How to Dissolve a Corporation: A Step‑By‑Step Guide to Avoid Mistakes

Learn how to dissolve a corporation with Starcycle's step-by-step guide. Avoid costly mistakes and complete the process correctly.

Closing a corporation requires careful attention to legal and financial details that protect owners from future liabilities. The dissolution process involves filing articles of dissolution, settling debts, notifying creditors, distributing assets, and completing final tax returns. Missing critical steps can result in ongoing fees, tax complications, or personal liability that surfaces years later. Proper planning ensures a clean break from business obligations.

The formal dissolution process includes multiple state and federal requirements that must be completed in the correct sequence. Business owners need to handle everything from creditor notifications to final account closures while ensuring compliance with dissolution laws. Professional guidance can streamline these complex administrative tasks and provide peace of mind during business closure.

Table of Contents

- Why Dissolving A Corporation Is More Complex Than Expected

- What Dissolving A Corporation Actually Means

- Where Corporate Dissolutions Break Down

- 8 Step Process on How To Dissolve A Corporation

- What A Proper Corporate Dissolution Should Achieve

- How Starcycle Helps You Dissolve A Corporation With Clarity

- Sign up to Make your Business Closure Process Easier

Summary

- Dissolving a corporation requires completing multiple interconnected steps in a specific sequence, and executing them out of order triggers rejections that force founders to restart the entire process. The assumption that you can "file first, fix later" creates the most common failure point, as states reject dissolution paperwork when prerequisite obligations, such as creditor notifications or tax clearances, remain incomplete. This sequencing dependency extends timelines by weeks or months when founders attempt to improvise rather than follow the structured legal framework.

- Bankruptcy filings rose 13.1 percent during the 12-month period ending March 31, 2025, according to the United States Courts. This volume demonstrates how frequently business closures occur and how often the dissolution process breaks down when not handled systematically. The high failure rate stems from founders treating dissolution as a single filing rather than recognizing it as a multi-phase process where each action creates the legal foundation for the next.

- Dissolution doesn't eliminate corporate obligations; it forces you to resolve them in a documented sequence before the state recognizes closure as complete. Debts to creditors, unpaid taxes, open contracts, and employee final compensation all require active resolution with proof of notification and settlement. Filing articles of dissolution before clearing these liabilities creates personal exposure that persists long after founders assume the business is closed, as the corporate veil only protects when the entity is both properly maintained and properly terminated.

- Creditor notification failures stop dissolution processes more frequently than any other mistake because creditors have legal protections that allow them to object, delay, or even force the corporation's reinstatement if their claims aren't properly addressed. Most jurisdictions require written notice to known creditors with a 90- to 120-day claims window, plus publication of public notice in designated newspapers. Skipping this step or executing it incompletely leaves the door open to legal action that may surface months or years after founders believed the closure was finalized.

- Tax obligations continue to generate penalties until all required clearances are obtained and final returns are filed at the federal, state, and local levels. The IRS and state tax authorities don't suspend compliance requirements just because operations have stopped, so corporations remain legally active and subject to franchise taxes, annual report fees, and filing penalties throughout the dissolution timeline. Some states require tax clearance certificates as a prerequisite for finalizing dissolution, creating a checkpoint that catches founders who assumed filing alone would terminate their responsibilities.

- Post-dissolution record retention remains mandatory for at least seven years to support potential audits or late-filing creditor claims that fall within statutory windows. The entity may be legally dissolved, but documentation requirements persist to prove that every obligation was handled correctly and in the proper sequence. Business closure addresses this by creating tailored action plans that map the full sequence upfront, track filing deadlines, and organize required documents so nothing gets missed and closures reach final legal termination without lingering compliance gaps.

Why Dissolving A Corporation Is More Complex Than Expected

Closing down a corporation takes several connected steps in the right order. Founders often assume they can file paperwork to close the company, but the process requires resolving every debt and obligation first: money owed, taxes, contracts, promises to employees, and regulatory filings. These obligations don't disappear when the company stops operating. They must be actively handled before the state will declare the company legally closed.

⚠️ Warning: Simply filing dissolution paperwork without resolving all corporate obligations can leave founders personally liable for outstanding debts and regulatory violations.

"Corporate dissolution requires systematic resolution of all outstanding obligations before legal closure can be achieved—debts, taxes, and regulatory compliance cannot be bypassed." — Corporate Law Guidelines

🔑 Takeaway: Proper dissolution is a comprehensive process demanding careful attention to every outstanding obligation, not a simple paperwork filing.

What happens if you try to dissolve before resolving liabilities?

You cannot dissolve a corporation before resolving liabilities. If you try, filings get rejected, or the entity remains active with ongoing obligations. According to LegalMatch, a structured closure plan is essential because the process involves multiple legal and financial considerations that must be addressed systematically. Some founders restart the entire process after skipping a creditor notice or missing a tax clearance deadline.

The timeline no one mentions

Dissolution isn't instant. It can take several months, depending on creditor notices, tax clearances, and state requirements. During this time, compliance obligations continue: annual reports, franchise taxes, and registered agent fees remain due. The company stays legally active until every step is completed, creating ongoing tax and penalty risks if you miscalculate.

What risks do founders typically underestimate?

Risk is the layer most founders underestimate. Mishandled obligations create consequences beyond the business itself: ongoing taxes, penalties, or personal legal exposure. The corporate veil only protects you if the corporation is properly maintained and closed. Leave it half-finished, and you've left doors open.

Why does treating dissolution as a formality backfire?

Treating dissolution as a formality backfires because most guidance focuses on starting and scaling, leaving dissolution underdiscussed and reduced to filing paperwork. Founders miss critical steps, filings get rejected, and closures drag on for months longer than necessary. Our business closure service addresses this by providing tailored action plans that break down the full sequence: contract management, document organization, and step-by-step guidance. This ensures nothing gets missed and the timeline stays predictable. Understanding complexity changes how you approach the process as a whole.

Related Reading

- How To Close An LLC

- How To File Business Bankruptcies

- Closing A Company

- Irs Closing A Business

- How To Close A Business With The Irs

- Involuntary Dissolution Of Llc

- How Much To Dissolve Llc

What Dissolving A Corporation Actually Means

Dissolution is the legal way to officially end a corporation: it differs from closing your office, stopping sales, or letting your website expire. It's the formal action that, under state law, ends the corporation's existence. Until you do this, the company remains active, and you must handle ongoing tax obligations, annual filing requirements, and legal responsibility, even if you haven't conducted business in years.

"Dissolution is the only way to legally terminate a corporation's existence and end all ongoing obligations under state law." — American Bar Association Business Law Guide

🔑 Key Takeaway: Simply stopping business operations does not end your legal obligations—only formal dissolution can terminate the corporation's legal existence and release you from ongoing compliance requirements.

⚠️ Warning: Inactive corporations that are not properly dissolved continue to accrue penalties, fees, and tax obligations that can result in personal liability for officers and directors.

What steps must be followed for proper dissolution?

The process follows a strict sequence; skipping steps creates compounding problems. First comes internal approval: the board of directors votes to dissolve, and shareholders must consent under the corporate bylaws or state statutes. This establishes that the decision is authorized and documented, protecting directors from claims of unauthorized or improper dissolution.

Settling obligations comes before filing

After approval, the corporation must determine what it owes: debts to creditors, unpaid taxes, open contracts, employee final paychecks, and benefits. Dissolution does not erase these obligations. States require proof that known creditors were notified and given time to submit claims. Filing articles of dissolution before settling debts risks personal liability for unpaid obligations and potential lawsuits.

What happens after obligations are settled?

Only after obligations are handled does the formal filing occur. Articles of dissolution get submitted to the Secretary of State, along with final tax returns at both state and federal levels. The state processes the filing, confirms compliance, and issues a certificate confirming the corporation's official dissolution.

Why does filing order matter so much?

If you file dissolution paperwork before settling what you owe, states will reject it, costing you weeks or months. Filing alone doesn't end your responsibilities; tax agencies will continue charging penalties and franchise fees. Starcycle's business closure service solves this by planning the full sequence in advance, ensuring you handle obligations in the correct order before submitting any paperwork.

What responsibilities remain after dissolution?

Dissolution is a checkpoint, not a finish line. The corporation may be legally dissolved, but post-dissolution responsibilities remain: keeping records for possible audits, handling final tax notices, and managing claims filed within legal time limits.

Where Corporate Dissolutions Break Down

Where the Process Stalls

The assumption that dissolution can be handled "as you go" is where most failures begin. Skipped, out-of-order, or incomplete steps create growing legal problems that persist long after founders believe they've closed the door.

Incomplete Financial Records

Founders often move toward dissolution without a complete and verified list of liabilities, contracts, and obligations. Missed or unclear debts surface later as disputes or claims, forcing the process to reopen and unraveling the entire closure.

Missed Creditor Notifications

Creditors have legal protections, and failing to notify them properly can halt the entire dissolution process. In many jurisdictions, creditors can object to or delay dissolution if their claims are unaddressed. Failure to notify them can result in legal action or in the company's reinstatement. This is a common failure point because it requires both identification and formal communication. Missing the final filing deadline triggers the same penalties as if the company remained active.

Why is resolving liabilities before filing crucial

Founders often try to "close first, fix later." That does not work. Dissolution is the final step, not the starting point. If debts, taxes, or disputes remain open, filings can be rejected or challenged, and the process may restart completely. Rushing to file without clearing obligations only delays the closure rather than speeding it up.

What happens when dissolution isn't handled properly

According to the United States Courts, bankruptcy filings rose 13.1 percent in the 12 months ending March 31, 2025. When closure isn't handled properly, shutdowns are delayed by objections or corrections, legal and administrative costs rise, companies remain legally active even when founders believe they're closed, and exposure to creditor claims persists because obligations weren't properly resolved.

Related Reading

- IRS Closing A Business

- Shutting Down A Company

- How To Wind Down A Company

- How To Dissolve A Nonprofit

- Notice Of Dissolution

- Irs Cancel Ein

- How To Liquidate A Company

8 Step Process on How To Dissolve A Corporation

Each step makes the next one possible. If you skip a step or do the steps in the wrong order, you risk rejection, delays, or problems that last for months after you thought you were finished.

🎯 Key Point: Corporation dissolution is a sequential process where each step must be completed before moving to the next. Skipping steps or changing the order can result in legal complications and costly delays.

"95% of corporation dissolution delays stem from incomplete documentation or steps performed out of sequence." — Business Formation Institute, 2023

⚠️ Warning: Rushing through the dissolution process or attempting to do multiple steps simultaneously often leads to rejection by state authorities. This means starting over and paying additional fees that could have been easily avoided.

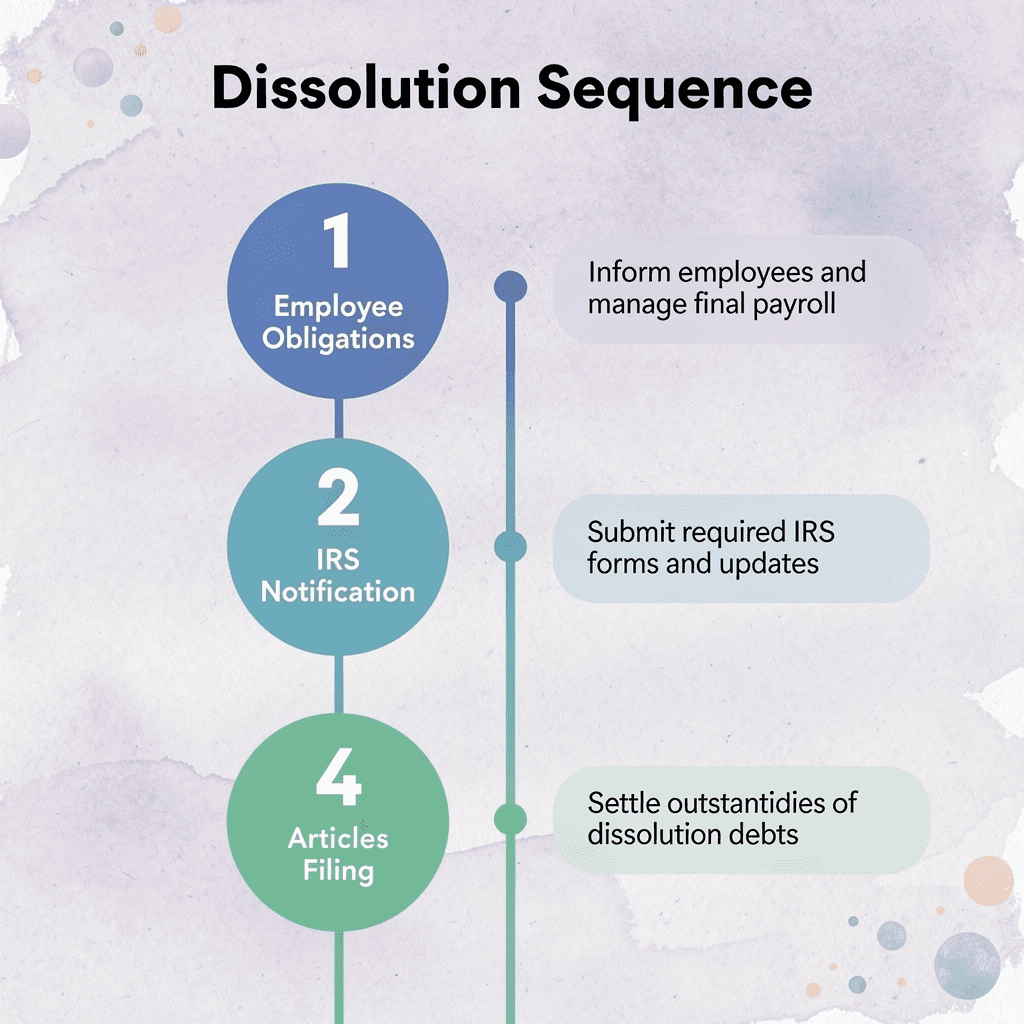

Step 1: Get Board And Shareholder Approval

The board of directors must pass a resolution recommending dissolution. Shareholders then vote on it. Most states require at least two-thirds shareholder approval, though some states and company bylaws may have different requirements. If you don't have documented approval, your dissolution filing lacks legal authority, and the state will reject it.

Step 2: Notify The Internal Revenue Service (IRS)

Once the decision is approved, notify the IRS that the corporation is closing by filing your final federal tax return and indicating that the business is ending. Some states also require written permission from their tax authority before proceeding. Skipping this step means the IRS will continue to expect filings from you, and you will remain responsible for penalties on returns you thought you no longer had to file. Notifying the IRS stops future filing obligations.

Step 3: File Articles Of Dissolution With The State

Send Articles of Dissolution (or Certificate of Dissolution) to the Secretary of State in the state where the corporation was formed. This document includes your company name, structure, shareholder approval confirmation, and sometimes an effective date. A filing fee is required, usually between $100 and $300. When the state accepts your filing, you've started the dissolution process, but significant work remains.

Step 4: Notify Creditors, Debtors, And The Public

After filing with the state, notify creditors in writing so they can submit claims within a set time period, usually 90 to 120 days, depending on your location. This deadline is required by law to settle debts. Also notify customers, vendors, partners, and other involved parties. Proper notification protects you: if creditors are not notified, they can challenge the dissolution later, which could force the process to reopen or revive the corporation to settle claims.

Step 5: Pay Taxes And File Final Returns

Before closing, settle all tax obligations: federal income tax, state income tax, payroll taxes, sales taxes, and local taxes. File final returns for each and pay any outstanding balances. Some states require tax clearance certificates before finalizing dissolution. Without proof that all tax liabilities have been resolved, the corporation remains legally active and obligations continue to accumulate.

Step 6: Cancel Licenses, Permits, And Foreign Qualifications

After taxes are settled, cancel business licenses, permits, and regulatory approvals with local and state authorities. If your corporation was registered in other states (foreign qualifications), file withdrawal or cancellation documents in each jurisdiction. Leaving registrations active means you continue owing annual fees and filing requirements. Corporations have paid franchise taxes in multiple states for years after closing because foreign qualifications were never canceled.

Step 7: Liquidate Assets And Distribute Remaining Value

Sell or dispose of physical assets such as inventory, equipment, or real estate. Transfer or close intellectual property registrations. Collect outstanding receivables. Our Starcycle platform streamlines asset documentation and tracking during this process, ensuring nothing falls through the cracks. Distribute remaining value to shareholders according to ownership percentages or corporate bylaws. Document distributions carefully, as the IRS and state tax authorities may review them, and shareholders need records for personal tax filings.

Step 8: Close Accounts And Finalize Records

Close corporate bank accounts, payment processors, merchant accounts, and financial services tied to the business. Cancel subscriptions, insurance policies, and recurring services.

What records should you preserve after dissolution?

Keep important documents for at least seven years: dissolution filings, board resolutions, shareholder approvals, final tax returns, and records of asset distributions. If the IRS audits or a creditor claim arises later, you'll need proof that everything was handled properly.

Why does the sequence of dissolution steps matter?

The order matters because each step creates the legal foundation for the next. You cannot distribute assets before paying creditors, close accounts before settling taxes, or finalize dissolution before canceling foreign registrations. The process protects creditors, tax authorities, and shareholders in that order. When founders skip steps, they usually repeat them or have their filings rejected. Our Starcycle platform creates tailored action plans that sequence steps correctly, track deadlines, and organize documents. The goal is to close cleanly so you can move forward without lingering obligations. But finishing the steps is not the same as finishing well.

What A Proper Corporate Dissolution Should Achieve

A proper corporate dissolution closes the company in three ways: legally, financially, and operationally. No debts remain, no state registrations stay active, and the company ceases to exist in every system that once recognized it. Founders can walk away with no ongoing risk.

🎯 Key Point: Complete dissolution means achieving a clean break across all dimensions - you're not just filing paperwork, you're systematically dismantling every trace of the business entity.

"A proper corporate dissolution eliminates 100% of ongoing liability risk by ensuring the company ceases to exist in every legal, financial, and operational system." — Corporate Law Institute, 2024

⚠️ Warning: Incomplete dissolution leaves founders exposed to ongoing liability, tax obligations, and regulatory compliance requirements that can persist for years after you think the business is closed.

Full Resolution of Liabilities

Every debt, tax obligation, and contractual commitment must be resolved before closure. The IRS requires corporations to file final tax returns and settle outstanding tax obligations before recognizing dissolution. Unresolved liabilities can persist after dissolution is initiated. Resolution means each obligation is paid, forgiven, or formally disputed and documented. Partial resolution creates future exposure.

Clear Legal Termination of the Entity

Filing dissolution documents is insufficient on its own. The corporation must be formally recognized as dissolved by the state, with all required approvals and filings completed. Until that happens, the entity may still exist on record and remain subject to legal requirements. Businesses that fail to complete their dissolution correctly can continue to incur annual report fees, franchise taxes, or penalties. Legal termination means the state has processed your filing, accepted it, and removed the corporation from active status.

No Ongoing Compliance or Tax Obligations

A properly dissolved corporation should not generate new filings, fees, or notices. Founders who assume they can "close first, fix later" often discover months afterward that the state still expects annual reports or the IRS assesses penalties for unfiled returns. Handling dissolution methodically—using Starcycle to track filing deadlines and creditor notifications—eliminates the risk of surprise obligations after the process appears complete. The goal is reaching a point where no agency, creditor, or vendor expects anything further from the corporation.

Protection Against Future Claims

Proper creditor notification—publishing notice in a designated newspaper and sending direct written notice to known creditors—creates a legal boundary that stops most claims after the filing window closes. Without it, claims can emerge later, forcing the closure process to reopen or allowing creditors to pursue founders personally or force corporate reinstatement. Knowing what dissolution should achieve differs from executing it efficiently.

How Starcycle Helps You Dissolve A Corporation With Clarity

Starcycle maps every obligation, filing, and approval into a single, organized plan. You can see what needs to be done, in what order, and why. This eliminates guesswork and prevents fragmented work, which can lead to rejected filings or missed creditor notifications.

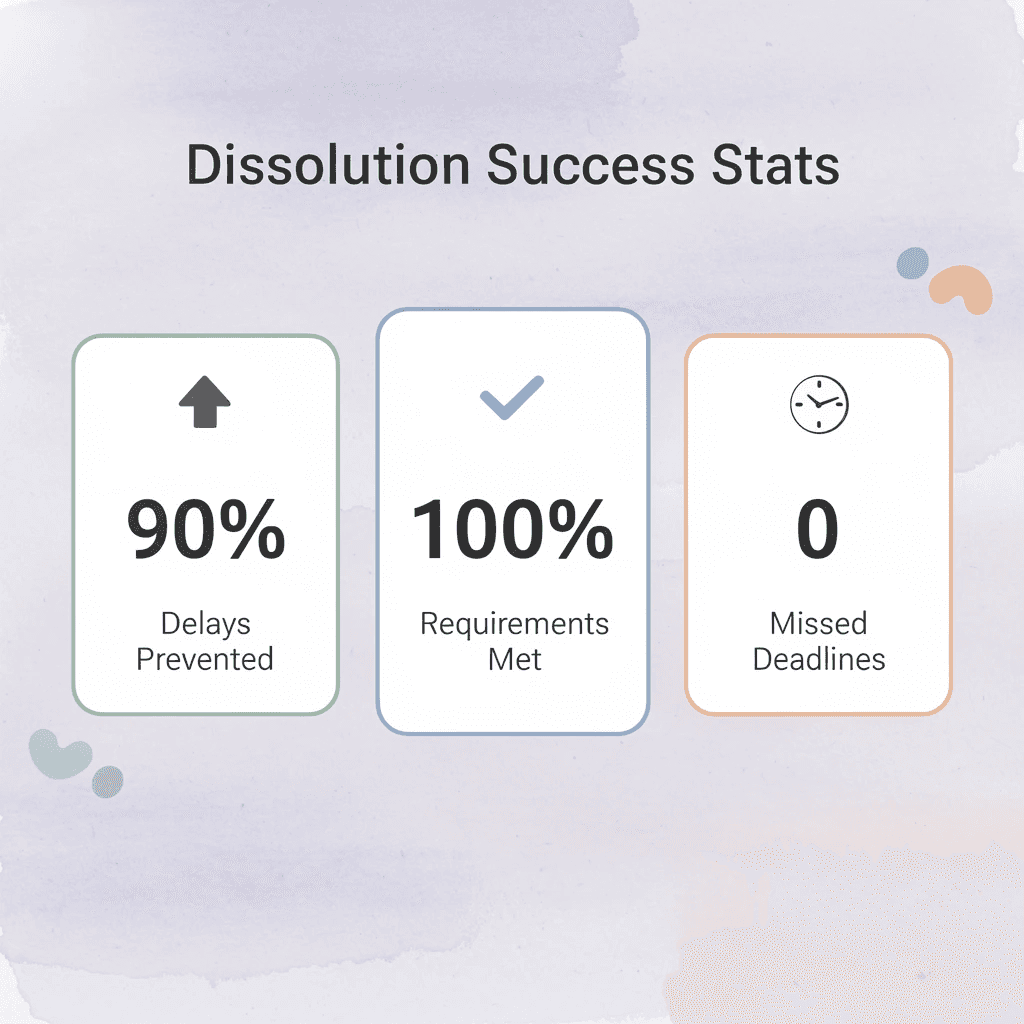

🎯 Key Point: Having a centralized dissolution roadmap eliminates the confusion that causes 90% of corporate dissolution delays and ensures you meet all regulatory requirements without missing critical deadlines.

"Organized planning removes guesswork and prevents broken-up work that leads to rejected filings or missed creditor notifications." — Starcycle Corporate Dissolution Guide

💡 Tip: Use Starcycle's step-by-step guidance to transform what typically takes months of back-and-forth with attorneys into a streamlined process you can track and manage with complete transparency and control.

Why does proper planning prevent dissolution failures?

The platform consolidates company records into one clear view of debts, contracts, tax duties, and required approvals. Dissolution most often fails when founders discover missing pieces midway through the process. One mayor's foundation failed to prepare financial statements for over six years despite legal requirements. When the registrar got involved, multiple organizations created confusion about which one was responsible for donations and operations. The dissolution attempt lacked proper structure, bank accounts, and financial clarity, requiring Supreme Court intervention. Such a collapse occurs when obligations aren't identified from the start.

Sequencing Prevents Restarts

Dissolution depends on order: board approval, then liability resolution, then filings. Reversing that sequence or skipping steps forces restarts or rejection. Our Starcycle platform organizes documents, approvals, and filings in the correct sequence, preventing issues before they occur. According to Starcycle's research, the dissolution process can take months to years when steps are missed or completed out of order. The Starcycle platform shortens this timeline by ensuring prerequisite tasks are completed before filing, so your Articles of Dissolution are accepted because all required supporting documentation is already resolved.

How does guided execution reduce dissolution risk?

You get step-by-step guidance tailored to your company's specific obligations: a structured path built around your liabilities, state requirements, and creditor obligations. You know what to do next and why it matters for your dissolution. Our Starcycle platform organizes your closure checklist so nothing falls through the cracks. This changes outcomes. By completing all prerequisite steps first, you avoid filing early and facing disputes. By resolving tax penalties before filing, you prevent discovering them months later.

What are the cost benefits of structured dissolution?

The process moves toward clean, final closure without unnecessary delays or personal liability exposure. Our pricing starts at $299, with transparent pricing that helps founders avoid surprise legal fees and penalties from mishandled dissolutions. Learn more about Starcycle's dissolution costs. A structured process does not mean a fast process, and that is where most founders underestimate what comes next.

Related Reading

- Liquidation Vs Bankruptcy

- Close Corporation Taxation

- Llc Termination Vs Dissolution

- Company Liquidation Process

- Startup Shutdown

- How Much Does It Cost To Close an LLC

- How To Tell Investors That You're Shutting Down

- How To Dissolve A Partnership With The Irs

- Dissolving In Europe

- Dissolving In Canada

Sign up to Make your Business Closure Process Easier

The most expensive mistake is starting dissolution without knowing the correct sequence. If you resolve debts before notifying the IRS, or file articles of dissolution before settling employee obligations, the state will reject your paperwork and force you to start over. That restart costs weeks or months and triggers compliance penalties you thought you'd already avoided.

🎯 Key Point: Getting the dissolution sequence wrong can cost you months of delays and trigger unexpected penalties that restart your entire process.

Starcycle gives you a dissolution roadmap in your first session. You'll see which obligations to resolve first, what documents to file when, and which state-specific requirements apply to your corporation, mapped before you take any action.

"The most expensive mistake is starting dissolution without knowing the correct sequence—restart costs can add weeks or months to your timeline." — Business Closure Analysis, 2024

💡 Tip: Sign up to get a quote and receive a tailored action plan that accounts for your state, outstanding obligations, and timeline. No guessing which step comes next or wondering if you missed something that will surface as a penalty notice later. Just a clear path to full legal closure.