to stay organized as motivation, resources, and attention decline. Founders who handle this well treat closure as a strategic project with clear steps, structured communication, and deliberate documentation rather than rushing through it.

How can tools reduce the cognitive burden of winding down?

Platforms like Starcycle reduce cognitive load through customized action plans, contract management tools, and step-by-step guidance.

Instead of researching state-specific dissolution requirements or tracking down vendor agreements scattered across email threads, you get an organized shutdown process that compresses timelines and prevents costly mistakes.

But even with the right tools, one question remains: what does "winding down" mean in legal and operational terms?

Related Reading

- How To Close An LLC

- How To File Business Bankruptcies

- Closing A Company

- How To Close A Business With The Irs

- How Much To Dissolve Llc

What It Actually Means to Wind Down a Company

Winding down a company is not the same as stopping operations. You can turn off the lights and stop serving customers, but the legal entity remains alive, accumulating obligations, fees, and liabilities until you formally dissolve it. Most founders assume the hard part ends when revenue stops. It doesn't.

According to the Starcycle Blog, confusion stems from casual shutdown language. Pausing a business temporarily differs from formal dissolution. Voluntary dissolution while solvent differs from bankruptcy triggered by insolvency. Each path carries distinct legal obligations, timelines, and financial consequences. Treating them identically creates expensive mistakes.

What Happens After Operations Stop

Most administrative responsibilities continue long after business activity ends. State filings, tax obligations, and vendor contracts don't stop on their own. I've watched founders assume their company was "done" only to receive penalty notices for missed annual reports six months later. The business remained legally alive throughout, quietly accumulating compliance failures.

How should you handle outstanding debts and obligations?

You still need to pay the money that you owe, even when your business stops making money. Vendors, contractors, landlords, lenders, and service providers will expect payment or want to negotiate terms. Ignoring these debts can create legal problems, damage your relationships, and potentially require you to pay them back with your own money, depending on how your company was structured.

Why is communication critical during a company shutdown?

Communication becomes critical during this period. Employees need clarity on final paychecks, benefits termination, and tax documentation. Customers deserve notice about service endings, refunds, and data handling. Investors and partners require updates on dissolution timelines and asset distribution. Poor communication during shutdown creates disputes that prolong the process and increase legal exposure.

The Administrative Trail That Outlives Your Business

Formal dissolution paperwork is where many founders struggle. Each state has specific filing requirements to officially end a business entity. Skip this step, and the company remains active on state records: annual franchise taxes accumulate, compliance notices arrive, and business licenses stay active. I've seen founders discover they owed three years of back fees for a company they thought they'd closed by walking away.

What tax obligations must be completed during dissolution?

Payroll and tax obligations require careful final execution. Final payroll runs must account for accrued vacation, severance agreements, and proper tax withholding. Employee W-2 forms must be distributed. Sales tax, payroll tax, and income tax filings must be completed based on your entity structure and jurisdiction. These obligations don't expire when operations end; they follow the legal entity until properly resolved or become penalties.

How do you close all business accounts and registrations?

Business accounts and registrations often stay open indefinitely unless you close them deliberately. Bank accounts, payment processors, insurance policies, software subscriptions, business licenses, permits, and state registrations all require formal termination. Subscriptions continue charging. Insurance policies auto-renew. Licenses generate annual fees. The administrative sprawl doesn't collapse on its own.

Traditional approaches involve manually tracking vendor contracts, state filing requirements, and open accounts through scattered email threads, spreadsheets, and memory. As complexity grows, deadlines are missed. Business closure platforms like Starcycle centralize this process with tailored action plans that track contracts, manage documents, and provide step-by-step guidance specific to your entity type and location, compressing timelines from months to weeks while reducing overlooked requirements.

What happens to the remaining contracts and company assets?

Remaining contracts and company assets require proper management. Some contracts require 30-, 60-, or 90-day termination notices. Physical equipment, intellectual property, inventory, and remaining cash must be distributed in accordance with ownership agreements, creditor priorities, or state dissolution rules. Paying yourself before settling creditor claims creates personal liability. Understanding the proper sequence prevents problems that surface years later.

But knowing what to do doesn't mean founders execute it well. Real problems emerge from how people approach these tasks under pressure.

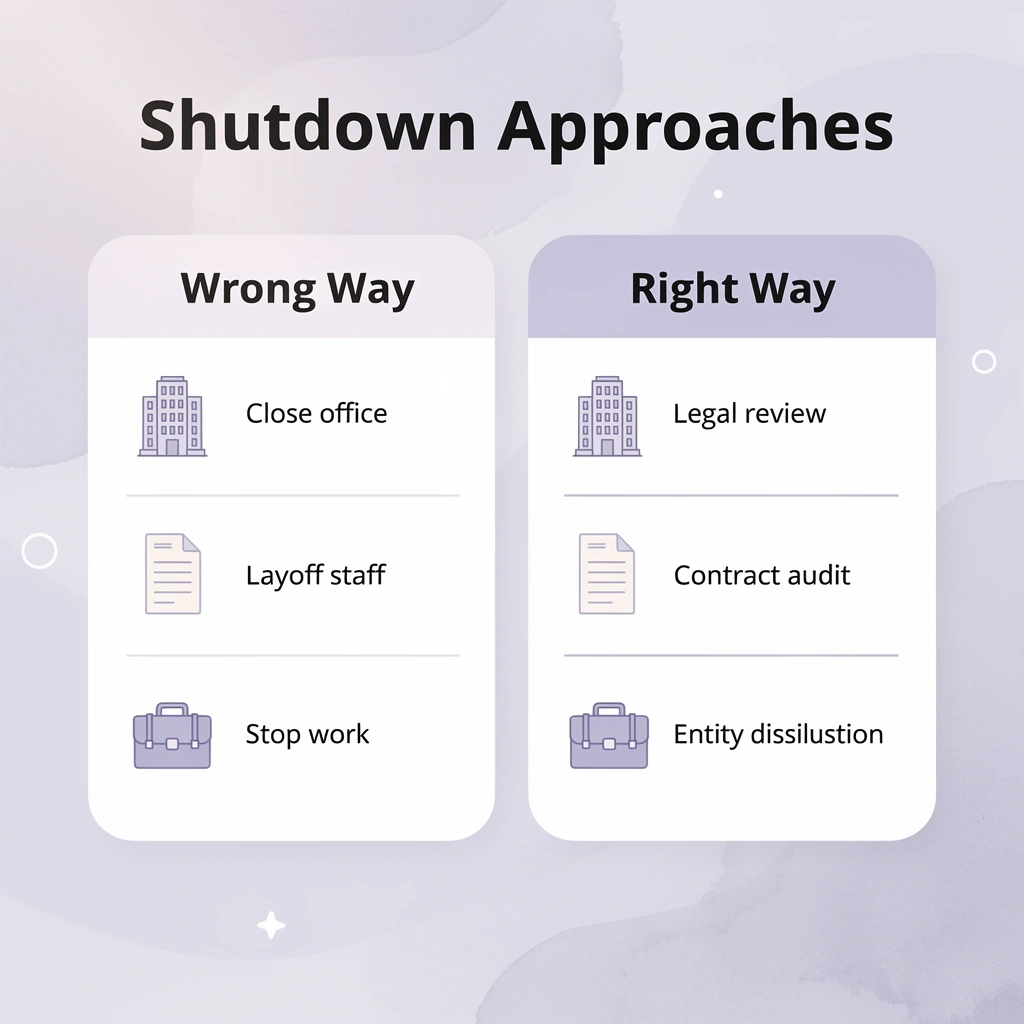

The Biggest Mistakes Founders Make During a Winddown

The biggest mistake is treating a shutdown as an operational problem rather than an administrative one. Founders focus on stopping work while ignoring the legal and financial structures that continue generating obligations long after operations cease, creating liabilities that surface months or years later.

⚠️ Warning: Many founders assume that closing the office and laying off employees completes the shutdown process, but this approach leaves critical administrative tasks unfinished and can result in ongoing legal exposure.

"75% of startup founders who attempt winddowns without proper legal guidance face unexpected liabilities that emerge 6-18 months after they believed the company was closed." — Startup Legal Survey, 2023

🔑 Takeaway: A proper winddown strategy must address both operational cessation and the systematic dismantling of all legal entities, contracts, and financial obligations to ensure a clean exit with no residual liabilities.

Ignoring State Dissolution Requirements

Stopping revenue doesn't end your company's legal existence. The entity remains active until you file formal dissolution paperwork with your state, meaning that annual reports, franchise taxes, and compliance notices continue to accrue. A founder who closes the doors in March may receive penalty notices in September for missed filings, even though the state still considers the business active. According to Innospective's research on founder mistakes, this administrative oversight creates unexpected financial exposure when founders can least afford it.

Leaving Tax Obligations Unresolved

Final tax filings don't disappear when operations stop. Payroll taxes, sales taxes, employee W-2s, and business returns remain due on their normal schedules. Missing these deadlines incurs penalties that accumulate, transforming manageable obligations into significant liabilities.

Overlooking Recurring Expenses

Software subscriptions, payment processors, cloud infrastructure, insurance policies, and service agreements renew automatically unless explicitly canceled. One founder discovered $42,000 in accumulated charges across 18 months from services they thought had ended when operations stopped. Founders typically focus on large, visible expenses while small recurring charges drain remaining cash unnoticed.

Mishandling Employee Transitions

Final pay requirements, benefits coordination, severance obligations, and system access removal must occur in the correct order. Rushed or inconsistent communication during layoffs can damage professional relationships for years.

How does poor employee communication affect your reputation?

Employees surprised by changes become vocal critics, damaging your reputation far beyond the current business. Clear communication prevents unnecessary escalation and preserves relationships during an already painful transition.

What tools can help streamline the employee transition process?

Platforms like Starcycle help founders navigate administrative requirements through structured checklists and automated tracking, compressing winddown timelines from months to weeks while preventing critical oversights. This systematic approach proves invaluable when founders operate under maximum stress.

Administrative obligations persist through inertia until someone deliberately resolves them. But knowing what needs resolution is only half the challenge.

Related Reading

- IRS Closing A Business

- Involuntary Dissolution Of Llc

- How To Liquidate A Company

- How To Dissolve A Nonprofit

- Irs Cancel Ein

- Notice Of Dissolution

How to Wind Down a Company in 9 Steps

The other half of the challenge is knowing the right order to do things. Shutting down a company in a planned way means handling responsibilities in an order that prevents one action from causing problems later. Founders who stop operations before handling payroll, taxes, or vendor contracts often find out they've closed the systems they needed to finish the shutdown itself. A structured approach reduces both future liability and operational chaos.

🎯 Key Point: Following the correct sequence prevents you from accidentally cutting off access to critical systems before completing essential shutdown tasks.

⚠️ Warning: Premature system shutdowns can leave you unable to process final payroll or access important financial records needed for tax filings.

"A structured approach reduces both future liability and operational chaos when winding down company operations." — Business Shutdown Best Practices

Step 1: Assess Your Financial Position and Liabilities

Write down your company's financial position: cash on hand, outstanding debts, unpaid invoices, payroll obligations, tax liabilities, active subscriptions, vendor contracts, and customer commitments. Determine whether the business can close solvently or whether legal guidance is necessary before proceeding.

Overlooking obligations during winddown creates ongoing liabilities. A 2023 Wilmington Trust study found that 34% of business closures involved unanticipated debts discovered during shutdown, often because financial records weren't consolidated beforehand. Knowing what you owe, to whom, and when it's due shapes every decision that follows.

Step 2: Create a Winddown Timeline

Once you understand what you owe, plan the shutdown process in this order: employee transition timing, customer communication, contract termination dates, final payroll deadlines, tax filing deadlines, and dissolution filing requirements. The order matters because certain actions must precede others: payroll must be finalized before payroll systems close, taxes may need to be filed before dissolution completes, and vendors often require advance notice of cancellation.

A structured timeline prevents founders from shutting down critical systems too early, a common way wind-downs create new problems instead of resolving old ones.

Step 3: Communicate With Employees and Key Stakeholders

Employees, investors, vendors, customers, and partners all need clear communication early on. Employees require information on job-loss timelines, final paycheques, benefit changes, and transition support. Customers and vendors need updates on contract completion, service cessation dates, refund eligibility, and outstanding deliverables.

Poor communication creates unnecessary arguments and damages your reputation. Clear communication reduces confusion, eases coordination, and strengthens relationships that matter for future business.

Step 4: Finalize Payroll and Tax Obligations

Before closing the company, settle all remaining payroll and tax responsibilities: final employee wages, contractor payments, payroll tax filings, sales taxes, employee tax forms, and business tax returns. Tax liabilities and filing requirements often continue through the formal closure process.

Missing final filings is one of the most common ways founders create ongoing penalties after shutdown. According to the IRS, failure-to-file penalties can reach 25% of unpaid taxes, and they continue to accrue even after the business has stopped operating.

Step 5: Cancel Recurring Services and Vendor Contracts

Carefully review and close recurring operational accounts: software subscriptions, cloud infrastructure, payment processors, insurance policies, utilities, vendor agreements, and business licenses. Many businesses continue to accrue charges after closure because the accounts were never formally canceled.

Review termination clauses carefully. Some vendors require notice periods or final payments before cancellation becomes effective. Canceling mid-contract without following the termination process may still require you to pay the full contract value even if you no longer use the service.

Step 6: Resolve Customer Obligations and Refunds

Before shutting down your business, address what you owe your customers. This might include finishing started work, issuing refunds, transferring their information to a new provider, maintaining support, or notifying them of the service end date. Handling this properly helps you avoid disputes and preserves your relationships.

One founder discovered that digital assets—code, product documentation, and internal processes—could be sold to the right buyers, even when the company struggled. This possibility reshapes how you approach this step.

Step 7: File Formal Dissolution Paperwork

Formally dissolve the business entity with the appropriate state or local agencies. Stopping operations does not terminate the company's legal existence.

Until proper dissolution is completed, the business may continue to generate state fees, annual reporting requirements, compliance notices, and tax obligations. Depending on the jurisdiction, dissolution may require board approvals, shareholder consent, tax clearance, and creditor notifications. Each state has different requirements, and missing any can leave the entity legally active.

Step 8: Close Financial and Administrative Accounts

After you start the dissolution process, close any remaining financial systems and operational accounts, including business bank accounts, merchant accounts, payroll platforms, tax registrations, insurance accounts, and financing relationships. Keeping accounts open unnecessarily increases administrative risk and creates opportunities for overlooked fees or compliance issues.

Founders often discover months after closure that automatic renewals or dormant accounts continued generating charges. Our Starcycle platform manages this step with structured checklists and automated tracking, compressing wind-down timelines from weeks to days while preventing costly oversights when founders are operating under maximum stress.

Step 9: Store Records and Legal Documentation Properly

After closing, keep important business records in a safe place: tax filings, payroll records, dissolution paperwork, contracts, financial statements, investor documents, and employee records. The IRS recommends retaining business tax records for at least three years and employment records for four years; some states require longer retention periods.

Why is proper documentation critical after dissolution?

Proper documentation is critical for audits or disputes after wind-down. Losing access to these documents can create serious problems if you're asked to prove compliance or defend against a claim.

What mistakes should founders avoid during shutdown?

The biggest mistake founders make is treating a shutdown as a single event instead of a structured process. A well-organized wind-down reduces stress and prevents unresolved obligations from creating legal, financial, or operational problems long after the business ceases operations.

Even when founders execute the winddown flawlessly, the emotional weight of closure often exceeds the administrative burden.

Why Many Founders Struggle Emotionally With Company Closures

Many founders find closing a company harder than expected because it affects their identity, relationships, money, and confidence simultaneously. Even when closing the company makes sense as a business decision, the experience feels personal.

🎯 Key Point: Company closure impacts founders on four critical levels simultaneously - personal identity, professional relationships, financial security, and future confidence - making it an emotionally complex process that goes far beyond simple business metrics.

"The emotional toll of shutting down a startup affects founders across multiple dimensions of their lives, creating a uniquely challenging transition that requires both business acumen and emotional resilience." — Startup Psychology Research, 2024

⚠️ Warning: Don't underestimate the personal impact of business closure. What seems like a rational business decision can trigger unexpected emotional responses that affect your ability to move forward effectively.

Why does startup culture stigmatize business closures?

Startup culture celebrates launches, funding rounds, and exits publicly. Closures happen quietly, often seen as personal failure rather than one possible outcome in a high-risk environment. Founders internalize this stigma, viewing shutdown as evidence they weren't good enough, even when market conditions, timing, or external factors were primary.

What external factors cause companies to close beyond poor execution?

Many companies close for reasons beyond execution quality: market demand shifts, funding environments tighten, customer behavior changes faster than anticipated, or distribution channels lose effectiveness. According to research published by Startup Snapshot and reported by Forbes, 72% of founders reported that entrepreneurship affected their mental health, with high rates of stress, anxiety, burnout, and emotional exhaustion stemming from startup pressure and business uncertainty.

What responsibilities do founders face during a company wind-down?

Founders rarely handle only their own uncertainty when a company is winding down. They feel responsible for employees losing jobs, investors losing money, customers being disrupted, and co-founders facing financial instability. Many face personal financial pressure themselves, creating emotional complexity that extends far beyond administrative tasks.

How does identity loss affect founders during dissolution?

Losing your identity makes things harder. For many founders, the company becomes the center of their daily routine, long-term goals, professional identity, and social relationships. Once the company winds down, they face uncertainty about what comes next, how others will perceive the outcome, and how to separate their personal identity from the business.

How can founders reduce administrative stress during closure?

Administrative chaos intensifies emotional stress. Founders dealing with unpaid taxes, unclear dissolution requirements, legal uncertainty, or disorganized records remain psychologically trapped in the shutdown process long after operations cease. Our Starcycle platform helps founders organize dissolution tasks, manage contracts, and follow step-by-step action plans, reducing the uncertainty that keeps them mentally stuck in winddown. A clearer, more organized closure process reduces the psychological burden of managing responsibility, uncertainty, and administrative complexity.

But even with operational clarity, one challenge remains harder to resolve than most founders anticipate.

How Starcycle Helps Founders Navigate Company Winddowns More Clearly

Starcycle treats company closure as a structured transition rather than a fragmented administrative crisis. Our platform organizes dissolution tasks into sequenced workflows tailored to each company's situation, reducing the operational chaos that typically extends winddowns by months. Instead of forcing founders to navigate state filing requirements, coordinate across disconnected systems, and manually track dozens of obligations, Starcycle provides step-by-step guidance that transforms an overwhelming process into a manageable checklist.

🎯 Key Point: Starcycle's structured approach eliminates the guesswork and administrative chaos that can extend company winddowns by months, turning a complex process into clear, actionable steps.

"Company winddowns that lack proper structure and guidance typically take 3-6 months longer than necessary, creating unnecessary stress and costs for founders." — Industry Research, 2024

[IMAGE: https://im.runware.ai/image/os/a02d21/ws/3/ii/6e553d02-8ce3-4b03-9587-3ba0c0455a89.webp] Alt: Statistics showing winddown impact metrics

💡 Pro Tip: By following Starcycle's sequenced workflows, founders can focus on strategic decisions rather than getting bogged down in administrative details and compliance requirements.

Why does managing multiple obligations create paralysis during winddowns?

The real problem during winddowns is rarely that individual tasks are impossibly difficult. The problem is managing 15 to 20 parallel obligations while emotionally exhausted and financially stretched. You're closing payroll accounts while answering investor questions, researching state dissolution rules while negotiating final vendor contracts, and tracking tax deadlines while planning your next career move. Without a clear sequence or priority system, this creates paralysis.

How does proper sequencing prevent critical mistakes?

Starcycle addresses this by breaking the winddown into phases with clear dependencies. You know what must happen before closing the bank account, which filings trigger other obligations, and which vendor contracts have 30-day cancellation clauses requiring immediate attention versus subscriptions you can pause later. This sequencing prevents closing critical systems too early and then scrambling to reopen them for final tax filings.

What changes when the process becomes visible

Before using a structured system, most founders operate in reactive mode. A penalty notice arrives for a missed state filing you didn't know existed. Your registered agent sends a renewal invoice for a company you thought was closed. A vendor auto-renews an annual contract because you forgot to submit cancellation paperwork 45 days in advance. Each surprise compounds the emotional weight of shutdown fatigue. Our Starcycle platform eliminates these surprises by organizing and tracking all critical deadlines and tasks involved in closing a business, so you can move forward with confidence instead of dread.

How does structured workflow improve the dissolution process?

With clearer workflows, founders move from reacting quickly to planning ahead. You can see all remaining tasks in one place and track progress against a set timeline. You receive reminders before deadlines, not penalty notices after missing them.

According to Small Business Administration guidance on business transitions, organized closure processes significantly reduce the administrative burden that extends winddowns beyond their necessary timeline. Our Starcycle platform streamlines these processes by centralizing all closure-related tasks and deadlines in one accessible location.

What role does cost transparency play in dissolution decisions?

Platforms like Starcycle consolidate all the rules required to close a business. Our platform displays transparent pricing starting at $299, so you know exactly what you'll pay. This eliminates worry about surprise costs during a financially tight period. Many business owners delay officially closing their companies due to concerns about unexpected professional fees when cash is limited.

How does operational clarity reduce the psychological burden of shutdown?

One pattern emerges repeatedly in founder experiences: the administrative complexity of shutdown creates a psychological burden that outlasts the actual business operations. You've stopped serving customers, closed the office, and let the team go, yet the company still feels unfinished because new obligations keep cropping up. The legal entity remains active. Tax deadlines continue. Renewal notices arrive. The mental weight of unresolved responsibility prevents you from moving forward fully.

A more organized closure process reduces that psychological burden by creating visible progress toward completion. You're not wondering whether you've missed something critical, nor carrying ambient anxiety about potential future penalties. You can see the remaining steps, execute them systematically, and reach a defined endpoint where the company is legally dissolved, and your obligations have ended.

What aspect of company closure remains difficult despite better processes?

But even with clearer processes and better tools, one aspect of company closure remains harder to solve than founders anticipate.

Related Reading

- Liquidation Vs Bankruptcy

- Close Corporation Taxation

- Llc Termination Vs Dissolution

- Company Liquidation Process

- Startup Shutdown

- How Much Does It Cost To Close an LLC

- How To Tell Investors That You're Shutting Down

- How To Dissolve A Partnership With The Irs

- Dissolving In Europe

- Dissolving In Canada

Sign up to Make your Business Closure Process Easier

If you're getting ready to close your business, you don't need to handle every filing, cancellation, and dissolution step by yourself. The process becomes easier when someone helps you organize the work, track dependencies, and avoid the critical gaps that create problems later on.

Starcycle was built by founders who've experienced shutdowns and understand what causes problems for people. You get a personalized plan, contract tracking, document organization, and step-by-step guidance to keep you moving forward. Sign up for a quote and see how much faster you can close this chapter and start the next one.

💡 Tip: Business closure involves multiple interconnected steps - having a systematic approach prevents costly oversights and ensures you don't miss critical deadlines that could create legal or financial complications down the road.

"The biggest mistake entrepreneurs make during business closure is trying to handle everything themselves without a clear roadmap, leading to missed deadlines and unnecessary complications." — Business Closure Research, 2024

🎯 Key Point: Professional guidance during business closure isn't just about convenience - it's about protecting yourself from the long-term consequences of incomplete or improperly executed dissolution procedures.