How to Close an LLC: A Step‑By‑Step Guide for Founders

Learn how to close an LLC with Starcycle's step-by-step guide for founders. Get the exact process, forms, and timeline for a proper dissolution.

Starting an LLC takes energy and vision, but sometimes business owners need to move on from their ventures. Whether the company didn't meet expectations or entrepreneurs are pursuing new opportunities, properly dissolving the entity prevents future tax obligations and compliance penalties. Skipping essential steps during dissolution can create legal complications that persist long after owners believe the process is complete.

State requirements for LLC dissolution vary significantly, and navigating the paperwork without guidance often leads to costly oversights. Business owners must file articles of dissolution, settle outstanding debts, cancel licenses, and complete final tax filings to fully close their companies. Professional guidance can streamline this complex process and help entrepreneurs avoid common pitfalls during business closure.

Table of Contents

- Closing an LLC Is Not Just “Shutting It Down”

- What It Actually Means to Close an LLC

- 7 Step-by-Step Process to Close an LLC

- Where Most Founders Get It Wrong

- The Hidden Costs of Doing It Wrong

- How to Close an LLC Efficiently and Move On

- How Starcycle Helps You Close Your LLC the Right Way

- Sign up to Make your Business Closure Process Easier

Summary

- Closing an LLC requires formal dissolution paperwork filed with the state, not just ceasing operations. The IRS reports that missed tax filings can trigger penalties of $220 per partner per month for multi-member LLCs, and these penalties accumulate even when the business earns nothing. Dormant LLCs continue owing annual state fees, franchise taxes, and required filings until properly dissolved through official channels.

- Final tax returns marked as complete are mandatory regardless of revenue. The IRS expects a final return for the year you dissolve, and failure to file triggers compounding penalties that persist long after operations stop. State tax agencies operate similarly, requiring confirmation that all accounts are settled before considering an LLC truly closed.

- Proper creditor notification creates a legal claims deadline, typically 90 to 120 days, after which creditors lose the right to pursue the LLC. Skipping this step or distributing assets to members before paying creditors can expose members to personal liability for unpaid debts. Most states require that creditor payments be prioritized over member distributions during the winding-up period.

- Research on dissolution platforms shows that proper closure saves businesses an average of $2,500 to $5,000 in penalties and fees when all requirements are addressed in the correct order. The IRS reports that over 70% of businesses that close informally face compliance issues within three years, often because founders assumed completion without verification from state agencies or tax authorities.

- Incomplete closures create lasting founder profiles that include unresolved tax liens, state penalties, or outstanding judgments. These records stay attached to individuals even when the business itself is inactive, affecting standing with future partners, investors, or lenders. Clean closure protects the ability to move forward without explaining or repairing past mistakes.

- Platforms like Starcycle address this by organizing every required step across state agencies, tax authorities, and vendor contracts into a single verified timeline, compressing what typically takes months into weeks while maintaining full visibility over every closure point.

Closing an LLC Is Not Just “Shutting It Down”

You can't close an LLC by walking away. The legal entity continues to exist until you formally dissolve it with the state, even if you've stopped operating. Inactivity doesn't pause your obligations.

🔑 Key Point: Simply abandoning your LLC doesn't make it disappear - the legal entity remains active and continues to generate obligations.

The consequences are real and measurable. According to the IRS (2023), missed tax filings can trigger penalties of $220 per partner per month for multi-member LLCs. Dormant LLCs still owe annual state fees, franchise taxes, and required filings annually. Penalties accumulate even if the business earns nothing, and founders often discover years later that what felt like a closed chapter has been quietly building debt.

"Missed tax filings can trigger penalties of $220 per partner per month for multi-member LLCs." — IRS, 2023

⚠️ Warning: Dormant LLCs continue accumulating fees and penalties even with zero revenue - ignoring dissolution can cost thousands in unexpected debt.

Why does the business feel closed but legally remain open?

From a business standpoint, the company is defunct: no customers, no activity, no revenue. From a legal standpoint, however, nothing has changed. The business entity remains tracked, subject to regulatory requirements, and creates ongoing obligations.

States charge yearly fees until you submit dissolution paperwork. Missing deadlines incurs penalties and risks administrative dissolution of your LLC, leaving you with accumulated fees and a damaged compliance record.

What makes dissolution requirements so confusing?

This confusion exists because dissolution is rarely explained clearly. Most guidance focuses on starting a business, not closing one. Founders assume that if nothing is happening, nothing is required. But inaction creates the problem.

One founder described the realization: "A lot of people dissolve their LLC and think they're done. Nope." They discovered a separate final filing deadline, distinct from regular tax cycles, that they hadn't known existed.

What does inactive status actually mean for your LLC?

"Inactive" describes how a business operates, not its legal status. You can stop working, earning, and marketing, but the LLC remains a registered entity with filing status and compliance deadlines that continue. Many people mistakenly believe dissolution occurs automatically or that ceasing operations closes the business. This misunderstanding creates problems.

What steps are required to formally close an LLC?

Closing an LLC requires formally ending the business by filing articles of dissolution, paying off debts, canceling licenses, and completing final tax returns. Skipping any step can result in penalties, tax notices, and legal problems that may persist for years.

But what does that process look like when you break it down step by step?

What It Actually Means to Close an LLC

Closing an LLC means formally ending its legal existence by notifying the state, the IRS, and other agencies. Until you complete this process, the LLC remains legally alive with all its responsibilities intact.

🎯 Key Point: Your LLC continues to exist legally until you complete the entire dissolution process with all required agencies.

"An LLC remains legally active and subject to ongoing compliance requirements until formal dissolution is completed with state authorities." — Business Formation Expert

⚠️ Warning: Many business owners assume their LLC is automatically closed when they stop operations, but this leaves them vulnerable to ongoing tax obligations and potential penalties.

Two things must happen together

First, file dissolution paperwork with your state, usually called Articles of Dissolution or a Certificate of Cancellation. The state must accept, process, and mark your LLC as dissolved in its records. Until then, you remain responsible for annual reports, franchise taxes, and other state-level requirements.

Second, settle everything the business owes: pay creditors, notify claimants, distribute remaining assets per your operating agreement or state default rules, and close contracts. Many founders skip this step when no money remains, but creditors can still make claims and potentially reach members personally if dissolution was not handled properly.

Tax closure is not optional

You must file final tax returns with the IRS, your state tax authority, and any local agencies that require them. Mark these returns as final and close your EIN account to prevent future filing expectations.

What happens if you skip final tax filings?

According to the IRS (2024), businesses that fail to file final returns or notify the agency of closure continue receiving notices, penalties, and compliance demands long after operations have stopped. Founders often discover this years later when a tax lien appears, or a notice arrives for a business they thought was closed.

How does proper closure protect your future?

Proper closure protects you from future claims, stops fees from accumulating, and clears the path forward. Platforms like Starcycle help founders navigate dissolution faster by organizing documents, tracking state-specific requirements, and building step-by-step action plans that account for tax obligations, creditor notifications, and final filings.

An LLC is closed only when the state recognizes it as dissolved, and no obligations remain. Anything short of that leaves the door open.

What does that process look like when broken into specific, sequential steps?

Related Reading

- How To Close An LLC

- How To File Business Bankruptcies

- How Much To Dissolve an LLC

- Involuntary Dissolution Of Llc

- Closing A Company

- How To Close A Business with the IRS

- How To Dissolve A Corporation

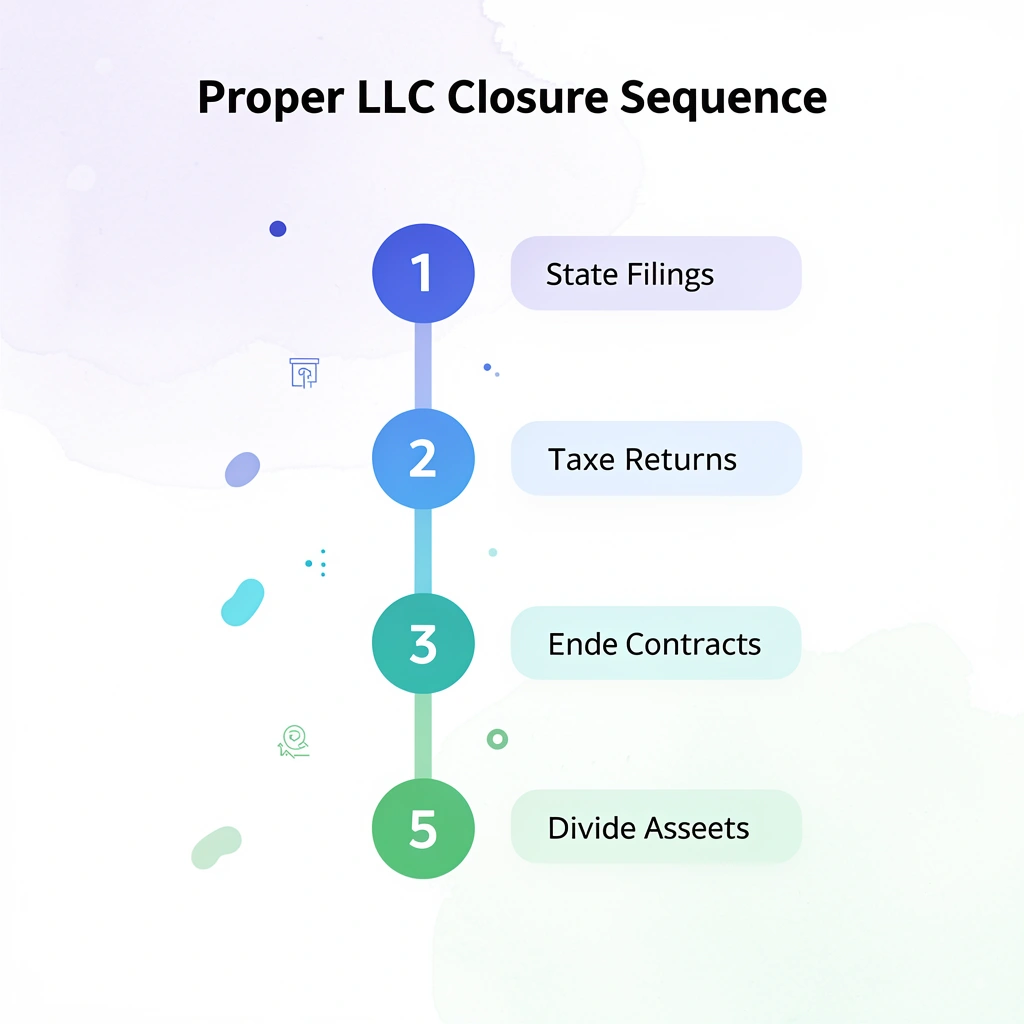

7 Step-by-Step Process to Close an LLC

The dissolution process follows a fixed sequence that cannot be altered or abbreviated. Skipping steps creates legal exposure that persists long after closure. Our Starcycle platform helps you track and complete each required step systematically, reducing the risk of overlooked compliance requirements.

🎯 Key Point: Legal liability doesn't automatically disappear when you stop operating—it requires proper dissolution procedures to be fully terminated.

"Improper LLC dissolution can leave business owners personally liable for debts and obligations years after they believed the company was closed." — Business Law Institute, 2024

⚠️ Warning: Informal closure without following the legal dissolution process leaves you vulnerable to ongoing tax obligations, creditor claims, and regulatory penalties that can surface months or years later.

1. Review Your Operating Agreement

Your operating agreement sets the internal rules for dissolution, defining who approves closure, how votes are counted, and how assets are distributed. If more than 50% of the LLC members must vote to dissolve, that threshold matters. Without an operating agreement, your state's default LLC statutes apply instead, which may require unanimous consent or impose distribution rules you never intended.

The agreement creates the legal foundation for closure. Dissolving without following its terms exposes you to member challenges, creditor claims of improper distribution, and a contestable dissolution process.

2. Vote to Dissolve

Someone must formally decide that the LLC is ending. Single-member LLCs require written documentation kept with business records, while multi-member LLCs typically need a vote based on ownership percentages or operating agreement terms.

Record the decision in meeting minutes or a written consent form. This document proves the dissolution was authorized and becomes important if anyone later questions the closure's legitimacy.

3. File Articles of Dissolution

Submit Articles of Dissolution (sometimes called a Certificate of Dissolution or Certificate of Cancellation) to the Secretary of State to officially dissolve your LLC. Most states require filing within 60 days of filing your certificate of dissolution, or you risk penalties and ongoing obligations.

Until the state processes this filing, your LLC remains active, so annual reports, franchise taxes, and registered agent fees continue to accrue. Filing fees range from $50 to $500, depending on the state, with processing times from a few days to several weeks.

4. Settle Outstanding Debts

After filing dissolution paperwork, you enter the "winding up" period to pay creditors, close contracts, and resolve remaining obligations. Most states require you to prioritize creditors before distributing assets to members. If you distribute assets too early, creditors can pursue members personally for unpaid debts.

How do you notify creditors during dissolution?

Tell creditors you know about in writing. Many states also require you to publish a notice in a local newspaper to alert unknown creditors. This creates a deadline for claims, usually 90 to 120 days. After this deadline passes, creditors lose the right to pursue the LLC. If you skip this notification, creditors can attempt collection indefinitely.

What happens if the LLC can't pay all its debts?

Closing doesn't mean walking away from vendor invoices or lease obligations; those debts follow you unless properly settled or discharged. If the LLC lacks funds to pay everyone, state law dictates the priority order, and members may need to contribute additional capital to cover shortfalls.

5. Cancel Licenses, Permits, and Accounts

Every active license, permit, or account tied to the LLC must be formally closed. Business licenses, sales tax permits, employer accounts, vendor agreements, and bank accounts remain open until you cancel them. A sales tax permit obligates you to file quarterly returns even without sales activity. A business bank account with automatic debits can overdraw and generate fees.

How should you contact agencies and vendors for cancellation?

Contact each agency or vendor individually. Some require written notice, others accept online cancellations. Keep confirmation records for everything; proof of cancellation is your only defense if a state agency later claims you owe fees.

What forgotten accounts might this process reveal?

This step identifies forgotten subscriptions, auto-renewing services, and inactive accounts that drain funds or create compliance issues.

6. File Final Tax Returns

Tax closure is required and often the most time-sensitive part of dissolving your business. The IRS requires a final federal tax return marked "FINAL" for the year you dissolve. If your LLC has employees, you must file final employment tax returns and send final W-2s or 1099s. State tax agencies require final income tax, sales tax, and franchise tax returns.

What is a tax clearance certificate, and why do you need it?

Some states issue a tax clearance certificate after you pay all your taxes. This certificate confirms that the state has no outstanding claims against the LLC. Without it, dissolution may not be considered complete, and you could remain responsible for future tax bills.

What happens if you miss final tax filing deadlines?

If you miss filing your final tax return, you will face rapidly escalating penalties. The IRS charges $220 per partner each month for late partnership returns, and states add their own penalties on top of that.

7. Distribute Remaining Assets

Once debts and obligations are paid off, any remaining cash or property goes to members based on the ownership percentages listed in the operating agreement, or, if no agreement exists, according to state law.

Write down the distribution with a final accounting that shows all money coming in, all money going out, and each member's share. This protects everyone if questions arise about whether the dissolution was handled fairly.

What happens if assets remain after distribution?

After distribution, the LLC should have zero assets and zero liabilities. Anything left unresolved keeps the entity technically active.

Founders often discover unknown obligations during this process. Platforms like business closure help by organizing the full scope of tasks up front, tracking deadlines across state and federal agencies, and flagging overlooked steps, such as creditor notices or tax clearances, before they become costly problems. Our Starcycle platform ensures nothing falls through the cracks during wind-down.

What common mistakes should you avoid?

But even with the right process, founders make predictable mistakes that undo this work.

Related Reading

- IRS Closing A Business

- Shutting Down A Company

- How To Wind Down A Company

- How To Dissolve A Nonprofit

- Notice Of Dissolution

- Irs Cancel Ein

- How To Liquidate A Company

Where Most Founders Get It Wrong

The biggest mistake is assuming that no business activity means the company is legally closed. Founders stop taking new customers and cancel subscriptions, but the LLC stays registered, continues accumulating obligations, and remains legally theirs.

🚨 Warning: Just because you've stopped operating doesn't mean your business has stopped existing in the eyes of the law. Your LLC registration continues to generate legal responsibilities and financial obligations that can come back to haunt you.

"An inactive business entity can still accumulate tax penalties, filing fees, and compliance violations that the founder remains personally responsible for." — Small Business Administration Guidelines

💡 Key Point: Dormant LLCs continue to rack up annual fees, tax obligations, and regulatory requirements even when they're generating zero revenue. This silent accumulation of debt is what catches most founders completely off guard.

The Illusion of "Done"

When the product shuts down and the last employee leaves, it feels finished. That emotional closure creates a dangerous assumption: the business must be closed as well. But state agencies don't track whether you're making sales or answering emails—they track whether you've filed dissolution paperwork. Until that happens, you remain liable for annual reports, franchise taxes, and registered agent fees. One founder stopped operations in March, assuming everything would resolve itself. By November, the state had assessed $800 in penalties for missed filings on a business that hadn't earned a dollar in eight months.

Tax Obligations Don't Fade with Revenue

Final tax returns get delayed or ignored when there's no money coming in. The logic seems sound: no income, no taxes, no urgency. But the IRS doesn't see it that way. They expect a final return, properly marked as such, regardless of revenue. Miss that filing, and penalties accumulate. State tax agencies operate identically—they want confirmation that you've settled up and closed your accounts. Without it, they assume you're still active and send notices that turn into liens faster than most people expect.

The Subscription Trap

Operational loose ends pile up quietly. A domain auto-renews. A payment processor keeps charging its monthly fee. A business bank account incurs maintenance charges. Individually minor, together they drain hundreds of pounds over months, while you assume the business is dormant.

Some vendor agreements include automatic renewal clauses or termination-notice requirements buried in the fine print. Founders discover these obligations after moving on mentally, creating unexpected costs that structured offboarding could prevent.

What tools help identify all closure obligations upfront?

The business looks closed from where you're standing, but legally it's still breathing. Platforms like business closure surface hidden obligations immediately, organizing every required step across state agencies, tax authorities, and vendor contracts into a single timeline.

That visibility transforms an endless checklist into a finite project with a clear endpoint. But even when founders know what needs to happen, the financial consequences of mistakes often don't surface until much later.

The Compound Effect

Mistakes in LLC closure build up quietly, often surfacing months or years later. According to Gartner, poor data quality costs organizations an average of $12.9 million annually. While that figure applies primarily to large operations, the same principle holds for small business closures: incomplete records, missed filings, and unresolved obligations create mounting financial problems.

Personal Liability Creep

One of the most overlooked risks is how improperly closed LLCs can erode the liability protection you formed the entity to secure. If you skip formal dissolution and leave obligations unresolved, creditors or claimants may argue that the LLC was never properly maintained or closed, potentially piercing the corporate veil. This exposes personal assets, credit, and your ability to start something new to disputes you thought were behind you.

The Attention Tax

Beyond dollars, there is the cost of distraction. Every notice, penalty letter, and follow-up call pulls you away from what you're building next. Founders who close incorrectly often describe lingering anxiety that something might surface later. That mental load compounds as momentum is regained in a new venture. Platforms like business closure eliminate that uncertainty by organizing every required step into a clear, trackable timeline.

The Reputational Ripple

Incomplete closures damage your reputation with future partners, investors, and lenders. Unresolved tax liens, state penalties, and outstanding judgments become part of your founder profile, even if the business is inactive. A clean closure protects your ability to move forward without explaining or fixing past mistakes.

The question becomes how to avoid these costs altogether.

How to Close an LLC Efficiently and Move On

Efficiency in closing an LLC means doing the right steps in the right order so nothing pulls you back later. Sequence tasks so each one simplifies the next, and centralize documentation to prove closure when questions surface months or years down the line. The goal is finality, not filing paperwork.

🎯 Key Point: The most common mistake is rushing through dissolution without proper sequencing, which can lead to unexpected liabilities or tax complications appearing years after you think the LLC is closed.

"Proper LLC dissolution requires completing all steps in the correct sequence to avoid future legal and financial complications that can persist for 3-7 years after filing." — Small Business Administration Guidelines

⚠️ Warning: Skipping the documentation centralization step is a critical error that leaves you vulnerable when the IRS, creditors, or state agencies come asking for proof of proper closure 2-5 years later.

Treat Closure as a Project, Not a Task

Plan what needs to happen in legal, financial, and operational areas before you start. When everything is visible, you avoid leaving gaps that turn into follow-ups, notices, or fees. A common trap is believing something is handled because you started it, only to discover it was never completed. Closure requires confirmation at every step. If you filed dissolution paperwork but never closed your business bank account, you will keep paying monthly fees until someone notices.

Sequence Matters More Than You Think

Handle internal approval and documentation first, then file dissolution with the state. Next, wind down obligations: settle debts, close accounts, and complete final tax filings. Each step builds on the previous one. If you close your bank account before paying final vendor invoices, you create delays that take weeks to untangle. If you file final tax returns before distributing remaining assets, you may need to amend those returns later.

Why should you keep all dissolution documents organized?

Keep filings, confirmations, tax submissions, and account closures in one place. If a state agency sends a notice two years later or you need proof of closure for a future investor, you won't have to rebuild the process from memory or scattered email threads. One folder—digital or physical—with every confirmation email, stamped filing, and closure receipt eliminates uncertainty.

How can technology streamline the dissolution process?

Spreadsheets and email work until complexity increases: multiple contracts to cancel, state filings across different states, and federal and state tax obligations. Important deadlines get buried, confirmations are lost, and visibility disappears. Our Starcycle platform consolidates the entire process in one place, with custom action plans, contract tracking, and document organization, compressing what typically takes months into weeks while maintaining full visibility at every stage.

Confirm Completion, Do Not Assume It

Be deliberate about closure points. Whether it's a canceled subscription, closed bank account, or filed return, confirm each item is completed, not started. Call the bank to confirm the account is closed and no automatic charges remain. Verify that the state accepted your dissolution filing, the IRS accepted your final return, and your EIN is marked inactive. Assumptions create the gaps that pull you back into something you thought was finished.

But even when you follow every step, the real test is whether the process you built can survive later scrutiny.

Related Reading

- Liquidation Vs Bankruptcy

- Close Corporation Taxation

- Llc Termination Vs Dissolution

- Company Liquidation Process

- Startup Shutdown

- How Much Does It Cost To Close an LLC

- How To Tell Investors That You're Shutting Down

- How To Dissolve A Partnership With The Irs

- Dissolving In Europe

- Dissolving In Canada

How Starcycle Helps You Close Your LLC the Right Way

Closing an LLC means doing every step the right way, in the right order. You're managing state filings, final tax returns, ending contracts, closing accounts, and dividing assets across different systems and timelines. One missed detail can become a compliance problem months later.

That's the gap Starcycle was built to fill.

🎯 Key Point: LLC dissolution involves multiple interconnected steps that must be completed in the proper sequence to avoid future legal and financial complications.

⚠️ Warning: Missing even one step in the LLC closure process can result in ongoing liability, unexpected tax obligations, or compliance issues that surface long after you think your business is closed.

"One missed detail during LLC dissolution can create compliance problems that persist for months or even years after the intended closure date." — Business Formation Experts

A Complete Process, Not Just a Checklist

Most founders approach LLC closure as a simple mental checklist: file the dissolution paperwork, close the bank account, and submit the final tax returns. However, these steps have dependencies, timing requirements, and verification needs that aren't obvious until you're already in the process.

Why does proper dissolution order matter for your business?

According to research on dissolution platforms, proper dissolution can save businesses an average of $2,500 to $5,000 in penalties and fees when all requirements are handled in the correct order.

Starcycle provides structured guidance that accounts for these dependencies. Instead of wondering whether you filed your state dissolution before or after closing contracts (it matters), our platform helps you follow a step-by-step plan that ensures each step builds properly on the last. Starcycle tracks what's been completed, what's pending, and what verification you still need.

Verification That Actually Confirms Closure

Finishing a step and ensuring it was done correctly are two different things. You can send Articles of Dissolution to the state, but that doesn't mean the filing was accepted or your LLC is marked as dissolved in their system. You can close a bank account online, but automatic debits may still be set up.

The IRS reports that over 70% of businesses closing informally face compliance issues within three years, often because founders assumed completion without confirmation.

How does Starcycle ensure proper verification?

Starcycle builds verification into the process. You're prompted to confirm that the state accepted your dissolution filing, that the IRS marked your EIN inactive, and that no outstanding debts remain with vendors or creditors. This ensures that when you're done, you're truly done—not quietly accumulating legal obligations in the background.

Clarity When You Need It Most

Closing a business is hard: you're ending something you created. Starcycle removes uncertainty by giving you a clear path from decision to completion, with every requirement accounted for and every loose end tied off.

The outcome is a fully closed entity, with documentation to prove it, so you can move forward without concern about future complications.

Sign up to Make your Business Closure Process Easier

If you're not sure whether your LLC is closed, you're not alone. Starcycle removes that confusion by providing a clear path, a custom action plan, and confirmation at every step.

Sign up to get a quote that shows exactly what your closure needs, how long it will take, and what it costs. You'll see the full scope upfront, so you can finish this chapter and move forward without loose ends.

🎯 Key Point: Don't leave your LLC closure to chance - Starcycle's systematic approach ensures nothing falls through the cracks during your business wind-down process.

"Clear documentation and step-by-step confirmation eliminate the uncertainty that keeps business owners awake at night wondering if their closure was truly complete." — Business Closure Best Practices, 2024

💡 Tip: Getting an upfront quote means no surprises later - you'll know your total investment and timeline before committing to the closure process.