How To Close A Business With The IRS: Step-by-Step Checklist

Learn how to close a business with the IRS using Starcycle's step-by-step checklist. Handle tax forms, final returns, and compliance requirements.

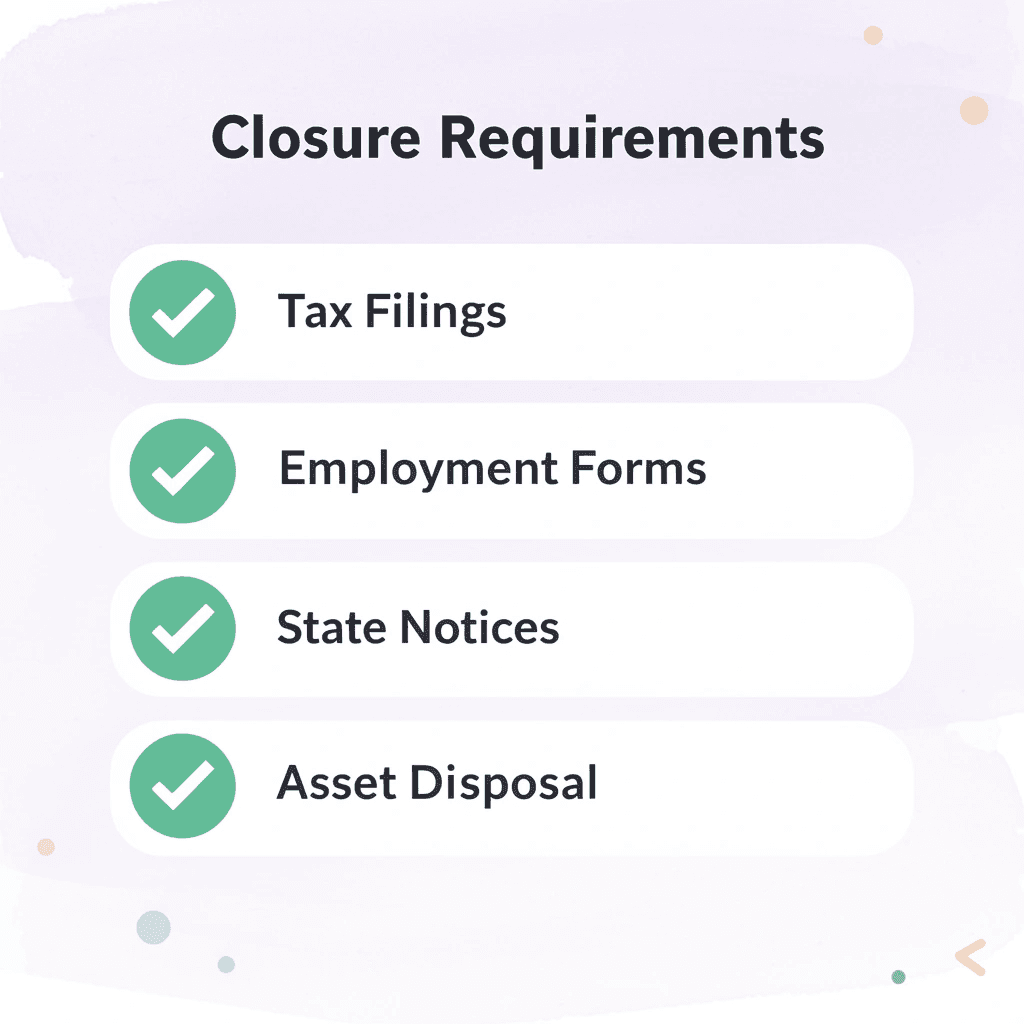

Closing an LLC requires more than simply stopping operations. The IRS continues to expect tax filings and compliance until the proper dissolution procedures are completed, including the filing of final tax returns, state dissolution paperwork, and the cancellation of the employer identification number. Without these steps, business owners face ongoing tax obligations, penalties, and collection notices for companies that no longer exist.

Understanding how to dissolve an LLC and properly close a business with the IRS protects owners from years of unexpected complications. The process involves specific deadlines, required forms, and agency notifications that must be handled correctly. Professional guidance ensures nothing gets overlooked during business closure.

Table of Contents

- Why Closing A Business With The IRS Is More Complex Than Expected

- What Closing A Business With The IRS Actually Means

- Where IRS Business Closures Break Down

- How To Close A Business With The IRS Step By Step

- What A Proper IRS Business Closure Should Achieve

- How Starcycle Helps You Close A Business With The IRS Correctly

- Sign Up to Make Your Business Closure Process Easier

Summary

- The IRS does not automatically recognize that your business has closed when you stop operations. Without proper notification through final tax returns, account closure requests, and employment tax filings, your business remains technically active in federal systems. This triggers ongoing filing expectations, automated penalty assessments, and compliance notices that can continue for years after you've shut down.

- IRS enforcement staff declined by 30% between 2010 and 2018, according to research from Yale Budget Lab. Reduced staffing does not mean less scrutiny. It means slower processing times and more reliance on automated penalty systems that assess charges when filings do not match expectations, making mistakes more expensive by the time they are caught.

- Employment tax noncompliance accounts for over $80 billion in unpaid federal taxes annually, according to the Treasury Inspector General for Tax Administration (2022). A significant portion comes from missed final filings. Businesses that had employees must file final Form 941 for quarterly payroll taxes and Form 940 for federal unemployment taxes, each marked as final, or the IRS will continue to expect quarterly submissions indefinitely.

- Filing a final tax return does not close your IRS business account. Your Employer Identification Number remains on record permanently, but the accounts tied to it require formal closure requests submitted in writing. Without this step, the IRS continues to generate filing reminders and compliance checks even after your business is dissolved under state law, creating an administrative limbo that keeps tax obligations active.

- The IRS held over $130 billion in unpaid business tax debt as of 2022, much of it tied to entities that believed they had closed properly. Unpaid balances continue to accrue penalties at 0.5% per month, plus daily compounding interest, after operations stop. For LLCs taxed as partnerships or S corporations, the IRS can pursue individual partners or shareholders personally when business debts remain unresolved.

- Starcycle's business closure services help founders complete IRS closures by mapping required filings by entity type, identifying outstanding tax obligations before final returns are submitted, and organizing the sequence of forms and account-closure requests to prevent missed steps that keep businesses open in federal systems.

Why Closing A Business With The IRS Is More Complex Than Expected

You can't stop filing and assume the IRS will figure it out. Closing a business requires completing every tax obligation tied to your entity type, employment status, and filing history. One missed form keeps your business technically active, meaning notices, penalties, and interest continue accumulating long after you've locked the door.

⚠️ Warning: Many business owners mistakenly believe that simply ceasing operations is enough to close their business with the IRS. This assumption can lead to ongoing tax liabilities and accumulating penalties that follow you for years after you think your business is closed.

🔑 Takeaway: The IRS requires formal closure procedures that vary significantly based on your business structure. Whether you're a sole proprietorship, LLC, corporation, or partnership, each entity type has specific forms and deadlines that must be met to achieve proper closure.

How many separate tax responsibilities create complications?

The problem is that there are many separate tax responsibilities. Income tax is one part. If you had employees, you are responsible for final payroll tax returns, even if you haven't run payroll in months.

Forms 941 and 940 don't disappear when you stop operating. Skip them, and the IRS will assess penalties immediately. State-level obligations follow separate timelines and don't automatically align with federal closures. Each layer has its own deadline, documentation requirements, and consequences for errors.

Different entities, different requirements

An LLC taxed as a partnership files differently than an S corporation. A sole proprietorship has simpler requirements but still requires a final Schedule C. Corporations often must file Form 966 to report dissolution along with their final 1120. The IRS treats business structures differently, so what works for one founder won't work for another. Founders who follow advice meant for a different entity type often end up with incomplete closures.

Why are IRS processing delays creating bigger problems?

According to research from Yale Budget Lab, IRS enforcement staff declined 30% between 2010 and 2018. This leads to slower processing, longer wait times, and more automated penalty assessments when filings don't meet IRS expectations. The system isn't forgiving: it's slower to catch mistakes, making penalties steeper when they arrive.

What happens when business owners miss required forms?

One founder filed what they thought was their final return, only to receive three separate notices over six months, each demanding a different unfamiliar form. The stress wasn't about money alone; it was the feeling that the process would never end, that something would always be missed. That uncertainty makes it hard to move forward when the past keeps returning.

Our Starcycle business closure services transform this scattered sequence into a clear timeline. We identify which forms apply to your business type, track all deadlines, and ensure the IRS receives everything needed to permanently close your accounts. Rather than guessing what's required or waiting for penalty notices, you get a roadmap tailored to your business type, employment history, and state obligations.

But knowing what to file doesn't explain what the IRS actually does with those documents or why some businesses remain open in their system for years.

Related Reading

- How To Close An LLC

- How To File Business Bankruptcies

- Closing A Company

- Irs Closing A Business

- How To Close A Business With The Irs

- Involuntary Dissolution Of Llc

- How Much To Dissolve Llc

What Closing A Business With The IRS Actually Means

Closing a business with the IRS requires a sequence of formal actions: filing final returns, settling outstanding liabilities, and requesting account closure. Skipping any step leaves your business technically active in federal systems.

🎯 Key Point: The IRS doesn't automatically recognize business closure - you must actively complete all required steps to officially terminate your federal tax obligations.

"Business owners must complete the formal closure process with the IRS, or their entity remains active in federal tax systems indefinitely." — IRS Business Closure Guidelines.

⚠️ Warning: Many business owners assume that stopping operations equals official closure, but the IRS requires explicit notification and final documentation to close your tax account permanently.

What forms do you need for your final tax return?

Every business structure requires a final tax return indicating cessation of business activity. Corporations file Form 1120, partnerships submit Form 1065, and sole proprietors report on Schedule C attached to their personal 1040.

How do you handle the timing and final checkbox?

Your return must include all income and expenses through the actual shutdown date, not just the end of the tax year. If you closed in July, your final return covers January through July, and you check the box indicating it is your final filing.

The IRS uses that checkbox to stop expecting future returns. Without it, the system assumes you are still operating and will send notices requesting your next filing, with penalties accruing automatically.

What happens if you don't settle outstanding tax liabilities?

Unpaid federal taxes, including income taxes, payroll taxes, and estimated payments, must be resolved before closure. The IRS will not close your accounts while a balance remains. If you cannot pay in full, set up a payment plan or submit an offer in compromise before requesting closure.

Tax debt follows you personally if your business structure lacks liability protection or if you're personally responsible for trust fund taxes, such as withheld payroll taxes.

What are the long-term consequences of closing without addressing liabilities?

Founders who close their business without settling debts face years of collection notices, liens, and wage garnishments. The IRS has 10 years from the assessment date to collect, and closure does not forgive what you owe.

How do you close your EIN accounts with the IRS?

Your Employer Identification Number stays on record permanently, but the accounts tied to it can be closed. This requires a written request to the IRS, typically submitted by mail or fax, stating that the business has stopped operating. For businesses with employees, you file a final Form 941 for payroll taxes and mark it as final.

If closing mid-year, file 941 for each quarter you operated, then submit a final annual Form 940 for federal unemployment taxes.

What happens to your EIN after closing?

The EIN itself is never canceled—it stays in the system as an identifier. What changes is the status of the accounts linked to that EIN. Once closed, those accounts stop generating automatic notices and penalty assessments.

The IRS does not send confirmation that closure is complete, so many founders assume silence means success when their request is still being processed or was never received.

How can you properly track the closure process?

Most founders treat closure as a single event, filing one form and moving on. Platforms like Starcycle transform it into a guided sequence, tracking which forms you've filed, which liabilities remain, and when to send closure requests.

Instead of guessing whether the IRS received your paperwork or waiting months for a penalty notice, you follow a checklist built for your business type and employment history. But knowing what to do leaves one question unanswered: why do some businesses remain open in the IRS system for years, even after founders believe they've completed everything correctly?

Where IRS Business Closures Break Down

The problem lies in the gap between what founders think they submitted and what the IRS actually needs to process closure. You file what feels complete, but the system flags it as incomplete because a box wasn't checked, a schedule wasn't attached, or a form series wasn't finalized. These procedural gaps keep your business legally active in the federal tax system, sometimes for years.

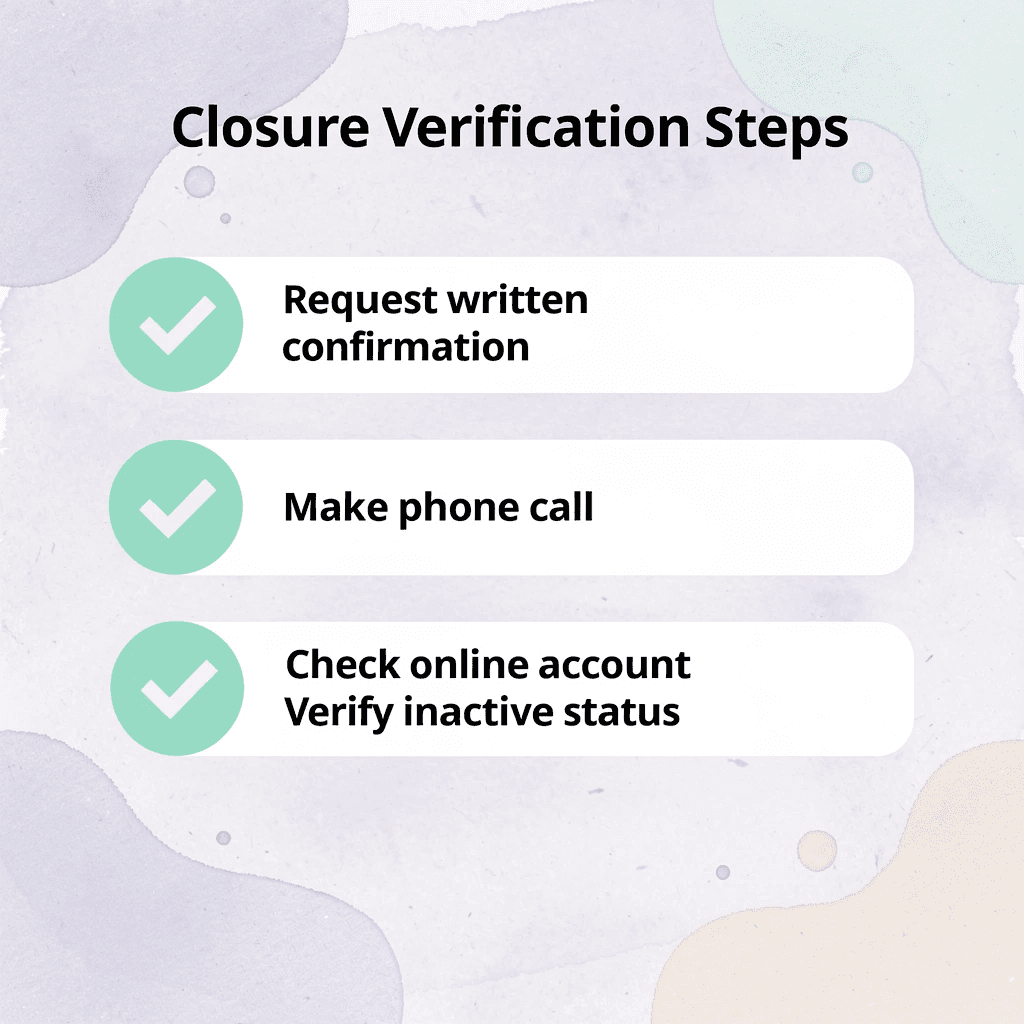

💡 Tip: Always request written confirmation from the IRS that your business closure has been fully processed. A simple phone call or online account check can reveal if your entity is still considered active in their system.

⚠️ Warning: Even minor procedural oversights can result in ongoing tax obligations and penalty assessments long after you think your business is closed. The IRS doesn't send courtesy reminders about incomplete closures.

The Final Return Problem

Filing a final tax return requires clearly marking it as final. Form 1120 for corporations and Form 1065 for partnerships both include a "final return" checkbox. Leave it unchecked, and the IRS expects another filing next year—your business didn't close; it simply went quiet, triggering automated notices instead of closure confirmation.

Partial-year reporting creates similar problems. If you dissolved your LLC in July but filed taxes through December 31, you've reported income for a period when the business legally didn't exist, forcing reconciliation and extending your closure timeline.

Employment Tax Gaps

Most founders know about quarterly Form 941 filings for payroll taxes, but fewer remember that the final Form 941 requires its own "final" designation, separate from your income tax return. According to the Treasury Inspector General for Tax Administration (2022), employment tax noncompliance accounts for over $80 billion in unpaid federal taxes annually, with missed final filings representing a significant portion of that gap. The IRS doesn't assume your payroll obligations ended when you stopped operating.

How does Form 940 factor into business closure?

Form 940 is the annual federal unemployment tax return, and it follows the same pattern. If you had employees during your final year, that return must be filed and marked final. Missing it triggers automatic penalties, even if you owe zero tax.

The Open Account Issue

Filing all required tax forms doesn't automatically close your IRS business account. Your Employer Identification Number (EIN) stays active unless you formally request closure. The IRS continues sending filing reminders, compliance checks, and penalty notices. Our Starcycle platform streamlines the documentation and tracking needed during business closure, making it easier to manage these critical compliance steps.

What formal steps does the IRS require for account closure?

The IRS doesn't close accounts after inactivity. According to IRS Publication 1635, you must submit a formal closure request with your EIN, business name, closure date, and reason for closing. Without this step, your business remains active for federal tax purposes despite being dissolved under state law.

How can you avoid gaps in the closure process?

Platforms like Starcycle help founders avoid these gaps by organizing closure requirements into entity-specific checklists that track which forms need final designations, which tax accounts require formal closure requests, and which deadlines still apply after operations stop.

Why Structure Prevents Breakdown

The pattern is consistent across entity types. Founders assume good intent translates to complete filings, but the IRS system operates on explicit signals, not implied ones. A missing checkbox, an unfiled form, or an unclosed account each produce the same outcome: your business remains open, obligations continue, and penalties accumulate on a timeline you didn't know existed. The question isn't whether you intended to close properly, but whether you followed the specific procedural steps the IRS requires to recognize closure—and most founders don't know what those steps are until something goes wrong.

Related Reading

- IRS Closing A Business

- Shutting Down A Company

- How To Wind Down A Company

- Irs Cancel Ein

- How To Dissolve A Nonprofit

- Notice Of Dissolution

- How To Liquidate A Company

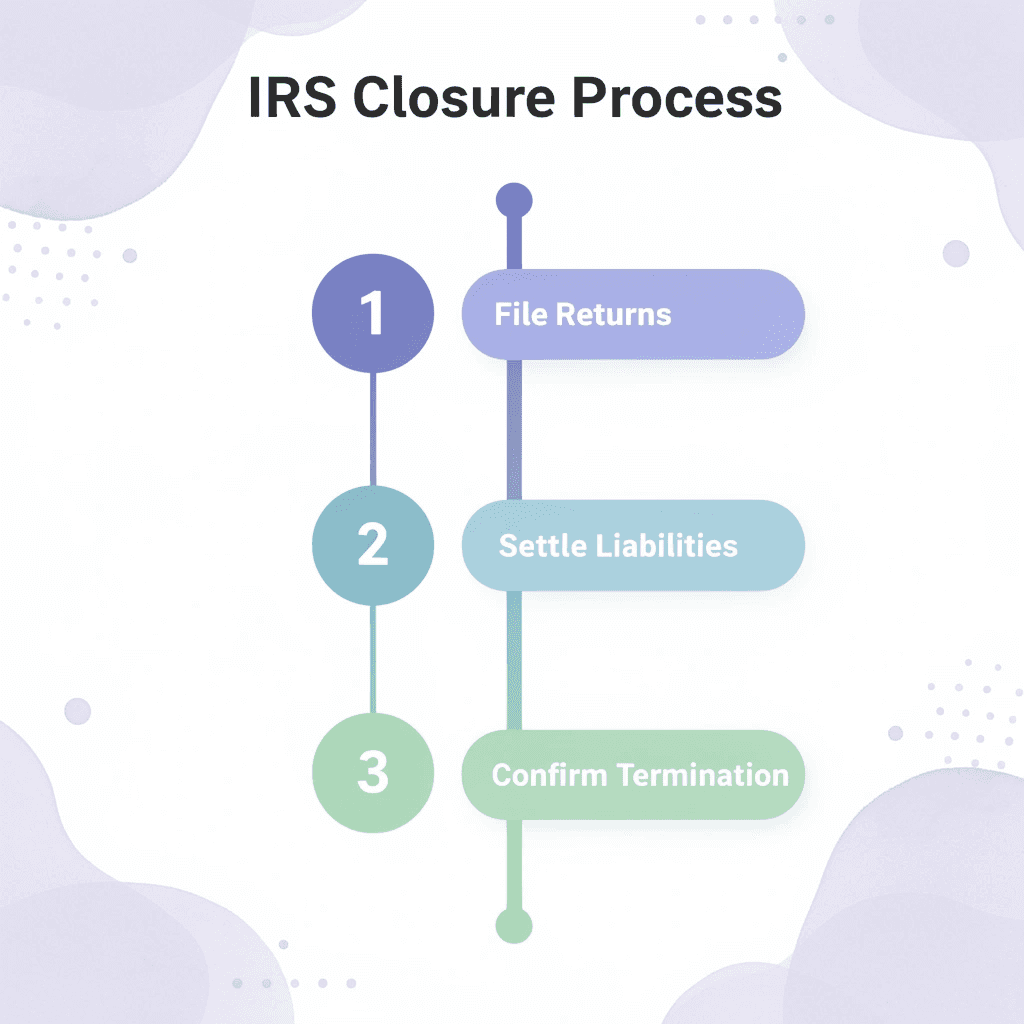

How To Close A Business With The IRS Step By Step

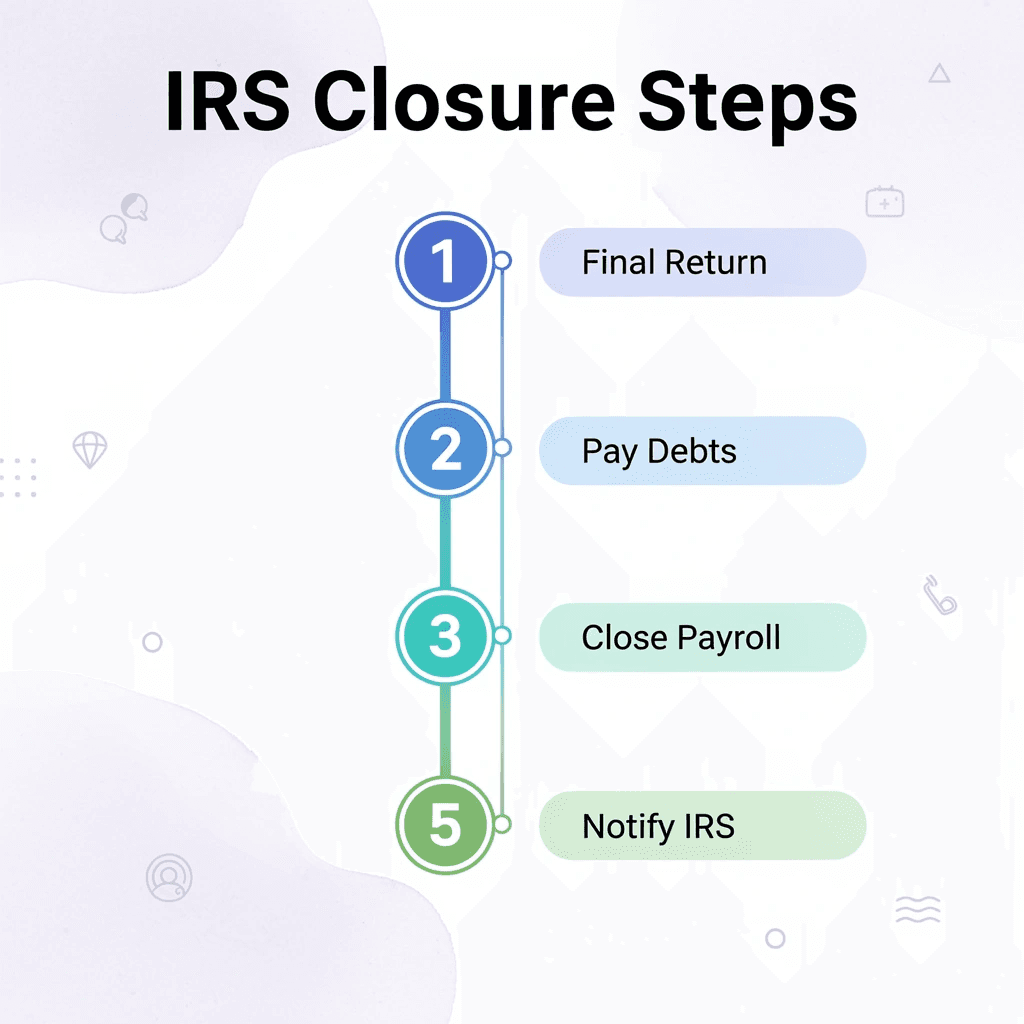

You file a final tax return marked as final, pay what you owe, close payroll accounts if needed, issue final wage forms, and formally notify the IRS to close your business account. Each step depends on completing the previous one correctly—miss a checkbox or a form, and the IRS will continue treating your business as active.

🎯 Key Point: The IRS closure process is sequential—each step must be completed correctly before moving to the next, or your business remains legally active in their system.

"Missing even a single checkbox or form during business closure can result in the IRS continuing to treat your business as active, potentially leading to ongoing tax obligations." — IRS Business Closure Guidelines

⚠️ Warning: Incomplete closure is one of the most common mistakes business owners make. The IRS doesn't automatically close your business—you must actively complete every required step to avoid future tax complications.

File Your Final Tax Return First

Your final federal tax return notifies the IRS that you won't be filing taxes anymore. The form you use depends on your business structure: sole proprietors file Schedule C with Form 1040; partnerships file Form 1065 with final Schedule K-1s; C corporations file Form 1120 and Form 966 within 30 days of dissolution; and S corporations file Form 1120-S with final K-1s.

How do you report all business activity through closure?

Your final return must include all income, deductions, and business activity through your exact closure date. Asset sales during shutdown (equipment, inventory, or other business property) get reported on Form 4797.

If you stopped operating in July but only report activity through June, the IRS will flag the gap and send automated follow-up notices.

Settle All Outstanding Tax Liabilities

Closure does not erase tax obligations. Federal income taxes, payroll taxes, estimated payments, and other liabilities must be paid before the IRS considers your account settled. If you cannot pay in full, you can request a payment plan or submit an offer in compromise, but the debt remains.

Unpaid balances continue accumulating penalties and interest after you stop operating. The IRS applies failure-to-pay penalties at 0.5% per month, compounding until cleared. Shutting down doesn't halt enforcement; collection actions often accelerate once the business stops generating revenue, as the IRS prioritizes recovery before it becomes harder.

Close Payroll Accounts And Issue Final Forms

If you had employees, file final payroll tax returns and mark them as final. Form 941 covers quarterly payroll taxes, or Form 944 if you filed annually. Form 940 reports federal unemployment tax. Each requires the final return box checked. Missing this step is one of the most common reasons businesses receive IRS notices months or years after closure.

What employee forms must you issue by January 31?

Give W-2 forms to employees and send Form W-3 to the Social Security Administration by January 31 of the next year. Contractors who received $600 or more must receive Form 1099-NEC, with Form 1096 as the transmittal. Without these, the IRS assumes payroll obligations remain active and continues expecting quarterly filings.

How can you streamline the IRS closure process?

Most founders underestimate how quickly this becomes overwhelming. You're managing vendor payments, contract cancellations, and the emotional weight of shutdown. Then the IRS checklist arrives: cross-referencing form numbers, tracking down payroll records, and figuring out which boxes to check. Platforms like Starcycle help founders move through this faster by organizing documents, tracking deadlines, and providing step-by-step guidance tailored to your entity type. The goal is reaching what's next without the IRS following you there.

Notify The IRS To Close Your Business Account

Filing a final return doesn't automatically close your IRS account. Send a formal letter that includes your Employer Identification Number, business name, address, and reason for closure. Without this step, your account remains open, and automated notices continue to arrive.

Your EIN is permanent and cannot be deleted or reassigned to another business. Once all filings are complete and your account is formally closed, the IRS marks the EIN as inactive, stopping future compliance requirements from being attached to a business that no longer exists.

But filing the right forms and checking the right boxes gets you only halfway there.

What A Proper IRS Business Closure Should Achieve

A proper IRS business closure should achieve complete administrative compliance and strategic finality: nothing remains open, nothing continues building up, and no future obligations attach to the business entity. This means ensuring the IRS has no reason to contact you again—not just by filing your last return.

🎯 Key Point: Complete closure means eliminating all future IRS contact possibilities, not just submitting final paperwork.

⚠️ Warning: Filing your final tax return is only the first step—true closure requires addressing all outstanding obligations and administrative loose ends.

"Strategic finality in business closure means ensuring no future obligations attach to the business entity, creating a clean break from all IRS responsibilities." — Tax Administration Best Practices

No Outstanding Tax Liabilities

Every federal obligation must be resolved before the IRS considers your business closed: income tax, payroll tax, estimated payments, and prior penalties. Unpaid balances accrue a 0.5% monthly failure-to-pay penalty plus daily compounding interest. According to the Treasury Inspector General for Tax Administration (2022), the IRS held over $130 billion in unpaid business tax debt, much from entities that believed they had closed properly. The debt doesn't disappear—it transfers. If you operated as an LLC taxed as a partnership, the IRS can pursue individual partners. If you were an S corporation, shareholders may face assessments. Proper closure eliminates that exposure.

No Ongoing Filing Requirements

Once your final returns are filed and your account is closed, the IRS marks your EIN as inactive and stops sending automated reminders for quarterly filings, annual returns, or other compliance requirements. This requires checking the final return box on every applicable form, reporting through your dissolution date, and ensuring employment tax filings match your last payroll. Without this step, the system continues generating notices that become penalties for non-filing, even though your business no longer exists.

Clear Closure Status in IRS Records

Your EIN stays on record indefinitely but should be marked as inactive. An active EIN indicates your business is operating and further filings are expected. An inactive EIN indicates you have completed all responsibilities and no additional activity is planned. The IRS does not issue confirmation letters or certificates of closure. Verify your status by confirming no future notices arrive, and your account shows no outstanding balances or pending filings.

No Future Penalties or Automated Notices

A properly closed business creates no follow-up issues: no letters about missed filings, no building penalties, no automated assessments for returns the IRS believes you should have filed. Most founders file a final return and assume they're done, only to receive a notice six months later about a missing quarterly payroll filing or an unfiled state reconciliation. Our Starcycle platform helps ensure nothing falls through the cracks during closure by organizing and tracking all required filings in one place.

The notice triggers a penalty, which builds interest and worsens the issue. Proper closure prevents this entirely.

How do you ensure the IRS agrees your business is finished?

Closure happens when the IRS agrees you are finished, not when you stop operating. That agreement requires deliberate action, accurate reporting, and confirmation that every account tied to your EIN has been resolved.

Platforms like Starcycle help founders navigate this by organizing required filings, tracking closure milestones, and ensuring nothing gets missed between dissolution and final IRS resolution. Without such coordination, overlooking a single form or missing a final designation can leave your business open in the IRS system long after you thought it was closed.

But even with every form filed and every balance paid, one more layer remains that most founders do not anticipate.

How Starcycle Helps You Close A Business With The IRS Correctly

IRS closures fail not because people don't care, but because of broken processes, unclear rules, and out-of-order steps. Starcycle solves this by providing structured support that matches how closure actually works.

The platform maps all required IRS filings based on your business type—sole proprietor, partnership, or corporation—and outlines which forms apply to you. This eliminates a major failure point: using the wrong forms or missing required ones.

🎯 Key Point: Starcycle eliminates the guesswork by providing business-specific filing requirements tailored to your exact entity type.

"The platform maps all required IRS filings based on your business type and outlines exactly which forms apply to you."

⚠️ Warning: Using the wrong forms or missing required filings is one of the most common reasons IRS business closures get rejected or delayed.

Upfront Visibility Into Tax Obligations

Starcycle identifies outstanding tax obligations before filing, giving you clear visibility into what needs to be resolved before closure. This reduces the risk of penalties and IRS notices. Many founders report being surprised by employment tax balances or estimated payment shortfalls months after believing their business was closed.

Starcycle then organizes your documents and filings in the correct order. IRS closure is order-dependent: final returns, employment filings, payments, and account closure must happen in a specific sequence. This prevents rework and rejected filings. You're guided step by step through a defined path designed to prevent issues rather than react to them.

What This Changes in Practice

Instead of filing a final return and later discovering missed employment tax forms, you identify all required filings upfront, complete them correctly, and close your IRS account without follow-up issues or penalties. You gain confidence moving forward without wondering if something will surface later.

Sign up to get a quote. In your first session, you'll receive a clear breakdown of your IRS filing requirements and next steps to close your business cleanly and completely.

Sign up to Make your Business Closure Process Easier

Closing a business the right way means you move on completely: no surprise notices months later, no penalties piling up while you're focused on what comes next. Finishing cleanly protects your work and keeps your options open.

🎯 Key Point: Most founders try to handle closure themselves until they're three forms deep and unsure if they've covered everything. The cost of getting it wrong isn't immediate—it's the IRS letter that arrives when you thought you were done, or penalties compounding while you're building something new.

"The cost of getting business closure wrong isn't immediate—it's the IRS letter that arrives when you thought you were done, or penalties compounding while you're building something new." — Business Closure Reality

Starcycle was built by founders who've navigated this exact process. Our platform maps your filing requirements based on your business structure, flags outstanding obligations before they become problems, and organizes the sequence so nothing gets missed.

What You Get | How It Helps |

|---|---|

Complete breakdown of requirements | Know exactly what needs to happen |

Proper sequencing of filings | No missed deadlines or dependencies |

Employment tax guidance | Avoid common compliance gaps |

Final return verification | Ensure proper closure marking |

Your first session gives you a complete breakdown of what needs to happen and in what order. No guessing about employment tax filings or whether your final return was marked final: just a clear path from where you are now to fully closed.

💡 Tip: If you're ready to be actually done, sign up and move forward knowing the IRS piece is handled correctly. Complete closure means true peace of mind for your next venture.