Closing a Company: A Step‑By‑Step Guide to Shutting Down Legally

Closing a company legally? Polsia's step-by-step guide covers the requirements, paperwork, and deadlines for a proper shutdown.

Closing an LLC requires more than simply stopping operations and walking away. Proper dissolution protects business owners from ongoing tax obligations, legal complications, and personal liability issues that can persist for years after shutting down.

The dissolution process involves filing official paperwork, settling outstanding debts, notifying creditors and tax authorities, and completing various state-specific requirements. Business owners who handle these steps correctly can move forward confidently, knowing their personal assets remain protected and all legal obligations have been satisfied through proper business closure.

Table of Contents

- Why Closing A Company Is Harder Than Starting One

- What Closing A Company Actually Involves

- Where Company Closures Break Down

- How To Close A Company in 6 Steps

- What A Clean Company Closure Should Achieve

- How Starcycle Helps You Close A Company With Clarity

- Sign up to Make your Business Closure Process Easier

Summary

- Starting a company requires optimism and forward momentum, but closing one demands precision during the worst possible time for decision-making. The structural difference is significant. Launching means moving forward with incomplete information, while shutting down means accounting for every obligation created along the way. According to LendingTree, 22.1% of new US businesses close within a year, and research from Clearly Payments shows that half fail within five years. That means millions of founders navigate this process, yet most resources still focus on growth rather than shutdown.

- The assumption that closure is straightforward because operations have stopped creates the most common failure point. Stopping work and legally dissolving a company are entirely separate processes. You still have creditors expecting payment, contracts requiring formal termination, tax filings to complete, and state requirements to satisfy. A 2023 Deloitte study found that 34% of dissolved businesses faced post-closure penalties due to incomplete filings. The system doesn't assume you're done until you provide formal documentation.

- Incomplete financial visibility causes most closures to unravel midway through the process. Founders often lack a consolidated view of what the company owes and to whom, with contracts, vendor balances, taxes, and contingent obligations scattered across systems and documents. Without a complete picture, liabilities are missed or handled out of order, creating disputes and follow-up claims later. What looked resolved on the surface remains legally active.

- Filing sequence determines whether the closure stays clean or becomes contested. You cannot dissolve a company that still owes money without exposing yourself to claims that follow you personally. Pay what the business owes in the correct order (taxes, employee wages, and secured debts typically come first), notify stakeholders within required timelines, then submit dissolution paperwork. According to the National Federation of Independent Business, 41% of dissolved businesses faced post-closure penalties in 2022 due to incomplete filings, with missed final tax returns and failure to cancel state registrations being the most common errors.

- Personal liability exposure increases when compliance steps are missed or handled in the wrong order. If personal guarantees were signed or filings are incomplete, creditors may pursue claims beyond the business itself. The boundary between the company and the founder only holds if you honor it through proper process. Skip a filing, miss a notice period, or leave a tax return incomplete, and the shield dissolves, making personal assets fair game for unresolved business obligations.

- Starcycle's business closure service addresses this by organizing obligations, filings, and stakeholder notifications into a sequenced action plan that prevents fragmented execution and missed deadlines, which trigger post-closure penalties and legal exposure.

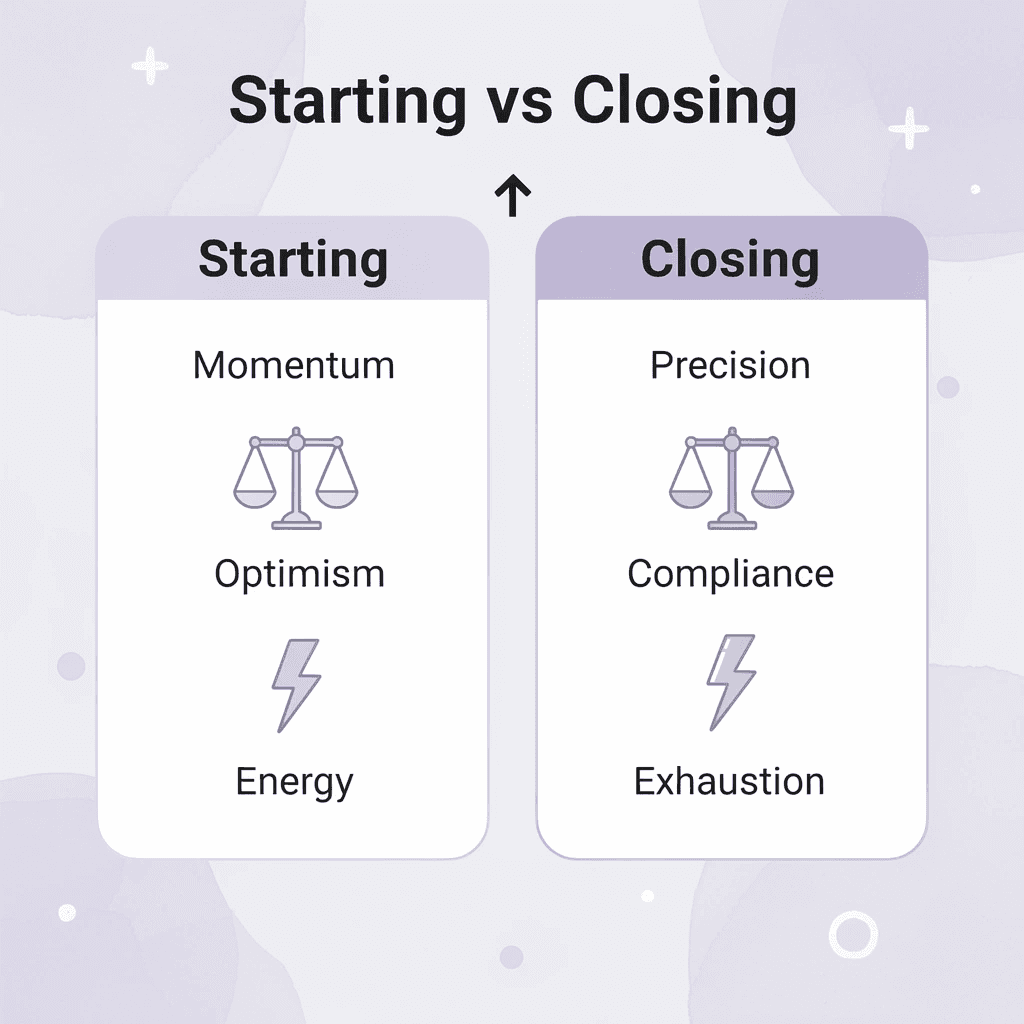

Why Closing A Company Is Harder Than Starting One

Starting a company requires momentum and optimism. Closing one requires precision, compliance, and risk management while exhausted. Launching means moving forward with incomplete information. Shutting down means accounting for every obligation you created.

🎯 Key Point: The emotional and administrative burden of closing a business is significantly higher than starting one, as you must handle complex legal requirements while dealing with the stress of business failure.

⚠️ Warning: Many entrepreneurs underestimate the time and resources required for proper business closure, leading to potential legal complications and personal liability issues down the road.

What makes company closure legally complex?

Most founders assume closure is straightforward because operations have stopped. But stopping work and legally dissolving a company are two completely different things. You still have creditors expecting payment, contracts requiring formal termination, tax filings to complete, and state requirements to satisfy. Miss one filing, and the company remains legally active. Leave a liability unresolved, and creditors can pursue claims beyond the business itself.

Why do so many businesses struggle with proper shutdown?

According to LendingTree, 22.1% of new US businesses close within a year, and research from Clearly Payments shows that half fail within five years. Yet most resources focus on growth rather than shutdown, leaving founders to gather information from multiple sources while avoiding costly mistakes.

The risk compounds when you're already under pressure

Closure happens during the worst possible time for decision-making. Financial pressure is high. Emotional fatigue sets in. The clarity you had when starting the company is gone. In that state, it becomes harder to be precise with details while managing the stress of what closing means for your future.

Why doesn't a single checklist work for every business closure?

The complexity spreads across multiple disconnected systems: state dissolution filings, federal tax clearances, employee final payments, lease terminations, and vendor settlements. Each has different requirements and deadlines. No single checklist works for every business because obligations vary by state, industry, and company structure. What works for an LLC in Delaware doesn't apply to an S-Corp in California.

Platforms like Starcycle solve this problem by creating customized action plans tailored to your specific business structure and obligations, and by coordinating filings, contracts, and compliance requirements, so founders need not become experts in dissolution law. Rather than searching across state websites and legal forums, you get a clear path tailored to your situation.

What surprises most founders about the closure process?

Most founders don't realize the complexity involved until they're in the middle of it, discovering that what looked simple is a web of interconnected obligations, each with real consequences if handled incorrectly.

Related Reading

- How To Close An LLC

- How To File Business Bankruptcies

- How Much To Dissolve an LLC

- How To Close A Business with the IRS

- IRS Closing A Business

- How To Dissolve A Corporation

- Involuntary Dissolution Of Llc

What Closing A Company Actually Involves

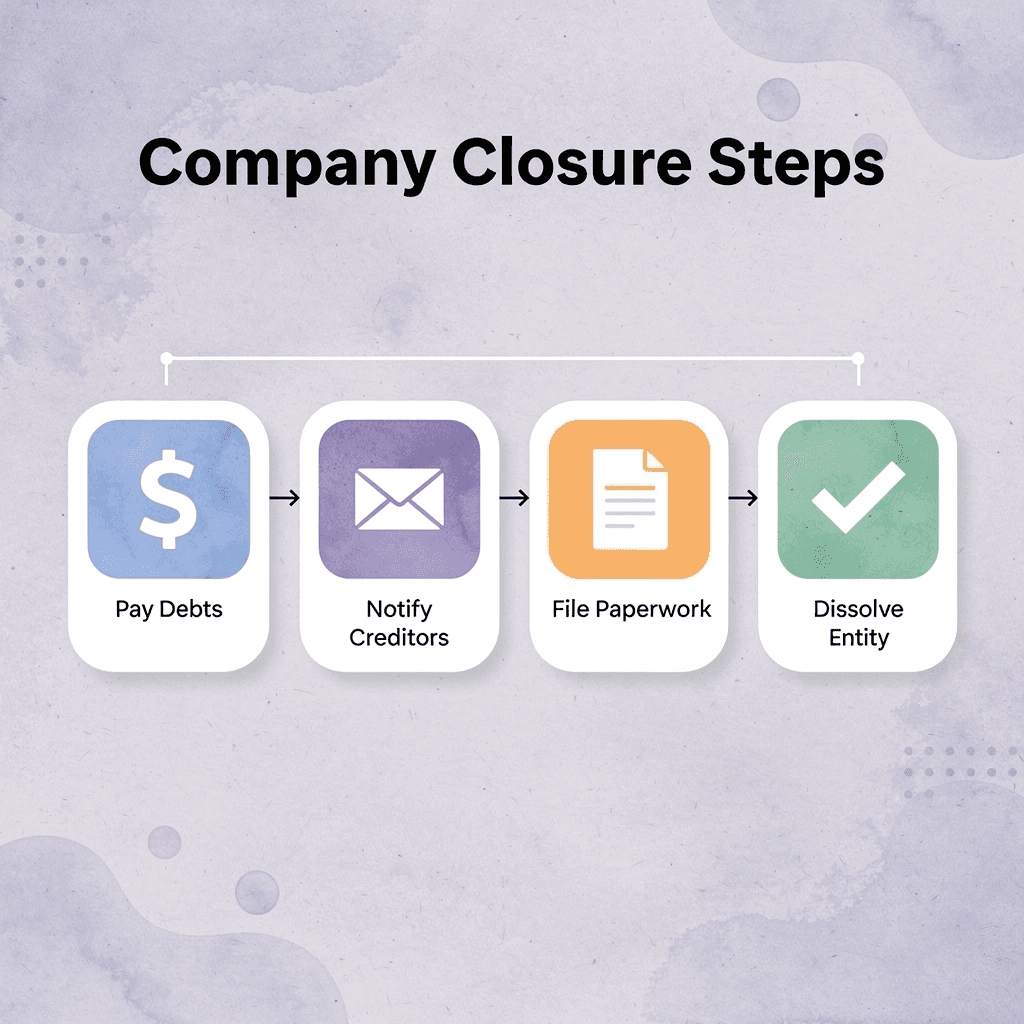

Closing a company means formally ending its legal existence by paying off debts, notifying creditors, completing final paperwork, and dissolving the entity. This differs from stopping operations: the company continues to exist on paper, accumulating penalties and obligations until you complete the formal shutdown.

🎯 Key Point: Simply ceasing business activities doesn't legally dissolve your company—you must complete the formal closure process to avoid ongoing liabilities.

"A company that stops operating but doesn't formally dissolve continues to accrue legal obligations and penalties until proper dissolution is completed." — Business Law Institute

⚠️ Warning: Many business owners mistakenly think closing their doors means closing their company, but the legal entity remains active until you file the proper dissolution paperwork.

The sequence matters more than you think

Paying off debts comes first because creditors have legal standing. Money owed on invoices, loans, employee wages, vendor contracts, and taxes is not optional. You cannot close a company that still owes money without risking personal claims. The order protects you. Next comes stakeholder notification. Employees, partners, vendors, and lenders all require formal notice within specific timelines set by your location. This ensures claims surface before dissolution, not after. Missing these deadlines doesn't eliminate obligations—it only complicates resolution once the company ceases to exist.

Filing closes the loop

Final tax returns, registration cancellations, and government filings close the loop with state and federal systems. Without them, your company remains active on record, triggering ongoing compliance obligations, potential penalties, and the assumption you're still operating. A 2023 Deloitte study found that 34% of dissolved businesses faced post-closure penalties due to incomplete filings. Dissolution is the final step and requires board approvals, shareholder votes, and formal state filings, depending on your structure. It only works if everything before it is resolved: you cannot dissolve a company with outstanding liabilities or incomplete filings.

Why do filing dependencies create closure delays?

The real challenge is the dependencies between steps. Each one unlocks the next, and skipping or misordering creates delays, risks, and incomplete closures, leaving you exposed. Platforms like Starcycle help by mapping these dependencies into tailored action plans, so you know what to do next without having to hunt across state websites or legal forums. Most founders don't realize how many ways this process can stall until they're already deep into it.

Where Company Closures Break Down

The idea that "I'll figure it out as I go" causes most company closures to fail. Small gaps accumulate into delays, costs, and ongoing risk.

🎯 Key Point: Without a structured closure plan, businesses face exponential complications that turn simple shutdowns into costly nightmares.

"Small gaps in closure planning create a domino effect of delays, costs, and ongoing risk that can devastate final outcomes." — Business Closure Analysis, 2024

⚠️ Warning: The "figure it out later" approach to business closure is the #1 reason companies experience extended timelines and unexpected expenses during shutdown.

Incomplete Records and Unclear Liabilities

Founders often lack a complete picture of the company's liabilities. Contracts, vendor balances, taxes, and contingent obligations are scattered across different systems and documents. Missing liabilities can create disputes and follow-up claims later. One founder received a DMCA notice four years after launching a subscription service, forcing immediate operational changes without warning. The claim arrived after years of silence, and platform compliance occurred automatically before they could respond. What appeared resolved remained legally active.

Missed Filings and Incorrect Legal Steps

Closing a company requires specific filings, final tax returns, deregistrations, and formal dissolution documents. Skipping even one step leaves the company legally active, triggering ongoing compliance requirements, penalties, or unexpected notices months after operations cease. Coresight Research tracked more than 8,100 stores that closed across the U.S. in 2025, yet many left unresolved filings, triggering penalties long after operations ended.

What happens when stakeholders aren't properly coordinated?

Creditors, employees, partners, and regulators must be contacted in a specific order. Without a plan, poor communication can result in creditors not being properly notified, disagreements over what is owed, and extended timelines. Platforms like Starcycle organize these dependencies into tailored action plans, enabling founders to know what to do next without hunting across state websites or legal forums.

Why do company closures break down in execution?

A founder shuts down operations, believing the business is closed, then misses key filings and fails to resolve all liabilities. Months later, penalties and compliance notices arrive. The closure must be revisited at a higher cost and complexity than if handled correctly initially. Company closures fail not in the decision to close, but in execution. Knowing where things break down doesn't tell you how to avoid it.

Related Reading

- IRS Closing A Business

- Shutting Down A Company

- How To Wind Down A Company

- Notice Of Dissolution

- How To Dissolve A Nonprofit

- Irs Cancel Ein

- How To Liquidate A Company

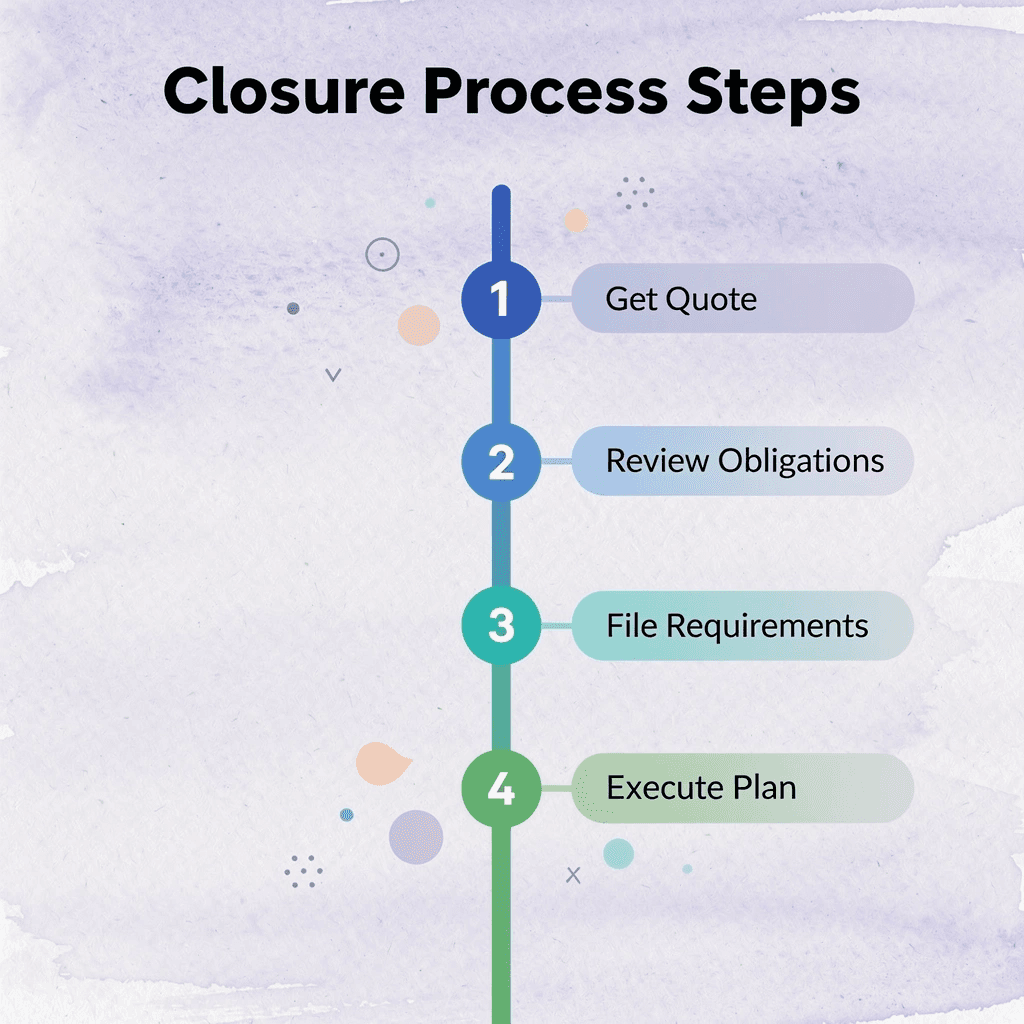

How To Close A Company in 6 Steps

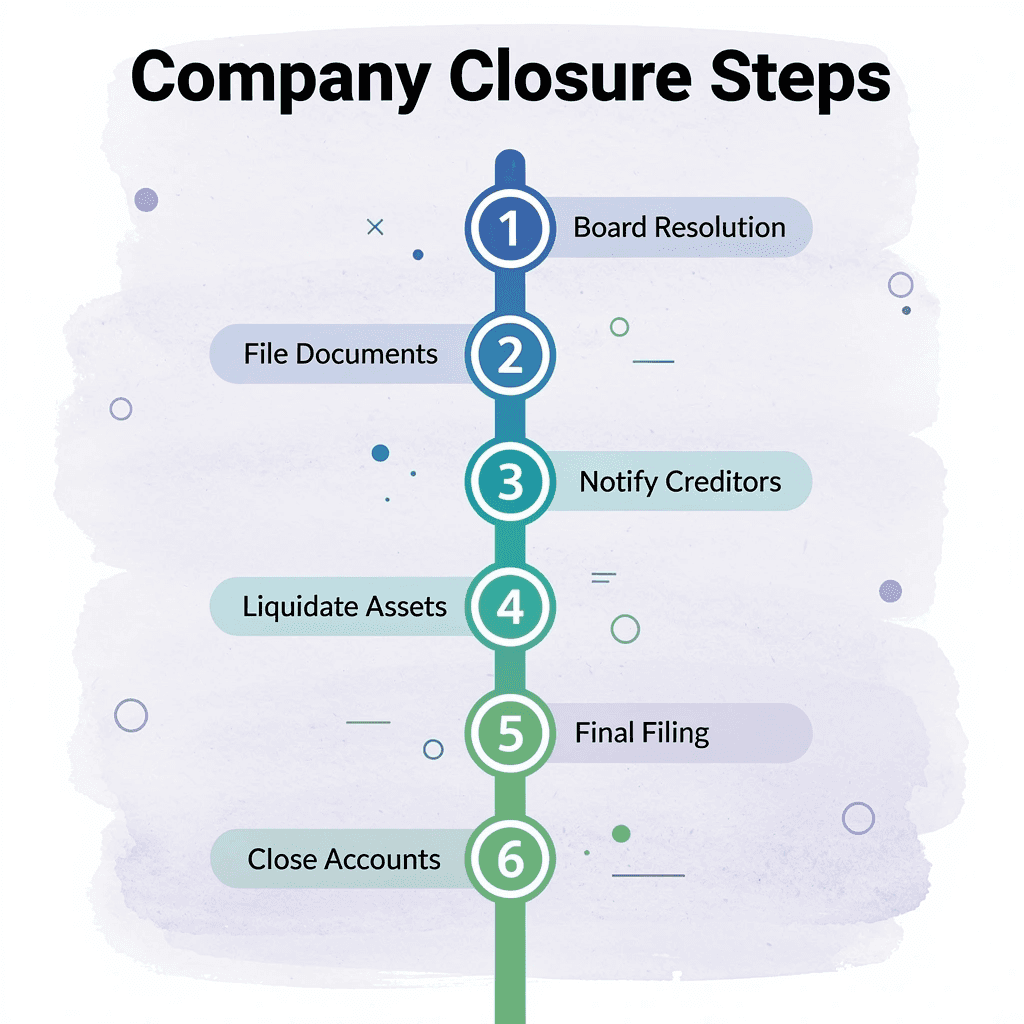

Avoiding the breakdown means following the sequence. Each step depends on the one before it. Miss one, rush another, or reverse the order, and you create gaps that turn into liabilities later. Here's the full process, step by step.

Step | Action Required | Timeline |

|---|---|---|

1 | Board resolution to dissolve | 1-2 days |

2 | File dissolution documents | 3-5 business days |

3 | Notify creditors and stakeholders | 30-60 days |

4 | Liquidate assets and pay debts | 60-90 days |

5 | File final tax returns | Within 4 months |

6 | Complete final state filings | 30 days after assets are distributed |

"85% of business closures face unnecessary delays because owners don't follow the proper sequence of dissolution steps." — Small Business Administration, 2023

🎯 Key Point: The dissolution timeline typically takes 4-6 months when done correctly, but can extend to 12+ months if steps are completed out of order or documentation is incomplete.

⚠️ Warning: Skipping the creditor notification period is the most common mistake that leads to personal liability for business owners, even after the company is officially dissolved.

Step 1: Assess Financial Position

List every asset: cash, inventory, equipment, intellectual property, receivables. Then list every liability: outstanding invoices, loans, unpaid wages, tax obligations, contractual commitments. This is forensic accounting—without knowing what you owe, you cannot settle it correctly. This determines your path forward. If liabilities exceed assets, you may need to file for bankruptcy or negotiate a settlement. If you have enough to cover obligations, voluntary dissolution is possible. Getting this wrong means making legal and financial decisions on incomplete information, risking penalties and personal liability.

Step 2: Decide On Closure Path

Pick the legal exit that fits your situation. If the business can pay its debts, voluntary dissolution is the standard choice. If it cannot, you may need to file for bankruptcy or another insolvency process, depending on your location. This choice affects the timeline, how creditors are treated, and which legal steps you must follow. The way you close determines the creditor payment order. Bankruptcy follows a legal hierarchy: secured creditors, taxes, employee wages, then unsecured debts. Voluntary dissolution gives you more control but still requires you to follow statutory priority rules. Choosing incorrectly can expose you to claims you believed were resolved.

Step 3: Notify Stakeholders

Tell employees, creditors, suppliers, customers, and partners about the closure. In many places, you are required by law to give formal notice with specific deadlines for creditors to submit claims. This protects you from future claims by ensuring everyone has had the opportunity to raise what the company owes them before closure is complete. Skipping or delaying this step is common and expensive. A creditor not notified of the closure can claim they lacked opportunity to collect what they were owed, potentially restarting the closure process or creating personal liability for owners.

Step 4: Settle Debts And Obligations

Pay the business what it owes in the correct order. Taxes, employee wages, and secured debts typically come first, though priority depends on your location and closure path. If you cannot pay everything, negotiate settlements with creditors or work through bankruptcy to resolve claims legally. This clears liabilities that could otherwise follow you after dissolution.

What obligations do founders often overlook?

Founders often underestimate their obligations: contracts with auto-renewal clauses, uncancelled software subscriptions, and missed tax filings. Each represents a potential liability. Resolving them before filing dissolution paperwork prevents post-closure penalties and legal exposure.

How can you manage complex obligations efficiently?

Keeping track of what you owe across contracts, tax filings, and vendor agreements can feel overwhelming when managing a shutdown on your own. Platforms like Starcycle organize these into a single action plan, helping founders determine what needs to be settled and in what order.

Step 5: File Legal And Tax Documents

Submit the paperwork that legally ends the business: final tax returns, dissolution forms with your state or national registry, cancellation of business licenses, and deregistration of permits. Each jurisdiction has different requirements, and missing even one filing can leave the entity active on record, creating ongoing compliance obligations and potential penalties.

What happens if you miss required filings?

According to a 2022 study by the National Federation of Independent Business, 41% of businesses that dissolved faced penalties after closing due to incomplete filings. The most common problems were missed final tax returns and failure to cancel state registrations. Formal dissolution on file also protects you if someone later claims the business owes them money. Without it, you may remain legally responsible for obligations arising after closure.

Step 6: Distribute Remaining Assets

After debts are paid and paperwork is finished, distribute the remaining assets. For corporations, assets go to shareholders based on their ownership stake. For LLCs, distribution follows the operating agreement or state default rules. For sole proprietorships, remaining assets belong to the owner.

What are the legal requirements for asset distribution?

Asset distribution must follow legal priority rules. You cannot distribute assets to owners if creditors haven't been paid, as doing so creates personal liability and allows creditors to pursue those assets even after transfer. Liabilities must be paid before assets are distributed.

When is the business legally closed?

Once assets are distributed and all filings are complete, the business is legally closed with no remaining obligations, compliance requirements, or legal exposure.

What A Clean Company Closure Should Achieve

A clean company closure means nothing is left unresolved—legally, financially, or operationally. Most founders treat closure like flipping a switch: stop answering emails, stop paying bills, stop showing up. That's abandonment, not closure, and it leaves you exposed long after you've moved on.

🎯 Key Point: Proper closure requires systematic resolution of all outstanding obligations, not just walking away from the business.

"Abandoning a business instead of properly closing it can create legal and financial liabilities that persist for years, potentially affecting future ventures and personal assets." — Business Law Institute, 2023

⚠️ Warning: Incomplete closure can result in ongoing tax obligations, creditor claims, and regulatory penalties that surface when you least expect them.

Clear Resolution of Obligations

Every liability must be identified, addressed, and either settled or formally discharged. According to the U.S. Small Business Administration, many failed businesses carry outstanding debt at the time of closure, often tied to loans, vendor obligations, or taxes. Without a structured process, these obligations persist and accumulate interest, penalties, or legal claims. Creditors have legal tools to enforce claims years later.

Minimal Personal Exposure

This is where closures quietly fail. If personal guarantees were signed or compliance steps are missed, creditors may pursue claims beyond the business itself. Proper sequencing around debt settlement and filings protects the boundary between the company and the founder. Skip a filing, miss a notice period, or leave a tax return incomplete, and the shield dissolves—personal assets become fair game.

A Defined Legal Endpoint

A company is truly closed only when formally dissolved by the relevant authority. According to the Internal Revenue Service, businesses must file final tax returns and formally close accounts to end tax obligations. Missing this step leaves the entity active on record, which can trigger ongoing reporting requirements or penalties even after operations stop. The company exists in the eyes of the law until you formally notify the law otherwise.

How can you streamline the closure process?

Most founders manage closure through spreadsheets, email threads, and memory, tracking debts in one place, contracts in another, and filings in a third. As complexity grows, things slip through: vendor invoices get overlooked, state filing deadlines pass unnoticed, tax forms sit incomplete. Platforms like Starcycle centralize the entire shutdown process, organizing contracts, deadlines, and filings in one place with step-by-step guidance tailored to your situation. They compress what typically takes months of fragmented effort into a structured path with clear milestones.

The Ability to Move On Without Lingering Issues

Closure should create finality: no follow-up notices, unresolved claims, or administrative loose ends. Without this, founders often revisit the business months later to fix avoidable mistakes. The shift moves from reactive and uncertain to structured and complete, with every obligation addressed, every requirement met, and the company fully closed in both practice and law. But knowing what closure should achieve differs from knowing how to make it happen, which most founders underestimate.

How Starcycle Helps You Close A Company With Clarity

Execution is where most closures break down. You're managing creditors, state filings, tax obligations, and stakeholder notifications across different timelines, each with consequences for missteps. Starcycle solves this by organizing the entire closure process into a structured, step-by-step plan that ensures nothing is missed and everything happens in the right sequence.

"The majority of business closure failures stem from poor execution and missed deadlines, not lack of intent." — Business Closure Research, 2023

🎯 Key Point: Starcycle transforms chaotic closure requirements into a manageable workflow that prevents costly mistakes and ensures regulatory compliance.

⚠️ Warning: Attempting to manage multiple closure deadlines without a systematic approach often leads to missed filings, penalty fees, and extended liability exposure.

A Single View of What You Actually Owe

The first breakdown point is the lack of complete financial visibility. Debts hide in forgotten subscriptions, vendor agreements, or tax obligations that haven't surfaced yet. Starcycle maps your full financial picture up front, consolidating assets, liabilities, and contractual obligations into a single view. Instead of discovering problems as they appear, you see everything that needs resolution before you start.

Sequenced Actions That Prevent Rework

Closing a business requires following specific steps in the right order. Filing for dissolution before paying certain debts eliminates legal protections. Late stakeholder notification triggers penalties. Missing a final tax return leaves the entity active on state records indefinitely. Starcycle organizes these actions sequentially, so each step builds on the last without creating new problems. You move through a defined path designed to close cleanly the first time, rather than reacting to missed filings or rejected documents.

Guided Support When Decisions Get Unclear

Founders often lose important time figuring out unclear next steps: applying for dissolution permits without ending vendor contracts, or filing final taxes before documenting creditor obligations. Starcycle provides step-by-step guidance at each stage, delivering clarity when needed most.

The Outcome Clean, Final, Done

What changes is finality. You complete every required step with documentation to prove it: no penalties arriving months later, no creditors showing up because a notification wasn't sent, no state filings left open because the sequence was wrong. According to Starcycle's analysis, professional closure support starting at $299 helps prevent post-closure complications that cost founders thousands in legal fees and lost time. You finish strong with nothing left unresolved. But knowing the process exists differs from starting it.

Related Reading

- Liquidation Vs Bankruptcy

- Close Corporation Taxation

- Llc Termination Vs Dissolution

- Company Liquidation Process

- Startup Shutdown

- How Much Does It Cost To Close an LLC

- How To Tell Investors That You're Shutting Down

- How To Dissolve A Partnership With The Irs

- Dissolving In Europe

- Dissolving In Canada

Sign up to Make your Business Closure Process Easier

Sign up with Starcycle to get a quote, and in your first session, you'll receive a structured breakdown of your obligations, required filings, and exact next steps. You gain clarity before you commit, with a roadmap that removes the guesswork from every decision that follows.

🎯 Key Point: Most founders gather closure advice from scattered sources (state websites, legal forums, accountant emails) and hope the pieces fit together. That approach fails when you discover six months later that you skipped a creditor notification deadline, filed dissolution before terminating a lease, or missed a final tax form that keeps your entity active on state records.

"Platforms organize the entire process into a sequenced action plan, starting at $299, so you handle obligations in the right order and finish without unresolved threads." — Starcycle Process Overview

Platforms like Starcycle organize the entire process into a sequenced action plan, starting at $299, so you handle obligations in the right order and finish without unresolved threads.

💡 Takeaway: Closure is where you take control of the transition, protect what you've built, and create space for what comes next. Start there, with a system that respects both the complexity of what you're leaving behind and the clarity you need to move forward.