IRS Closing A Business: What Most Founders Miss

IRS closing a business requires specific steps most founders overlook. Starcycle's expert guide covers tax obligations, forms, and deadlines.

Dissolving an LLC requires more than simply closing the doors and walking away. The IRS has specific requirements for business closure, and missing even one step can result in unexpected tax bills, penalties, or ongoing obligations years later. Proper dissolution involves filing final tax returns, canceling the EIN, settling payroll obligations, and notifying the appropriate government agencies.

Many business owners underestimate the complexity of this process and overlook critical compliance requirements in their eagerness to move forward. The paperwork, deadlines, and agency notifications can consume weeks of research and preparation. Expert guidance ensures every stage of winding down operations proceeds correctly, eliminating the stress of managing complicated business closure requirements.

Table of Contents

- Most Founders Think Closing With The IRS Is Simple

- Why This Misunderstanding Creates Risk

- What IRS Closing A Business Actually Involves

- Why Founders Still Get It Wrong

- What A Proper IRS Business Closure Actually Looks Like

- How Starcycle Helps You Close Your Business With The IRS The Right Way

- Sign up to Make your Business Closure Process Easier

Summary

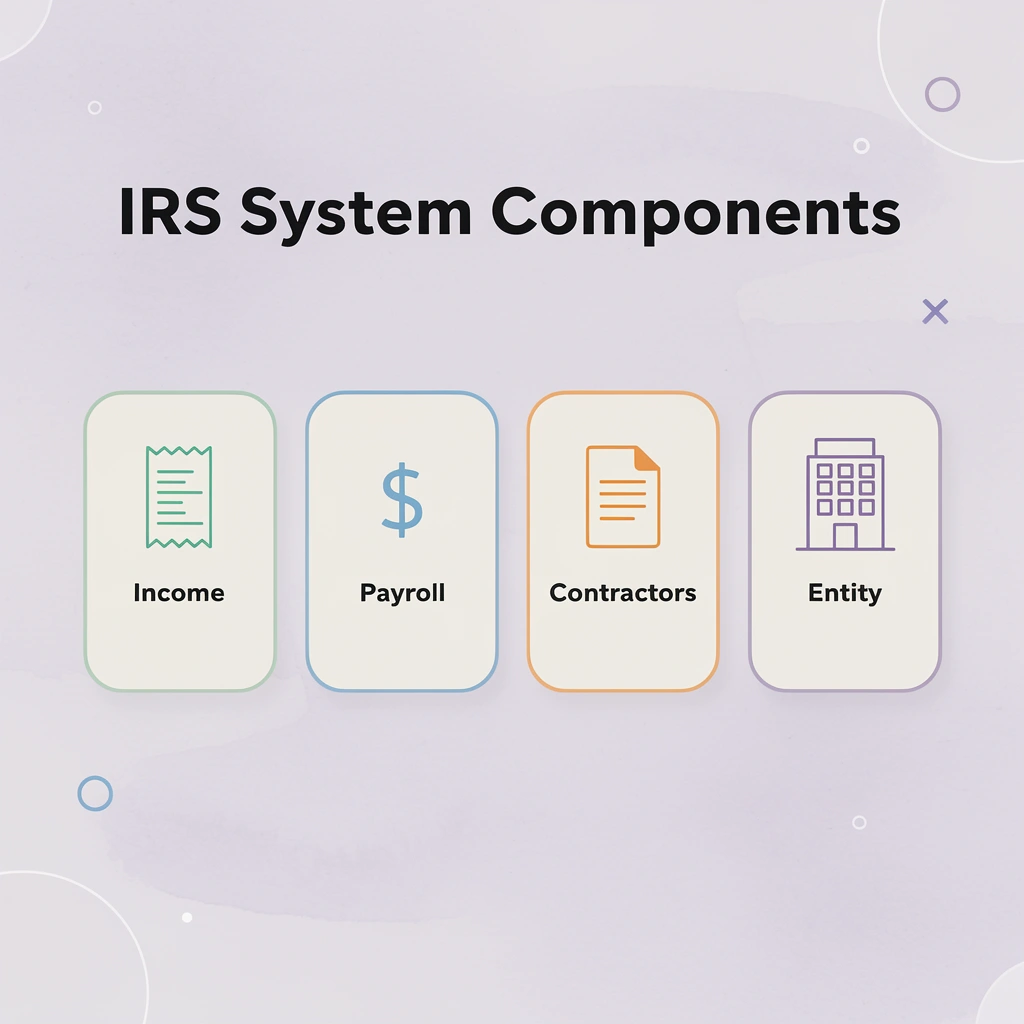

- The IRS does not treat business closure as a single action but as a detailed process involving multiple separate requirements. According to the U.S. Bureau of Labor Statistics, only 34.7% of businesses founded in 2013 were still operating in 2023, meaning nearly two-thirds closed within ten years. Yet many founders still approach closure informally, assuming that a single final filing ends their obligations. The reality is that closure requires final income tax returns, payroll tax filings, contractor reporting, tax payments, EIN account-closure requests, and record-retention obligations, all coordinated across different IRS systems.

- The IRS interprets silence as noncompliance, not closure. If you don't file a final return or mark it correctly, the system continues expecting quarterly filings and annual returns. According to IRS penalty data from 2023, failure-to-file penalties start at 5% of unpaid taxes per month and can reach 25% of the total balance, while failure-to-pay penalties add another layer of compounding cost. These automatic charges accrue the moment a deadline passes without proper filing, creating accumulated costs that surface months after founders believe everything is finished.

- Your EIN remains permanently assigned to your business entity even after it is closed. Unless you formally notify the IRS that the business has dissolved, the account stays active in their system. This creates situations where the business feels closed on your end but remains open on theirs, generating filing expectations that trigger notices when those filings don't arrive. The number itself never gets canceled, but you can close the associated business account by confirming operations have ceased, all final returns are filed, and all tax liabilities are paid.

- Employment tax obligations don't end when operations stop. If you had employees at any point during your final year, you must file final employment tax returns, including Form 941 (or 944 for smaller employers), Form 940 for federal unemployment tax, and issue W-2s to employees by the January 31 deadline following closure. If you paid independent contractors $600 or more, you're required to issue 1099-NEC forms by the same deadline. These federal reporting requirements remain enforceable even after the shutdown.

- Timing constraints add pressure to an already complex process. According to the IRS MeF shutdown schedule for 2025, electronic filing systems close at 11:59 a.m. Eastern Time, so founders racing to submit final filings before year-end must account for the hard cutoff. Missing these windows pushes filings into the next tax year, extending the closure timeline and creating additional compliance periods that could have been avoided with better coordination of deadlines.

- Starcycle's business closure service addresses this by centralizing shutdown workflows with key date tracking and document organization, compressing what typically takes weeks of scattered effort across income taxes, payroll systems, and contractor reporting into a clear, sequenced action plan.

Most Founders Think Closing With The IRS Is Simple

Most founders think closing a business with the IRS is a final paperwork step: submit one last return, check a "final return" box, and the business is gone. This makes sense because taxes happen every year, so closure feels like one more filing event.

🎯 Key Point: The IRS business closure process involves multiple steps beyond a simple final tax return, including potential asset distributions, employment tax obligations, and entity-specific requirements that can take months to complete properly.

"Business closure with the IRS requires careful attention to final employment taxes, information returns, and entity dissolution procedures that go far beyond a simple final return." — IRS Business Closure Guidelines

⚠️ Warning: Treating IRS closure as a single filing event can lead to ongoing tax liabilities, penalty assessments, and compliance issues that persist long after you think the business is officially closed.

Why does the IRS treat business closure as a complex process?

But the IRS treats business closure as a process, not a single action: one that is far more detailed than most founders expect.

What specific filings does the IRS require for closure?

The IRS requires multiple separate filings: final income tax returns, payroll tax filings, contractor reporting, tax payments, EIN account closure requests, and record retention obligations. This complexity matters because business closure is common.

According to the U.S. Bureau of Labor Statistics, only 34.7% of businesses founded in 2013 were still operating in 2023, meaning nearly two-thirds closed within ten years. Yet many founders approach closure informally.

What happens when business owners take an informal approach?

Founders often stop operating, shut down the website, and close the bank account, assuming IRS obligations end with the business. They don't. The IRS requires returns to be filed by their deadlines, even if a business is no longer operating. Businesses with employees must also complete final employment tax filings and issue final payroll forms.

Why do filing requirements vary by business structure?

Your obligations depend heavily on business structure. A sole proprietorship, partnership, S corporation, and corporation all have different filing requirements during closure. Some entities must file additional dissolution forms, while others must formally notify the IRS to close business accounts. Closing a business involves interconnected steps spanning taxes, payroll, entity structure, and federal reporting obligations.

What are the consequences of missing closure steps?

When founders treat closing a business as a one-time filing event, important steps get missed, leading to ongoing IRS notices, penalties, unresolved payroll obligations, and confusion about whether the business was properly closed.

Related Reading

- How To Close An LLC

- How To File Business Bankruptcies

- Closing A Company

- How To Close A Business With The Irs

- How Much To Dissolve Llc

Why This Misunderstanding Creates Risk

When founders treat IRS closure as a single event, they create a dangerous gap between operational shutdown and administrative reality. The business stops making money, but federal filing obligations continue in the background. That disconnect is where penalties, notices, and unresolved tax accounts accumulate for months after the founder believes everything is finished.

🔑 Key Takeaway: Business closure isn't complete until the IRS officially recognizes it - operational shutdown is only the first step.

"Federal filing obligations continue even after business operations cease, creating potential liability for founders who assume closure is automatic." — IRS Small Business Guidelines

⚠️ Warning: This administrative gap can result in unexpected penalties and tax notices arriving months after you think your business is closed.

How does the IRS interpret missing filings after business closure?

The IRS doesn't see silence as the end of things; it sees it as non-compliance. Without a final return or correct marking, the system continues to expect quarterly filings, annual returns, and employment tax submissions.

According to IRS penalty data from 2023, failure-to-file penalties start at 5% of unpaid taxes per month and can reach 25% of the total balance, while failure-to-pay penalties add another layer of cost that accumulates over time. These charges begin automatically once a deadline passes without proper filing.

The EIN confusion makes everything worse

Most founders assume closing a business means canceling the Employer Identification Number. However, the IRS doesn't cancel EINs as expected. The number remains permanently assigned to your business entity, and unless you formally notify the IRS that the business has closed, the account stays active. This creates a disconnect: the business feels closed to you but remains open to the IRS, triggering filing expectations and notices when those filings don't arrive.

Why do missed steps compound quickly

If you had employees, payroll tax accounts don't close automatically when operations stop. The IRS expects final employment tax returns, and penalties apply if they aren't submitted. Similarly, 1099 forms for contractors paid during your final year must be filed after the shutdown. Many founders receive CP notices months later, forced to reconstruct records and complete filings they didn't know were required.

How can tracking tools prevent administrative oversights?

Platforms like Starcycle help founders track overlapping deadlines using customizable shutdown checklists. These checklists transform administrative confusion into clear action steps, showing final tax returns, payroll closures, contractor reporting, and IRS notifications on specific dates. Founders no longer need to guess which forms remain incomplete or which accounts stay open.

What happens when closure steps are incomplete?

The result is a slow buildup of administrative friction that emerges after you've moved on, creating delays when starting something new because previous obligations were never formally resolved. You're not closing a business anymore—you're fixing one that was never properly closed.

Knowing the risks is only half the picture; the other half is understanding what the IRS expects you to do, step by step, to avoid them.

What IRS Closing A Business Actually Involves

Closing a business with the IRS isn't one form or a one-time submission—it's a series of coordinated filings tied to your business structure and operational obligations. Most founders assume there's a "close my business" button. There isn't.

🎯 Key Point: The IRS requires different closure procedures depending on whether you're a sole proprietorship, LLC, corporation, or partnership—each with distinct filing requirements and deadlines.

"Business closure with the IRS involves multiple coordinated steps rather than a single filing, with requirements varying significantly by entity type and operational history." — IRS Business Closure Guidelines

⚠️ Warning: Failing to properly close your business entity can result in ongoing tax obligations and potential penalties, even after you've stopped operating.

Filing Your Final Income Tax Return

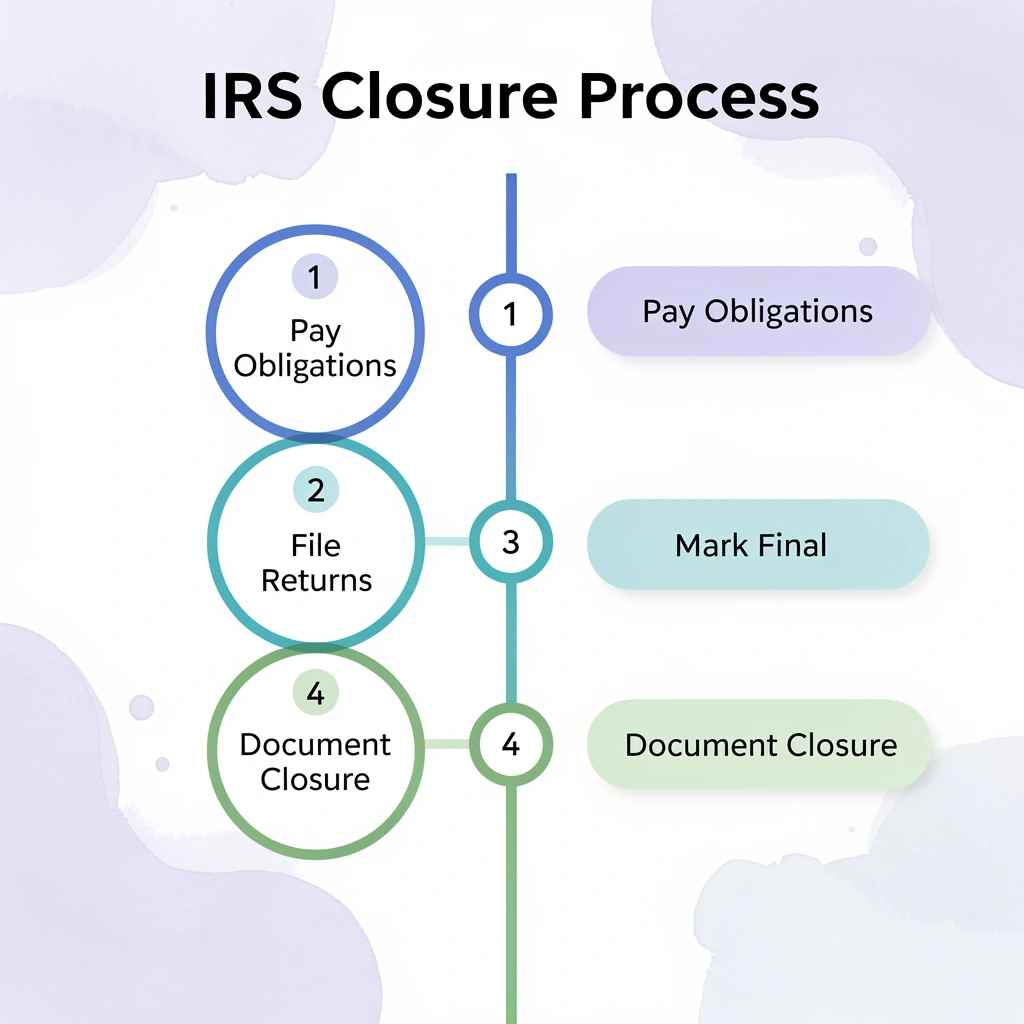

Your final income tax return must be marked as such, and the form you use depends on your entity type. Sole proprietors file Schedule C with their personal 1040 and check the "final return" box. Partnerships submit Form 1065 with "final return" noted at the top. S corporations file Form 1120-S, and C corporations use Form 1120, both of which are flagged as final. If you skip this step, the IRS will expect another return next year.

Settling All Outstanding Tax Liabilities

Every federal tax balance must be paid before the IRS considers your obligations resolved, including income taxes, payroll taxes, estimated tax payments, and excise taxes. Until the balance reaches zero, your business remains active in the IRS system and will continue to accrue interest and penalties.

Handling Employment Tax Obligations

If you had employees during your final year, file Form 941 (or 944 for smaller employers) for payroll taxes, Form 940 for federal unemployment tax, and issue W-2s by January 31 following closure. Issue 1099-NEC forms by the same deadline for any independent contractors you paid $600 or more. These federal reporting requirements remain in effect after the shutdown.

Closing Your IRS Business Account

Your EIN doesn't get canceled—it's permanently assigned to your business. Close the associated account by sending a letter to the IRS confirming the business has stopped operating, all final returns have been filed, and all tax liabilities have been paid.

Without this step, the IRS will continue treating your EIN as active, expect annual returns, and send notices if they don't arrive.

What creates a clear administrative trail with the IRS?

Filing final returns, paying balances, submitting employment forms, and closing your account creates a clear record of your activities. Platforms like Starcycle help founders track these steps with customized checklists and deadline reminders. This can compress what typically takes months into a manageable timeline with fewer missed deadlines.

Even when founders know these steps exist, they still make avoidable mistakes that keep their businesses stuck in IRS systems longer than necessary.

Related Reading

- Involuntary Dissolution Of Llc

- Shutting Down A Company

- How To Wind Down A Company

- Notice Of Dissolution

- How To Dissolve A Nonprofit

- How To Liquidate A Company

- Irs Cancel Ein

Why Founders Still Get It Wrong

The IRS process spans multiple systems with no central workflow. Income taxes, payroll accounts, contractor reporting, and entity-level obligations each have separate forms and deadlines. You must coordinate them yourself, and missing one piece leaves your business marked as active in the system.

🎯 Key Point: The IRS doesn't have a single "close my business" button - you must navigate multiple disconnected systems to fully shut down.

"Each step feels small, but each one keeps part of the business open in the IRS system, generating notices and penalties."

This fragmentation creates dangerous blind spots. A founder files their final return but forgets to close the payroll account, or stops paying contractors but misses final 1099 filings. Each step feels small, yet each one keeps part of the business open in the IRS system, generating notices and penalties.

⚠️ Warning: Even one missed component can trigger ongoing IRS obligations and penalties, making your "closed" business very much alive in their system.

Why do founders underestimate administrative closure?

Founders delay closing their business because it lacks urgency. A missed filing or an IRS notice can feel like a concern later on, even when there's no immediate sign of trouble. Our Starcycle platform helps founders track critical deadlines, ensuring nothing falls through the cracks during the closing process.

But the IRS doesn't wait. According to IRS penalty guidelines, failure-to-file penalties can reach 25% of unpaid taxes, with additional penalties applying to payroll-related obligations if those accounts aren't properly closed.

What happens when closure becomes reactive instead of proactive?

By the time founders realize something is incomplete, they're responding to accumulated issues, notices, penalties, and unresolved accounts that should have been handled earlier.

The familiar approach is to handle closure yourself, filing what seems necessary and assuming the rest will sort itself out. As obligations multiply across different IRS systems, that approach breaks down: critical deadlines get missed, required forms go unfiled, and what felt manageable becomes a fragmented mess of open accounts. Platforms like Starcycle help founders track these distributed requirements with tailored checklists and key date reminders, compressing what often takes months into a manageable timeline and reducing the risk of missed deadlines.

This goes wrong not because the rules are hidden, but because they're distributed, easy to underestimate, and unforgiving when missed. Closure isn't one thing you do: it's a sequence of things you coordinate across systems that don't talk to each other.

What A Proper IRS Business Closure Actually Looks Like

A proper IRS closure means that every tax obligation connected to your business has been fully paid and formally ended with the Internal Revenue Service.

🎯 Key Point: Your final tax return must be clearly marked as "final" to signal the end of your business operations to the IRS.

The process starts with ensuring everything lines up: your tax filings must match when your business shuts down. If your business stopped operating in a given year, your final returns must show that clearly by marking your income tax return as "final." This signals to the IRS that no future filings should be expected for that business.

"Proper business closure requires that all tax obligations be fully satisfied and formally documented with the IRS to avoid future complications." — IRS Business Closure Guidelines

⚠️ Warning: Failing to properly mark your final return or leaving tax obligations unresolved can result in ongoing IRS scrutiny and potential penalties even after your business has closed.

Completing the payroll shutdown sequence

If your business had employees, shutting down payroll requires filing final employment tax returns (Form 941 or 944) and sending final W-2s. For independent contractors, submit final 1099 forms. Missing these steps keeps payroll accounts active in the IRS system after closure, preventing the IRS from considering your business officially closed.

All outstanding federal taxes, including income and employment taxes, must be paid. The IRS does not consider a business closed if balances remain unresolved. Ensure all accounts are balanced with no outstanding discrepancies to reduce the risk of future notices or audits.

What does formal account closure require and accomplish?

To formally close your account, send a request to the IRS with your EIN, business name, address, and proof that you have filed all required returns and paid all taxes. According to the IRS MeF shutdown schedule for 2025, electronic filing systems close at 11:59 a.m. Eastern Time (ET), so submit your final filings before the year-end deadline. This step demonstrates that the business no longer needs to file reports.

Formal closure does not cancel your EIN—it stays permanently assigned to the business. Instead, it ends the active relationship between the business and the IRS and stops future filing requirements. When done correctly, the result is clean: no filings left to do, no unexpected notices, and no confusion about the business's tax status.

Why do founders struggle with closure obligations?

Most founders handle this alone, but as responsibilities spread across income taxes, payroll systems, and contractor reporting, important steps get missed. Months later, IRS notices arrive for unfiled returns or unpaid balances. Our Starcycle platform consolidates shutdown workflows in one place with key date tracking and document organization, transforming weeks of scattered effort into a clear action plan that prevents nothing from falling through the cracks.

How Starcycle Helps You Close Your Business With The IRS The Right Way

Starcycle turns an IRS closure into a structured, guided process for your business. You get a clear action plan tailored to your entity type, payroll history, contractor relationships, and outstanding filings rather than navigating forms, deadlines, and requirements independently. Our platform connects tax obligations with state-level dissolution and broader wind-down tasks, ensuring nothing falls through the cracks.

🎯 Key Point: Starcycle's integrated approach ensures your business closure meets all IRS requirements while coordinating with state obligations for a complete shutdown process.

"Business closures that fail to properly coordinate federal tax obligations with state requirements can result in ongoing compliance issues and unexpected liabilities even after dissolution." — IRS Business Closure Guidelines

⚠️ Warning: Attempting to handle IRS closure requirements independently often leads to missed deadlines, incomplete filings, and potential penalties that could have been easily avoided with proper guidance.

Why coordination prevents problems later

Most founders assume their business is closed after filing the final tax return, but they often miss critical steps, such as closing payroll accounts or sending final 1099 forms. Months later, penalties accumulate as notices arrive and the business remains technically active in the IRS system. Starcycle maps out every required step upfront, ensures filings happen in the correct order, and verifies that accounts are properly closed before you move forward.

What complete closure actually looks like

A founder handling closure alone operates on assumptions: submitting forms they think apply, hoping timing is right, and waiting for problems to surface. A founder using Starcycle operates with certainty. Our platform helps you identify which IRS filings your business requires, complete final returns with correct markings, close payroll obligations without leaving accounts open, and align everything with state dissolution timelines. No guessing whether a step was missed, no revisiting the process later, no reacting to preventable penalty notices.

The outcome is completeness, not convenience

Most founders can find the IRS closure checklist. The challenge is executing it—ensuring every filing, account, and obligation is handled correctly without gaps. Our Starcycle platform transforms what normally takes weeks of scattered work into a step-by-step workflow tailored to your situation. You close completely, confident that no obligations remain and no notices will arrive months later questioning why your business is still active in federal systems.

Knowing the process exists is only half the equation. The other half is making it simple enough that you'll finish.

Related Reading

- Liquidation Vs Bankruptcy

- Close Corporation Taxation

- Llc Termination Vs Dissolution

- Company Liquidation Process

- Startup Shutdown

- How Much Does It Cost To Close an LLC

- How To Tell Investors That You're Shutting Down

- How To Dissolve A Partnership With The Irs

- Dissolving In Europe

- Dissolving In Canada

Sign up to Make your Business Closure Process Easier

Start with Starcycle if you're not sure whether your business is fully closed with the IRS. You'll get a clear breakdown of the required tax filings and closure actions for your entity type, payroll history, and contractor relationships. Our platform tracks deadlines and confirms when accounts are properly closed, so you know nothing was missed.

💡 Tip: Don't guess about IRS closure requirements. Starcycle's platform provides entity-specific guidance that ensures complete compliance with federal systems.

Closing correctly means moving forward without worry that a notice will arrive months later. Starcycle helps founders finish this chapter with confidence that the administrative work is complete and nothing remains open in federal systems.

🔑 Takeaway: Peace of mind comes from knowing your business closure is 100% complete — no loose ends, no surprise notices, no lingering IRS obligations.

"Proper business closure eliminates the risk of unexpected tax notices and ensures founders can move forward with complete confidence in their compliance status." — Business Closure Best Practices