How to Dissolve a Partnership With the IRS: Step-by-Step Guide

How to dissolve a partnership with the IRS made simple. Starcycle's step-by-step guide covers tax forms, deadlines, and requirements.

Ending a business partnership requires more than a handshake between partners. The IRS must be properly notified through specific procedures, and mistakes can result in unexpected tax bills, continued liability, or future audits. Partnership dissolution involves filing final tax returns, settling outstanding obligations, and formally dissolving the partnership with federal authorities. Missing these steps creates ongoing complications that can persist for years.

The process includes multiple deadlines and detailed documentation requirements that vary by partnership structure and state of operation. Partners must coordinate final distributions, resolve any remaining debts, and ensure all tax obligations are satisfied before the entity can be legally terminated. Professional guidance often proves essential for navigating the complex requirements of business closure.

Table of Contents

- Why Dissolving a Partnership Involves More Than Just the IRS

- What Does It Mean to Dissolve a Partnership?

- How to Dissolve a Partnership With the IRS

- The Non-IRS Steps Many Partnerships Overlook

- What a Proper Partnership Winddown Looks Like

- How Starcycle Helps Founders Navigate Partnership Dissolutions With More Clarity

- Sign up to Make your Business Closure Process Easier

Summary

- Partnership dissolution requires coordinated action among multiple government agencies that don't communicate with one another. The IRS handles federal tax obligations, but your state still considers the partnership active until you file separate dissolution paperwork. According to the Small Business Administration's 2023 closure report, 41% of business owners who attempted to dissolve without professional guidance missed at least one required state filing, resulting in penalties or ongoing obligations they believed had been resolved.

- The IRS requires partnerships to file a final Form 1065 for the year they cease operations, but that return can't be filed until all financial activity is complete. This creates a gap between when partners stop taking new business and when the partnership can legally close. During this wind-down period, existing contracts need to be fulfilled, outstanding invoices need to be collected, creditors need to be paid, and assets need to be distributed before final tax filings can be prepared.

- State-level registrations operate independently from federal systems and require explicit closure requests. Closing your IRS payroll account doesn't terminate your state unemployment insurance registration, and filing your final federal return doesn't cancel your sales tax permit. Each state agency maintains its own records with specific forms, final reconciliation filings, and confirmation requirements that all outstanding liabilities have been settled.

- Partnership disputes during dissolution typically stem from undocumented assumptions rather than major legal mistakes. A 2023 study by the American Bar Association found that 62% of partnership conflicts during winddown arise from agreements partners made but never formalized in writing. These disagreements surface around asset valuation, liability allocation, intellectual property rights, and the handling of unexpected debts that arise after initial distributions.

- The IRS can audit partnership returns for three years after filing, and state agencies often have even longer lookback periods. This makes documentation retention critical long after operations end. Dissolution files should include copies of every termination notice sent, every final filing submitted, every account closure confirmation received, and every distribution made to partners to protect against questions that arise years later.

- Business closure addresses this coordination challenge by organizing federal filings, state notifications, vendor cancellations, and final distributions into centralized action plans that reduce the likelihood of overlooked obligations generating future penalties or cleanup work.

Why Dissolving a Partnership Involves More Than Just the IRS

Closing a partnership requires more than filing a final tax return with the IRS. You must pay off debts, notify creditors of the closure, distribute remaining assets, cancel state registrations, close payroll accounts, and end business licenses. The IRS handles federal tax obligations, while state agencies, banks, vendors, and local authorities handle the remainder.

🎯 Key Point: Partnership dissolution involves multiple government agencies and stakeholders - the IRS is just one piece of a much larger puzzle.

"Partnership dissolution requires coordination with federal, state, and local authorities, plus all business creditors and vendors." — Business Dissolution Best Practices

⚠️ Warning: Failing to properly notify all parties can result in ongoing liability and unexpected legal complications even after you think the partnership is officially closed.

What happens when you miss required dissolution steps?

Most founders discover this gap after filing their final Form 1065, assuming the business is closed. Then they receive a notice from their state demanding annual report fees, or a vendor sends an invoice to an inactive bank account.

According to the Small Business Administration's 2023 closure report, 41% of business owners who closed their business without professional help missed at least one required state filing, resulting in penalties or ongoing obligations they thought were finished.

The state doesn't know you stopped operating

The IRS and your state work separately. Filing a final partnership return tells the federal government you're done, but your state considers the partnership active until you file dissolution paperwork. You may receive tax notices, annual report reminders, or franchise tax bills long after ceasing operations. Each state has its own forms, fees, and timelines for officially dissolving a partnership, and missing these steps leaves the business legally open even when it's not operating.

Why do partners disagree during dissolution?

Partnership dissolution gets messier when multiple people are involved. One partner may want to distribute remaining cash immediately, while another insists on holding funds to cover potential liabilities.

Disagreements arise over asset division, outstanding invoices, and collections on unpaid customer accounts. These conflicts slow the process and create friction that hampers coordination.

How can you manage dissolution logistics effectively?

When managing dissolution across multiple agencies and stakeholders, Starcycle's business closure service provides a centralized action plan that tracks federal filings, state notifications, vendor cancellations, and final distributions, so you can see what's complete and what still needs attention.

But before you tackle those logistical steps, you need to understand what dissolution means in tax terms and why the IRS cares about how you close.

Related Reading

- How To Close An LLC

- How To File Business Bankruptcies

- Closing A Company

- How To Close A Business With The Irs

- How Much To Dissolve Llc

What Does It Mean to Dissolve a Partnership?

Dissolving a partnership means formally ending the business relationship and closing its affairs. It's a coordinated sequence: stopping new business, settling obligations, collecting receivables, distributing assets, filing final tax returns, and closing registrations. The decision to dissolve marks the start of the winddown, not its completion.

🎯 Key Point: Partnership dissolution is a process, not a single event. The formal decision to dissolve triggers a systematic wind-down that can take months to complete properly.

"The dissolution process requires careful coordination to ensure all legal obligations are met and assets are properly distributed to avoid future liability." — Business Law Institute, 2024

⚠️ Warning: Many partners mistakenly think dissolution happens immediately after the decision is made. In reality, the legal and financial obligations continue until the wind-down process is fully completed.

Dissolution Phase | Key Activities | Timeline |

|---|---|---|

Decision | Vote to dissolve, notify partners | 1-2 days |

Winddown | Settle debts, collect receivables | 3-6 months |

Final Steps | File tax returns, close registrations | 1-2 months |

Why can't you just stop operations and file paperwork?

A common mistake is treating dissolution like flipping a switch. Partners stop taking clients, file paperwork with the state, and assume they're done. But the partnership remains legally active until all obligations are settled: existing contracts must be fulfilled, outstanding invoices collected, creditors paid, and assets distributed. According to the IRS, partnerships must file a final Form 1065 for the year they cease operations, and that return cannot be filed until all financial activity is complete.

Why the timeline matters

A two-person consulting partnership decides to close. They stop taking new clients but continue operating for six weeks to collect payments, pay vendors, distribute cash, close accounts, and prepare tax filings. Mistakes often occur during this transition period.

Partners who treat closing as a single event often miss steps: filing state paperwork but forgetting to file with the IRS, distributing assets before settling debts, or closing bank accounts before tax obligations are resolved. The process requires coordination across federal and state tax agencies, banks, vendors, clients, and sometimes employees.

When trust breaks down during the wind-down

When a trusted partner acts unilaterally during a shared process, resentment builds quickly. One partner moves money claimed as "owed compensation" without consultation. Another stops answering emails about outstanding debts. These aren't interpersonal problems alone—they're process failures that impede meeting the legal and tax requirements for proper closure.

How can dissolution platforms help coordinate the process?

Platforms like Starcycle help founders manage dissolution as an organized process rather than a chaotic scramble. Custom action plans track federal filings, state notifications, vendor cancellations, and final distributions in one central place.

Instead of juggling spreadsheets and missed deadlines, founders can see what's complete and what still needs attention, reducing the risk of overlooked obligations that create liability.

What does proper dissolution require from partners?

A partnership dissolution requires a series of steps executed in the correct order, with clear documentation and coordinated action between partners who may no longer trust each other.

But knowing what dissolution means doesn't tell you how the IRS expects you to carry it out.

How to Dissolve a Partnership With the IRS

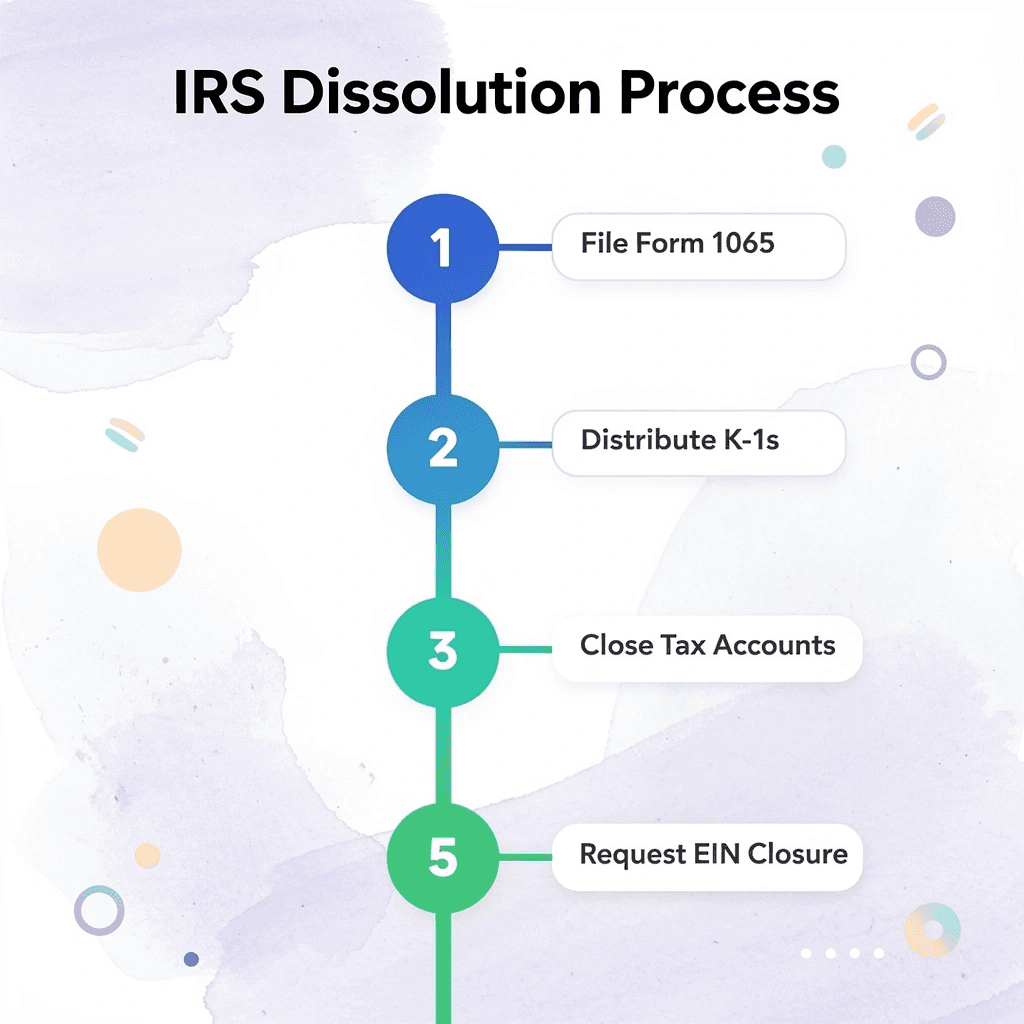

The IRS won't let you simply walk away from a partnership. You must file a final Form 1065, provide final Schedule K-1s to each partner, close any employer tax accounts, settle outstanding tax obligations, and request closure of your business account tied to your EIN. Missing any step can trigger penalties or leave the partnership technically active in the IRS system.

🎯 Key Point: The IRS requires a complete dissolution process - you can't just stop operating and assume you're done. Each step must be completed to avoid ongoing tax obligations.

"Partnerships that fail to properly dissolve with the IRS can face ongoing filing requirements and penalty assessments even after ceasing operations." — IRS Publication 541

⚠️ Warning: Skipping the formal dissolution process can leave your partnership legally active with the IRS, meaning you'll still be responsible for annual filings and potential penalties even though you're no longer in business.

Required Step | Form/Action | Deadline |

|---|---|---|

File the final partnership return | Form 1065 | 15th day of 3rd month after dissolution |

Distribute final statements | Schedule K-1 to all partners | Same as Form 1065 |

Close employment accounts | Contact IRS directly | Within 30 days |

Settle tax obligations | Pay outstanding balances | Before final filing |

Request EIN closure | Written request to IRS | After all obligations are met |

What form do you need to file as your final partnership tax return?

Form 1065 is the partnership's final official message to the IRS about income, deductions, gains, and losses. Check the "Final Return" box near the top of the form to notify the IRS not to expect another filing. Most calendar-year partnerships must file by the 15th day of the third month after the tax year ends. If you dissolved in October, you still report through December 31 and file by March 15 of the following year.

What happens if you miss filing your final partnership return?

Missing this filing leaves your partnership in administrative limbo. The IRS continues treating it as active and expects returns that never arrive. Penalties accumulate monthly for late filing, even if there is no business activity. Many founders assume that stopping operations means ending tax obligations, only to receive IRS notices months later demanding returns for a closed business.

What information must be included on final Schedule K-1s?

Every partner needs a final Schedule K-1 showing their share of income, deductions, gains, losses, and credits for the final year. The IRS requires you to check the "Final K-1" box on each form. Partners use these numbers when filing their individual tax returns.

Why does accuracy in K-1 allocations prevent future disputes?

If your allocations don't match the partnership agreement or the final distributions, you create tax problems that carry over to partners' personal returns. Accuracy prevents future disputes. When partnerships dissolve during difficult times, partners scrutinize every number. Misaligned allocations—whether they diverge from actual asset distributions or contractual split terms—create a foundation for conflict that extends beyond dissolution.

What employment tax obligations must be completed before closing?

If your partnership had employees, you cannot close until final wages are paid, all federal tax deposits are made, and final employment tax returns are filed. This typically includes Form 941 (quarterly payroll taxes), Form 940 (unemployment taxes), and W-2s for each employee. The IRS treats employment tax obligations as continuing responsibilities even when a business is shutting down.

How do quarterly deadlines affect the dissolution timeline?

You need to process final paychecks, calculate and deposit final payroll taxes, and file final returns before the IRS will consider your employer account closed. Quarterly filing deadlines often don't align with your dissolution timeline.

Platforms like Starcycle track overlapping deadlines across tax filings, payroll obligations, and state requirements, converting a confusing sequence of due dates into a single action plan.

What tax obligations must be resolved before closing your business account?

The IRS won't fully close a business tax account until all required returns are filed and outstanding obligations—including unpaid income taxes, payroll taxes, penalties, and accrued interest—are addressed.

Ignoring unpaid taxes doesn't eliminate them: collection activity continues, penalties accumulate, and notices keep arriving at an unmonitored address.

How do you notify the IRS that your partnership has ceased operations?

Your EIN never gets canceled, but the IRS can close or deactivate the business account connected to it. Send a written request that includes the partnership's legal name, EIN, business address, and reason for closure.

This tells the IRS that your partnership has ceased operating and should not file future business returns.

What other requirements remain after federal tax closure?

Completing IRS requirements addresses only your federal obligations. You still need to handle state dissolution filings, cancel licenses, make final distributions, and maintain records properly.

Federal tax closure is important but represents only one part of the broader operational closure that partnerships must navigate.

Related Reading

- IRS Closing A Business

- Involuntary Dissolution Of Llc

- How To Liquidate A Company

- How To Dissolve A Nonprofit

- Irs Cancel Ein

- Notice Of Dissolution

- How To Wind Down A Company

The Non-IRS Steps Many Partnerships Overlook

State dissolution filings represent the most frequently missed requirement when partnerships close. After filing a final Form 1065 and issuing final K-1s to partners, the business remains legally active in state records unless you submit formal dissolution paperwork to the Secretary of State or similar agency. Without proper cancellation, annual report obligations continue, franchise tax bills keep arriving, and the entity faces administrative penalties for non-compliance.

🔑 Key Takeaway: Filing federal tax returns doesn't automatically dissolve your partnership at the state level—you must take separate action to avoid ongoing compliance obligations.

"State dissolution filings represent the most frequently missed requirement when partnerships close, leaving businesses exposed to continued penalties and obligations." — Tax Foundation Business Compliance Survey

⚠️ Warning: Many partnerships assume that filing their final federal returns completes the dissolution process, but state-level requirements operate independently and can create costly surprises.

State-Level Tax Accounts Need Separate Closure

State payroll accounts, sales tax permits, and withholding registrations operate independently from federal systems. Closing your IRS payroll account does not stop your state unemployment insurance registration, and filing your final federal return does not cancel your sales tax permit. Each state agency requires explicit closure requests with specific forms, final reconciliation filings, and confirmation that all outstanding liabilities have been paid. A consulting partnership in Oregon discovered this gap eight months after its dissolution, when the state sent a delinquency notice for unfiled quarterly reports on a sales tax permit it believed had closed automatically.

What happens to business licenses when you stop operating?

Professional licenses, health permits, city business licenses, and industry-specific registrations renew on fixed schedules unless formally canceled. Stopping operations does not automatically end them. Renewal fees continue to accrue, and some areas impose penalties for operating without valid licenses, even when you're no longer doing business.

How do vendor agreements and subscriptions affect business closure?

Most partnerships maintain vendor agreements, software subscriptions, insurance policies, lease commitments, and utility accounts that renew automatically unless canceled with proper notice. These continue to bill and renew until you actively stop them, regardless of your business status.

Review every recurring expense and contract with renewal language. Some require 30 days' notice; others, 60 or 90 days. Missing these windows could lock you into another term or trigger early termination fees that exceed the cost of maintaining the service until its natural end date.

Platforms like Starcycle help founders track these obligations through centralized checklists and contract management tools, reducing time spent hunting renewal dates and cancellation procedures across vendor relationships.

What banking obligations must you address before dissolving?

Business checking accounts, savings accounts, merchant processing relationships, and payment platform accounts should close only after all obligations are settled and final distributions are complete. Leaving accounts open risks unexpected charges months later and maintenance fees on dormant accounts.

How do you properly close business financial accounts?

Close accounts formally, obtain written confirmation, and retain those records with your dissolution documents. The same applies to business credit cards, lines of credit, and financing relationships that may generate statements or reporting obligations even after balances reach zero.

Closing accounts and filing paperwork address only the mechanics, not the sequence that prevents the mistakes most partnerships make during their final months.

What a Proper Partnership Winddown Looks Like

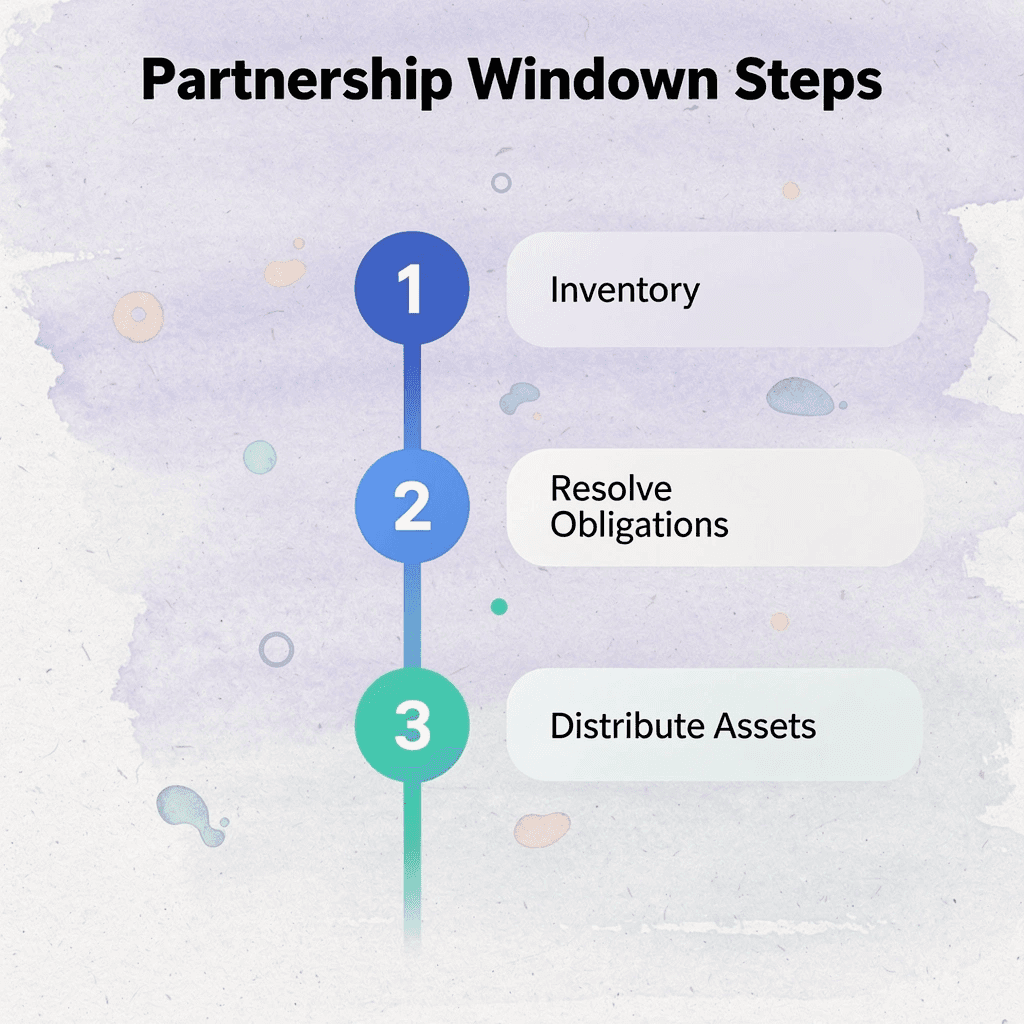

A clean partnership winddown depends on doing things in the right order. Most partners get the steps right but do them in the wrong order, creating problems that could have been avoided. The correct order is: inventory first, resolve obligations second, distribute third, file fourth, and verify last.

Step | Action | Key Focus |

|---|---|---|

1. Inventory | Document all assets and liabilities | Complete financial picture |

2. Resolve Obligations | Pay debts and settle contracts | Clear all commitments |

3. Distribute | Allocate remaining assets to partners | Fair division per agreement |

4. File | Submit dissolution paperwork | Legal compliance |

5. Verify | Confirm all steps completed | Final validation |

🎯 Key Point: Following the proper sequence prevents costly mistakes and ensures all partners receive their fair share without legal complications.

"80% of partnership disputes during dissolution stem from improper sequencing of winddown activities, not disagreements over the actual steps." — Business Partnership Research Institute, 2023

⚠️ Warning: Skipping the inventory step or rushing to distribute assets before resolving all obligations can expose partners to personal liability and create tax complications that persist long after dissolution.

Start With a Complete Operational Freeze

Before doing any administrative work, stop the partnership's operations by documenting every active commitment, open contract, pending invoice, recurring subscription, and unfinished customer obligation. Record what the business owes, what it's owed, and what it's promised to deliver. Skipping this step risks discovering forgotten liabilities weeks after distributing final assets, forcing partners to contribute personal funds to cover obligations they thought were settled. The freeze creates a snapshot that prevents surprises from emerging after you've moved money or filed paperwork.

Resolve Partner Disagreements Before Filing Anything

The dissolution agreement should address every potential conflict before filing: how to value the remaining assets, who assumes which liabilities, how to handle intellectual property rights, whether anyone continues to use the business name, and what happens if unexpected debts surface later. According to a 2023 study by the American Bar Association, 62% of partnership disputes during dissolution stem from assumptions partners made but never documented. Document all agreements in writing, even those that feel obvious.

Why should you shut down systems in reverse order of dependency?

Turn off systems in the opposite order of their dependencies. Cancel software subscriptions before closing the bank account that funds them. End vendor relationships before canceling the credit card they bill to. Close the payroll account after processing final payments, not before.

When a California partnership closed its business bank account before canceling its registered agent service, the annual fee bounced, the service lapsed, and they missed a state compliance notice that triggered penalties. Map your dependencies first, then work backward systematically.

How can structured workflows simplify the dissolution process?

Most business closings follow predictable patterns that don't require legal help when you have clear guidance and organized workflows. Our business closure solution provides step-by-step action plans that guide founders through the exact sequence of tasks, manage contract endings, and organize dissolution documents.

This approach compresses what used to take months of expensive legal coordination into a manageable, founder-led process, often saving thousands of dollars and shortening timelines by weeks.

Document Everything, Then Document Again

Create a dissolution file containing copies of every termination notice, final filing, account closure confirmation, and distribution to partners. Take photos of final meter readings for physical locations. Save screenshots of online account cancellations and certified mail receipts for creditor notifications. The IRS can audit partnership returns for three years after filing (longer if income was substantially understated), and state agencies often have longer lookback periods. A well-organized dissolution file remains accurate years later, when memory fades.

But documentation alone doesn't prevent the most common winddown failure, one that catches even methodical partners off guard.

How Starcycle Helps Founders Navigate Partnership Dissolutions With More Clarity

Understanding how to dissolve a partnership is one thing. Executing the process correctly is another. After partners decide to close the business, significant work remains: tax filings, account reviews, obligations to resolve, documentation to coordinate, and closure requirements to track across multiple agencies and service providers. Our Starcycle platform helps streamline this administrative burden by centralizing documentation and tracking closure requirements in one place.

🎯 Key Point: Partnership dissolution involves extensive administrative work that extends far beyond the initial decision to close, requiring careful coordination across multiple stakeholders and agencies.

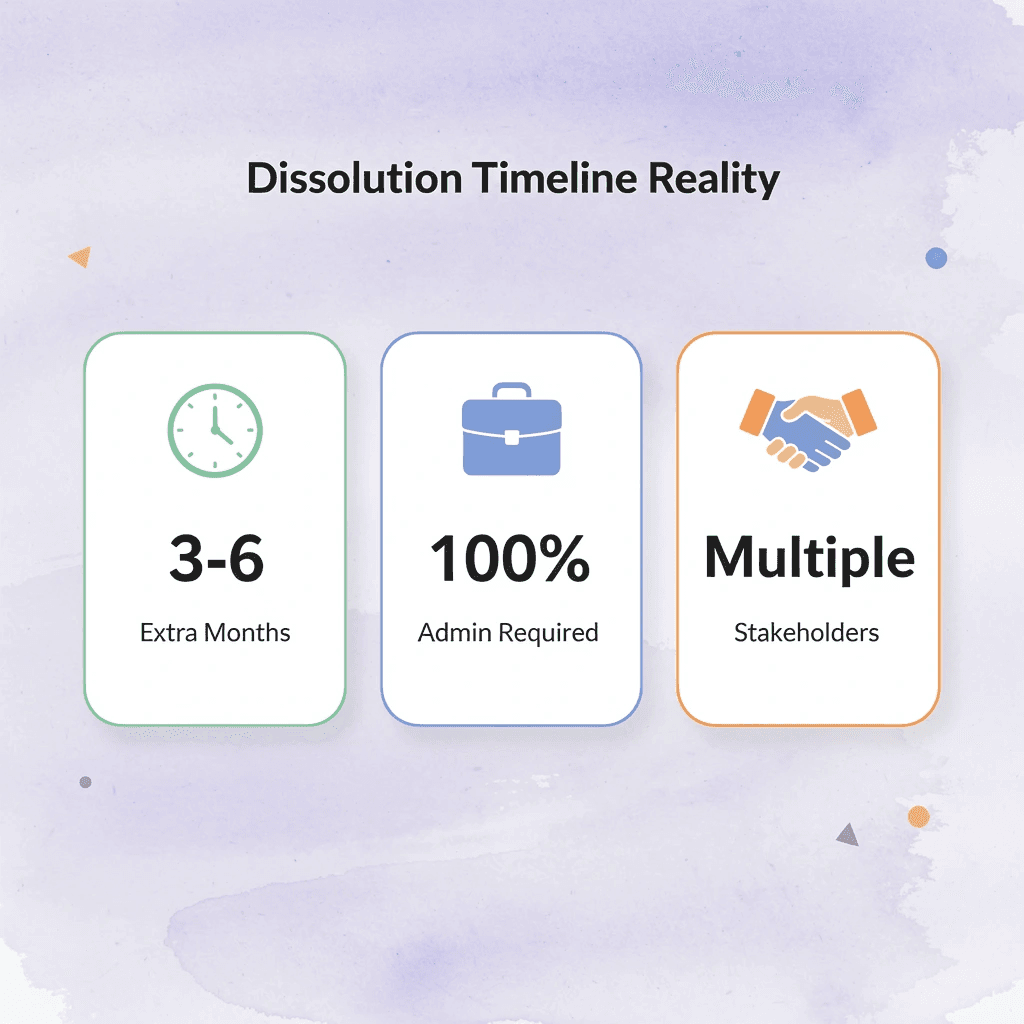

"The practical execution of partnership dissolution often takes 3-6 months longer than founders anticipate due to complex administrative requirements." — Business Dissolution Research, 2023

💡 Tip: Use centralized documentation platforms to avoid missing critical closure requirements that could result in ongoing legal or tax obligations for dissolved partnerships.

What operational burden do most founders underestimate?

Tax professionals and attorneys provide guidance, but founders remain responsible for properly closing partnerships. Identifying unresolved obligations is critical: partnerships may retain tax responsibilities, active registrations, payroll accounts, vendor agreements, subscriptions, banking relationships, and documentation requirements even after business activity ceases. Each represents a potential loose end that can trigger future notices, penalties, or cleanup work if overlooked.

Why do critical dissolution tasks slip through the cracks?

Most founders manage dissolution through spreadsheets and email because it's familiar. As closure tasks multiply across state agencies, banks, vendors, and service providers, critical items slip through the cracks: deadlines get buried, documentation fragments across systems, and what seemed manageable becomes an ongoing source of anxiety months after partners believed everything was finished. Starcycle organizes these responsibilities into a clearer closure workflow with tailored action plans, contract management tools, and document organization that reduce the likelihood of overlooking important steps.

Documentation coordination that prevents future problems

When a partnership ends, you need to handle tax records, dissolution filings, account closures, partner documentation, financial records, and agency communications. A structured dissolution plan consolidates these materials and coordinates closure tasks. Our Starcycle platform simplifies the administrative work and provides visibility throughout the winddown process.

Which administrative gaps most often cause partnership closures?

Most partnership closure problems stem from small administrative gaps rather than major legal mistakes: an account never formally closed, a missed filing, an active registration, or documentation that's hard to find later. These issues lead to future notices, penalties, confusion, and cleanup work long after partners thought the business had been dissolved.

According to Entrepreneur UK, many startups that grew from $0 to $6 million in ARR in 14 months struggled with administrative closure at the end of operations, demonstrating how operational complexity persists regardless of growth trajectory.

How does proper dissolution planning help founders move forward?

Ending a partnership is often more than handling paperwork; it's a significant change for the founders. A clear process lets founders close business chapters with care, stopping obligations, filings, and loose ends from resurfacing later.

But even with perfect documentation and careful planning, one final step determines whether you move forward cleanly.

Sign up to Make your Business Closure Process Easier

You can track every requirement in a spreadsheet and set calendar reminders, yet months later discover that a state registration remained active or a vendor account kept billing. The challenge isn't knowing what to do—it's coordinating everything across agencies, deadlines, and documentation requirements without letting something slip through.

🎯 Key Point: Even the most organized business owners can miss critical closure steps when managing everything manually across multiple platforms and agencies.

"The challenge isn't knowing what to do—it's coordinating everything across agencies, deadlines, and documentation requirements without letting something slip through."

Get a quote from Starcycle to organize your partnership winddown, identify unresolved obligations, and navigate closure with confidence. Our platform tracks filings, manages contract terminations, and documents each step so you can finish strong without administrative loose ends resurfacing later.

💡 Tip: Professional closure management ensures nothing gets overlooked during the complex process of winding down your business operations.