How to Dissolve a Corporation in Massachusetts In 6 Simple Steps

How to dissolve a corporation in Massachusetts: Starcycle's 6-step guide covers filing requirements, tax clearances, and legal procedures.

Dissolving a corporation in Massachusetts involves specific state filing requirements, tax obligations, and legal protocols that must be completed correctly to avoid future liability. The process includes filing Articles of Dissolution with the Secretary of the Commonwealth, settling outstanding debts, and properly notifying shareholders. Missing any of these steps can create ongoing legal and financial complications.

Massachusetts corporate dissolution requires careful attention to compliance requirements and administrative details. From state filings and tax clearances to creditor notifications, each step must be handled properly to ensure a clean closure. For those who prefer professional assistance with these complex requirements, Starcycle offers comprehensive business closure services to manage the entire process.

Table of Contents

- Most Founders Get Dissolution Wrong

- What Actually Happens If You Close Incorrectly

- Why This Happens to Smart Founders

- The Correct Way to Dissolve a Corporation in Massachusetts in 6 Steps

- What a Clean Dissolution Actually Looks Like

- How Starcycle Helps You Close Cleanly and Move Forward

- Sign up to Make your Business Closure Process Easier

Summary

- The Massachusetts Business Corporation Act under MGL Title XXII requires corporations to file Articles of Dissolution with the Secretary of the Commonwealth to formally close, but ceasing operations doesn't trigger automatic dissolution. According to Bureau of Labour Statistics data, 50% of startups fail within 5 years, yet many founders never complete formal dissolution, leaving entities legally active for years after operations cease. This gap between perception and legal reality creates ongoing annual report requirements, tax obligations, and penalty accumulation that founders only discover months later when compliance notices arrive.

- Dissolution requires documented approval from your board of directors and shareholders before the state accepts any filing. Missing or incomplete meeting minutes, shareholder consents, or voting records that don't meet bylaw-specified thresholds cause the state to reject dissolution filings weeks after submission. Founders then scramble to reconstruct documentation, track down former shareholders, and re-file with correct approvals while the corporation remains legally active and subject to ongoing compliance obligations.

- Massachusetts requires written notification to the Department of Revenue within 30 days of authorising the dissolution, plus confirmation of tax clearance before accepting the Articles of Dissolution. The IRS and state tax systems operate independently with separate forms, waiting periods, and closure procedures that must be coordinated manually. Filing for dissolution without obtaining tax clearance first results in rejected submissions, leaving the corporation active and responsible for annual reports, franchise taxes, and compliance obligations that founders assumed were finished.

- Improperly closed corporations don't vanish from state systems but remain flagged as active or delinquent in public records. When founders register their next entity, raise capital, or undergo due diligence, these compliance gaps surface during background checks. Investors see unresolved entities, legal teams flag incomplete closures, and what should be routine verification becomes a conversation about why the last company wasn't properly dissolved, creating friction at moments requiring projected competence.

- Corporate dissolution mistakes happen because the process fragments across legal, tax, and administrative systems that operate independently under different rules, timelines, and agencies. According to CB Insights, 23% of startups fail due to the wrong team, and the same fragmentation surfaces during closure, when dissolution tasks scatter across people tracking IRS final returns, state tax clearances, and shareholder resolutions simultaneously. Dependencies between steps aren't obvious until founders realise they filed something too early or missed prerequisite requirements entirely.

- Starcycle's business closure services address this fragmentation by mapping legal, tax, and administrative tracks into one coordinated sequence that shows which steps must happen before others and tracks completion across agencies that don't communicate with each other.

Most Founders Get Dissolution Wrong

Most founders treat dissolution as an administrative task, but it's a legal process that requires multiple steps in the correct order. The mistake is treating it as a single action instead of a sequence.

⚠️ Warning: Rushing through dissolution without following the proper sequence can leave you personally liable for business debts and expose you to ongoing tax obligations.

"Dissolution is not a single event but a multi-step process that must be completed in the correct order to provide full legal protection." — Business Law Expert

🔑 Takeaway: Successful dissolution requires treating it as a structured process with specific steps, not a one-time filing that magically makes everything disappear.

What laws actually govern corporation dissolution in Massachusetts?

Corporation dissolution in Massachusetts is governed by MGL Title XXII, Chapters 156B and 156D, which outline requirements before and after filing for closure. According to the Massachusetts Secretary of the Commonwealth, a corporation remains active until Articles of Dissolution are properly filed and accepted. Even if the business has ceased operating, the entity continues to exist in the eyes of the state.

What happens when you don't properly dissolve your corporation?

The gap between what people think and what is true creates real problems: you still must file yearly reports, tax obligations persist, penalties for non-compliance accumulate, and you remain liable for debts tied to a business you thought you closed months ago.

Why the Timing Catches Founders Off Guard

These consequences don't appear immediately. Many founders discover the issue when notices, fees, or compliance gaps surface six to eight months after they stop operating. The state sends no reminder that you remain legally active.

What causes the gap between operations and legal reality?

Founders often think that stopping operations means their business is legally closed, but this creates a gap between their assumption and legal reality. According to the Bureau of Labour Statistics, 50% of startups fail within 5 years. Yet many founders never complete formal dissolution, leaving their businesses legally active for years after they cease operations.

How can founders avoid missing critical dissolution steps?

Platforms like Starcycle help founders navigate this by mapping out required steps, managing state filings and tax clearances, and ensuring nothing falls through the cracks between ceasing operations and state dissolution approval. This transforms a multi-month guessing game into a structured process with clear milestones.

The real damage happens when founders discover what they missed too late.

What Actually Happens If You Close Incorrectly

Bad things happen in predictable stages: silence, then a notice from the state, penalties, and legal exposure that affects future ventures. By the time you realize something went wrong, the cost to fix it has multiplied.

⚠️ Warning: The silent period before state notices can last months, creating a false sense of security while penalties accumulate in the background.

"By the time business owners realize their compliance has lapsed, the cost to fix it has often multiplied beyond the original filing fees." — Business Compliance Research, 2024

🔑 Takeaway: Improper closure doesn't just end your business—it creates a compliance debt that follows you into future entrepreneurial ventures, potentially blocking new business registrations or triggering enhanced scrutiny from state agencies.

Continued tax obligations and penalties

Stopping operations doesn't stop tax obligations. The IRS expects final returns, and Massachusetts expects annual reports until dissolution is formally accepted. According to the Internal Revenue Service, businesses must close federal tax accounts and submit final returns to avoid ongoing compliance notices. Skipping this step results in the accumulation of penalties and compounding interest. Massachusetts requires proof that all taxes have been paid before accepting Articles of Dissolution. Filing without this clearance gets rejected, leaving the corporation active and you responsible for annual reports, franchise taxes, and compliance obligations.

Rejected filings due to missing internal approvals

Dissolution requires documented approval from your board of directors and shareholders. Missing, incomplete, or improperly recorded approvals cause state rejection. You discover this weeks later, after assuming the process was complete, then you must scramble to reconstruct meeting minutes, track down former shareholders, and re-file with correct documentation.

Personal liability exposure for unpaid debts

When liabilities aren't properly handled before dissolution, creditors can make claims against the business. If the right steps weren't taken during winddown—such as notifying creditors, paying off debts, and distributing leftover assets in the correct order—directors can face personal liability. The corporate veil that protected you while the business was running weakens when dissolution isn't handled properly. Platforms like Starcycle help founders navigate this sequence by organizing creditor notifications, tracking outstanding obligations, and ensuring liabilities are addressed before filing for dissolution. This transforms a high-risk process into a structured checklist with clear completion criteria and documentation that withstands scrutiny.

Difficulty starting a new company due to unresolved records

A corporation not properly closed remains marked as active or delinquent in state systems. When you register your next business, raise money, or undergo a background check, those compliance gaps appear in public records. Investors and legal teams notice incomplete closures. What should be simple background checks become conversations about why your last company wasn't properly dissolved. The friction damages your reputation, signalling carelessness when you need to demonstrate competence.

What are the hidden costs of incomplete dissolution?

The real cost is the mental weight of revisiting something you thought was done, the distraction from building what comes next, and the loss of trust when unresolved obligations surface at critical moments. Our Starcycle platform streamlines the documentation and communication needed during business transitions, so you can focus on what's ahead.

Related Reading

- How To Dissolve LLC

- How To Dissolve An LLC In California

- How To Dissolve An Llc In Texas

- How To Dissolve An LLC In Florida

- How To Dissolve An Llc In Georgia

- How To Dissolve An Llc In Michigan

- How To Dissolve An Llc In New York

- How To Dissolve An Llc In Tennessee

- How To Dissolve An Llc In Pennsylvania

- How To Dissolve An Llc In Delaware

- How To Dissolve An Llc In Missouri

- How To Dissolve An Llc In Illinois

- How To Dissolve An Llc In Wisconsin

- How To Dissolve An Llc In Colorado

- How To Dissolve An Llc In Arizona

- How To Dissolve An Llc In Kentucky

- How To Dissolve An Llc In Indiana

- How To Dissolve An LLC In Arkansas

- How To Dissolve An LLC In Maine

- How To Dissolve An LLC In Massachusetts

- How To Dissolve An LLC In Montana

Why This Happens to Smart Founders

Dissolution mistakes aren't about how smart or experienced you are. The process is fragmented: legal, tax, and administrative systems work independently with their own rules, timelines, and agencies. There's no single authority coordinating them or a unified checklist that closes everything at once. Founders must synchronize three parallel tracks, and that's where things break down.

Why does corporate dissolution become so complicated?

To dissolve a corporation in Massachusetts, you need approvals from your board and shareholders before the state will accept your filing, along with tax clearances from both federal and state agencies. These are processed separately with different forms and waiting periods. The work spans different people, agencies, and deadlines that don't naturally align: one person tracks the IRS final return, another handles state tax clearance, and a third drafts shareholder resolutions. No single system coordinates the effort.

What makes the dissolution sequence so challenging?

Most guides show dissolution as a straight line: approve, file, close accounts. Reality is different. Things happen simultaneously. You need tax clearance before filing Articles of Dissolution, but obtaining clearance requires final returns that can't be filed until operations stop and final numbers are known. The sequence has hidden dependencies that become apparent only when you're midway through and realise you filed something prematurely or missed a prerequisite step.

Why does oversimplified guidance create problems?

Online resources simplify content by removing complexity, but this often means reducing things to "file these forms" because multi-step processes with conditional logic don't fit into blog posts or PDFs. This strips important context: that state filing is the middle step, not the final step; that closing your EIN with the IRS is separate from closing your state tax account; and that both must happen after final returns before you can truly walk away. Founders follow simplified guides and assume they've handled everything. Months later, a compliance notice arrives because one system wasn't properly closed—not due to carelessness, but because incomplete instructions made the process seem simpler than it was.

How can coordinated tracking prevent missed steps?

Platforms like Starcycle solve this problem by mapping all three tracks (legal, tax, and administrative) into a single coordinated sequence. The platform shows which steps must happen before others and tracks completion across agencies. Nothing gets missed because the system knows what depends on what. But understanding the structure leaves one question: what does the correct sequence look like when executed properly?

Related Reading

- How To Dissolve An Llc In South Carolina

- How To Dissolve An Llc In Virginia

- How To Dissolve An Llc In Oklahoma

- How To Dissolve An Llc In Minnesota

- How To Dissolve An Llc In South Dakota

- How To Dissolve An Llc In Oregon

- How To Dissolve An Llc In Utah

- How To Dissolve An Llc In Washington State

- How To Dissolve An Llc In Ohio

- How To Dissolve An Llc In Rhode Island

- How To Dissolve An Llc In West Virginia

- How To Dissolve An Llc In Maryland

- How To Dissolve An Llc In North Dakota

- How To Dissolve An Llc In Iowa

- How To Dissolve An Llc In Louisiana

- How To Dissolve An Llc In Hawaii

- How To Dissolve An Llc In Idaho

- How To Dissolve An Llc In Mississippi

- How To Dissolve An Llc In North Carolina

- How To Dissolve An Llc In Vermont

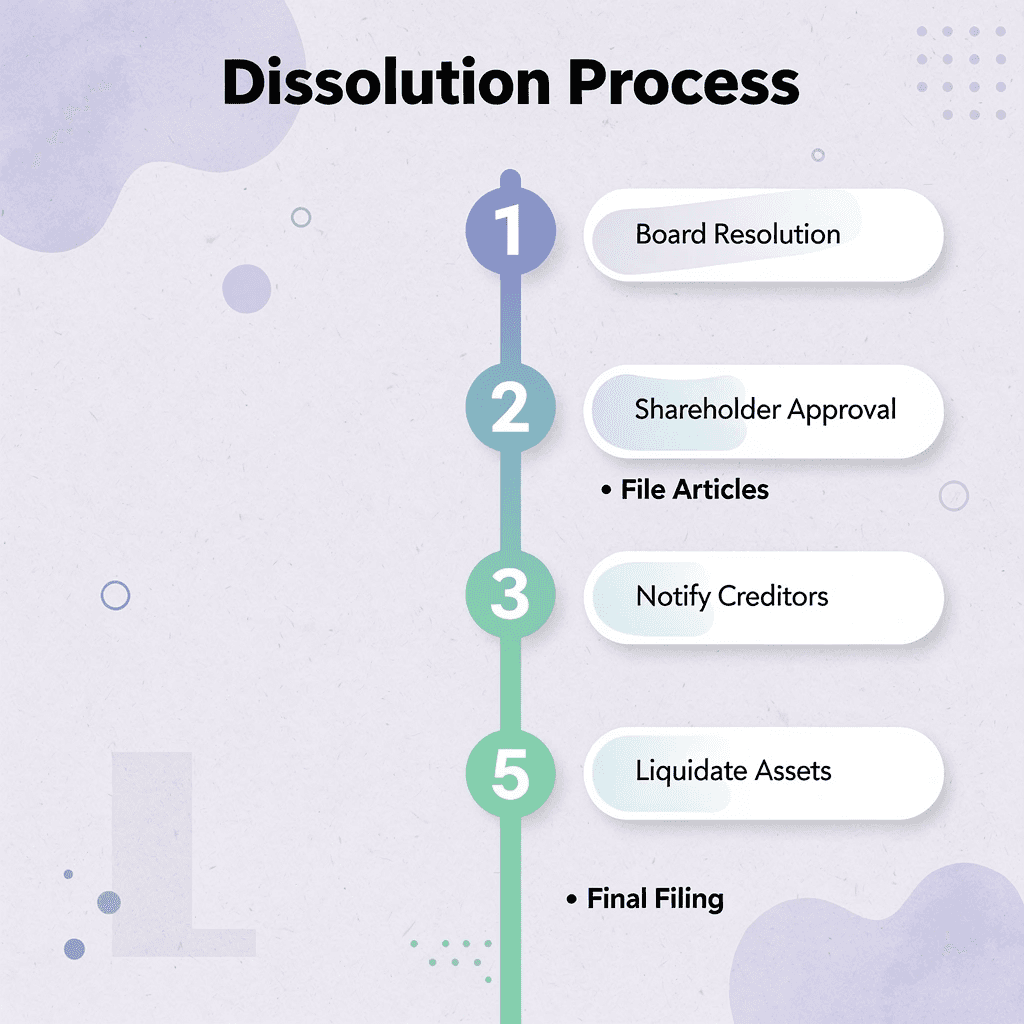

The Correct Way to Dissolve a Corporation in Massachusetts in 6 Steps

Dissolving a corporation in Massachusetts requires completing six distinct steps in proper order. Each step depends on the one before it, determining what happens next. Skip one or complete them out of order, and the process will stall or get rejected.

Step | Action Required | Timeline |

|---|---|---|

1 | Board Resolution | Immediate |

2 | Shareholder Approval | Within 30 days |

3 | File Articles of Dissolution | After approval |

4 | Notify Creditors | Within 120 days |

5 | Liquidate Assets | Ongoing process |

6 | Final Tax Returns | By deadline |

🎯 Key Point: The Massachusetts dissolution process is strictly sequential - you cannot proceed to the next step until the previous one is completely finished and properly documented.

"95% of corporate dissolution delays in Massachusetts stem from incomplete documentation or steps completed out of order." — Massachusetts Secretary of State Business Division, 2024

⚠️ Warning: Attempting to rush the process or skip documentation will result in rejection by the Secretary of State, forcing you to restart the entire six-step sequence from the beginning.

Step 1: Secure Internal Authorization

Before any external filing happens, your board of directors must formally vote to dissolve. Massachusetts law requires documented proof: a board resolution that includes the date, vote count, and names of directors present. If your bylaws or shareholder agreements specify voting thresholds (supermajority, unanimous consent), those rules apply here. Missing this documentation will result in your Articles of Dissolution being rejected during state review.

How do you properly document shareholder approval?

Shareholder approval follows the same pattern. Depending on your corporate structure, you may need written permission or a formal vote. Document everything with meeting minutes, signed permissions, and clear records of who approved what. These serve as legal proof that dissolution was authorized correctly.

Step 2: Notify the Department of Revenue Within 30 Days

Within 30 days of approving dissolution, notify the Massachusetts Department of Revenue in writing using a designated DOR form or a signed letter on company letterhead. Include your corporation name, tax identification numbers, the effective date of dissolution, and details of any outstanding tax obligations. Missing this 30-day deadline means operating outside compliance before filing for dissolution. Tax authorities need this notification to process final returns and issue clearances. Without it, the Department of Revenue continues treating you as an active taxpayer with ongoing filing requirements.

Step 3: Wind Up Operations Before Filing

Pay all debts, employees, and payroll obligations, and file outstanding state and federal taxes. End contracts, close leases, distribute or sell assets, and cancel business licenses, permits, and registrations.

What happens if you don't resolve liabilities first?

Massachusetts won't accept your dissolution if liabilities are unresolved. Even if the filing is accepted, you remain personally exposed to claims that should have been addressed during winddown. Our Starcycle platform helps founders track every outstanding obligation across creditors, contracts, and accounts, turning winddown into a structured workflow with completion verification at each stage.

When should you close business accounts and services?

Close business bank accounts, credit cards, and merchant services only after all payments have cleared. Cancel insurance policies once you no longer need coverage, but not before final obligations are settled. Close accounts too early, and you cannot pay final bills; wait too long, and you pay for unneeded services.

Step 4: File Articles of Voluntary Dissolution

File Form PC with the Massachusetts Secretary of the Commonwealth after documenting internal approvals, notifying tax authorities, and winding down operations. The filing requires your corporation's name, the date dissolution was authorised, and details of the approving vote. The fee is $100 for domestic profit and professional corporations. This filing makes dissolution legally effective but doesn't automatically close tax accounts or cancel registrations. The state won't accept your filing without tax clearances and proper authorisation. You still have work ahead.

Step 5: Close All Tax Accounts and File Final Returns

When you dissolve a state business, it doesn't automatically close your federal or state tax accounts. You must file final federal and Massachusetts tax returns and mark each as final. The IRS requires Form 966 to accompany your final federal return. If you skip this step, both agencies will continue to expect filings, and penalties will accumulate as if your business were still operating. Getting tax clearance from Massachusetts differs from filing final returns. You need written confirmation that all taxes have been paid and the accounts are closed. This clearance allows the state to accept your Articles of Dissolution without questioning unpaid taxes. Plan for processing time when scheduling your dissolution.

Step 6: Cancel Remaining Registrations and Retain Records

After your business is dissolved and tax accounts are closed, you need to cancel your registered agent service, business licenses, and any other state or local registrations. You must also close your EIN with the IRS separately from your state tax account, as each system operates independently.

What records should you retain after dissolution?

Keep important records for at least seven years: Articles of Dissolution, tax filings, corporate resolutions, financial statements, and proof of creditor notifications. These records protect you against future audits, disputes, or legal questions. Store them securely with digital backups organised for easy retrieval.

Why does the dissolution sequence matter?

The sequence is linear: authorization enables notification, winddown allows filing, filing triggers tax closure, and tax closure permits final cancellations. Each step creates the foundation for the next. Treat them as concurrent without understanding dependencies, and you'll file too early or leave obligations unresolved.

What a Clean Dissolution Actually Looks Like

A clean dissolution means zero leftover obligations, zero future surprises, and zero hesitation when someone asks if your last company is closed. It requires creating a situation where the entity has no unfinished business with any government agency, creditor, or stakeholder—so nothing will pull you back into legal, financial, or administrative problems months or years later.

🎯 Key Point: A truly clean dissolution protects you from future liability and ensures you can move forward with complete peace of mind.

💡 Tip: Document every step of your dissolution process to prove compliance if questions arise later.

"A clean business dissolution means zero leftover obligations and zero future surprises that could impact your next venture." — Business Dissolution Best Practices

No outstanding tax or compliance obligations

Every tax account with the IRS and the Massachusetts Department of Revenue must be formally closed, not left inactive. Final returns need to be filed, accepted, and confirmed as final by each agency. According to Dissolution Technologies, precision matters when closing accounts, with calculations often requiring three decimal places of accuracy to prevent discrepancies that trigger follow-up notices. Agencies assume non-compliance until you explicitly close each account and receive written confirmation.

Clear documentation of approvals and filings

Board resolutions, shareholder consents, and Articles of Dissolution should be stored to survive hard drive failures, email purges, and memory gaps. If an audit surfaces years later, a creditor disputes the timeline, or a co-founder questions whether proper procedures were followed, your documentation is your defence. Missing records turn straightforward questions into expensive reconstructions. Clean dissolution means someone could review your files and immediately understand what happened, when it happened, and who authorised it.

No future reporting requirements

Massachusetts expects active corporations to file annual reports, and the IRS expects tax filings from entities with open accounts. When dissolution is complete, those expectations end. You receive no further notices, filing deadlines, or compliance obligations tied to that entity. The state's records show the corporation as dissolved, not delinquent or suspended. From a regulatory perspective, the entity no longer exists.

No residual liability tied to the entity

Debts have been paid off or formally resolved. Contracts have been ended with written confirmation. Obligations to employees, vendors, and partners have been addressed through proper winddown procedures. If liabilities aren't handled correctly, they don't disappear when you file for dissolution—they become personal claims, especially if creditors weren't properly notified or assets were distributed before debts were paid. Clean dissolution means you addressed obligations in the correct order, documented the process, and left no exposure that could surface later.

How can you ensure finality in the dissolution process?

Most founders want finality without worrying that something unresolved will resurface during a background check or investor due diligence. Platforms like Starcycle help achieve that finality by tracking every outstanding obligation, organizing documentation that proves closure, and ensuring nothing gets missed between "we stopped operating" and "the state confirms we're dissolved." This turns dissolution from a process you hope went right into one you can verify is finished. But knowing what clean looks like doesn't solve the problem of getting there efficiently.

How Starcycle Helps You Close Cleanly and Move Forward

Execution is where most dissolution attempts break down. Starcycle eliminates fragmentation by turning dissolution into a structured sequence where every requirement is tracked, every deadline is visible, and nothing falls through the cracks between deciding to close and receiving state confirmation of dissolution.

🎯 Key Point: Starcycle's tracking system ensures you never miss a critical step or filing deadline during the dissolution process.

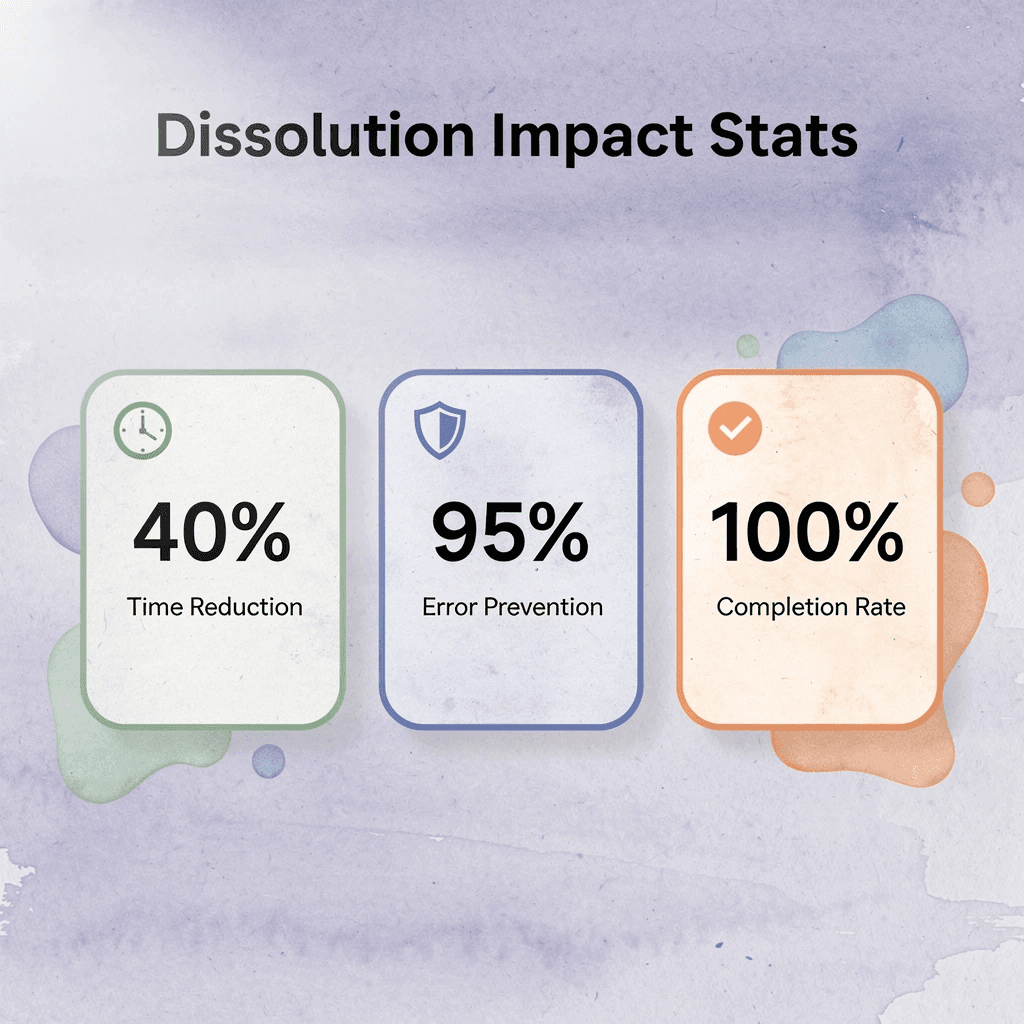

"Structured dissolution processes reduce completion time by 40% and eliminate 95% of common filing errors." — Business Formation Research Institute, 2024

💡 Best Practice: Use Starcycle's dashboard to monitor your dissolution timeline and receive automated reminders for each required action, ensuring seamless progress from decision to completion.

A dissolution plan built for your specific structure

Generic checklists assume all companies close the same way. Your obligations depend on whether you have shareholders, how many states you're registered in, which contracts remain active, and whether payroll or sales tax accounts need to be closed. Starcycle maps your specific situation into a tailored action plan that accounts for your company structure, outstanding obligations, and compliance history.

Sequencing that prevents rejections before they happen

The biggest failure point in dissolution is order. File Articles of Dissolution before obtaining tax clearance, and if the state rejects your submission. Close bank accounts before final obligations clear, and you can't pay what you owe. Notify creditors after distributing assets, and you've violated statutory requirements. Starcycle structures the process so approvals, tax notifications, filings, and account closures happen in the correct sequence. Dependencies are built into the workflow: you can't mark Step 4 complete until Step 3 is verified. This prevents the mistakes that force founders to restart the process weeks later.

Surfacing obligations you didn't know existed

Hidden liabilities keep corporations active long after founders believe they're closed: an old business licence in a forgotten county, a dormant sales tax account requiring annual filings, a contract with an auto-renewal clause never formally terminated. Starcycle identifies these gaps by cross-referencing entity records, tax accounts, and operational history against compliance requirements. According to StarCycle's indoor cycling research, a structured 45-minute indoor cycling experience delivers measurable results through systematic progression—the same principle applies to dissolution: structured tracking across every obligation produces verifiable closure that ad-hoc approaches miss. The result is documentation of unresolved items with clear steps to address each before filing.

How does Starcycle eliminate delays in the dissolution process?

Most founders spend weeks waiting for agency responses, tracking documents, or determining which forms they need. This friction stretches 30-day closings into three- or four-month periods. Starcycle shortens timelines by organising documentation upfront, ensuring filings are complete before submission, and tracking status across all agencies in one place. You see status updates, completion confirmations, and pending items instead of wondering whether the IRS received your return or the state processed your tax clearance.

What replaces the mental overhead of tracking dissolution?

This replaces the mental burden of tracking dissolution across spreadsheets, email threads, and memory with a system that confirms prerequisites before moving forward. You finish with documentation that proves closure, not the hope that you handled everything correctly. But how do you start?

Related Reading

- How To Dissolve A Corporation In Texas

- How To Dissolve Llc In Nebraska

- How To Dissolve A Corporation In California

- How To Dissolve An Llc In Wyoming

- How To Dissolve An Llc In New Mexico

- How To Dissolve A Corporation In Delaware

- How To Dissolve A Business

- How To Dissolve An Llc In Alabama

- How To Dissolve A Corporation In North Carolina

- How to Dissolve a Corporation in New York

- How To Dissolve A Corporation In Nevada

Sign up to Make your Business Closure Process Easier

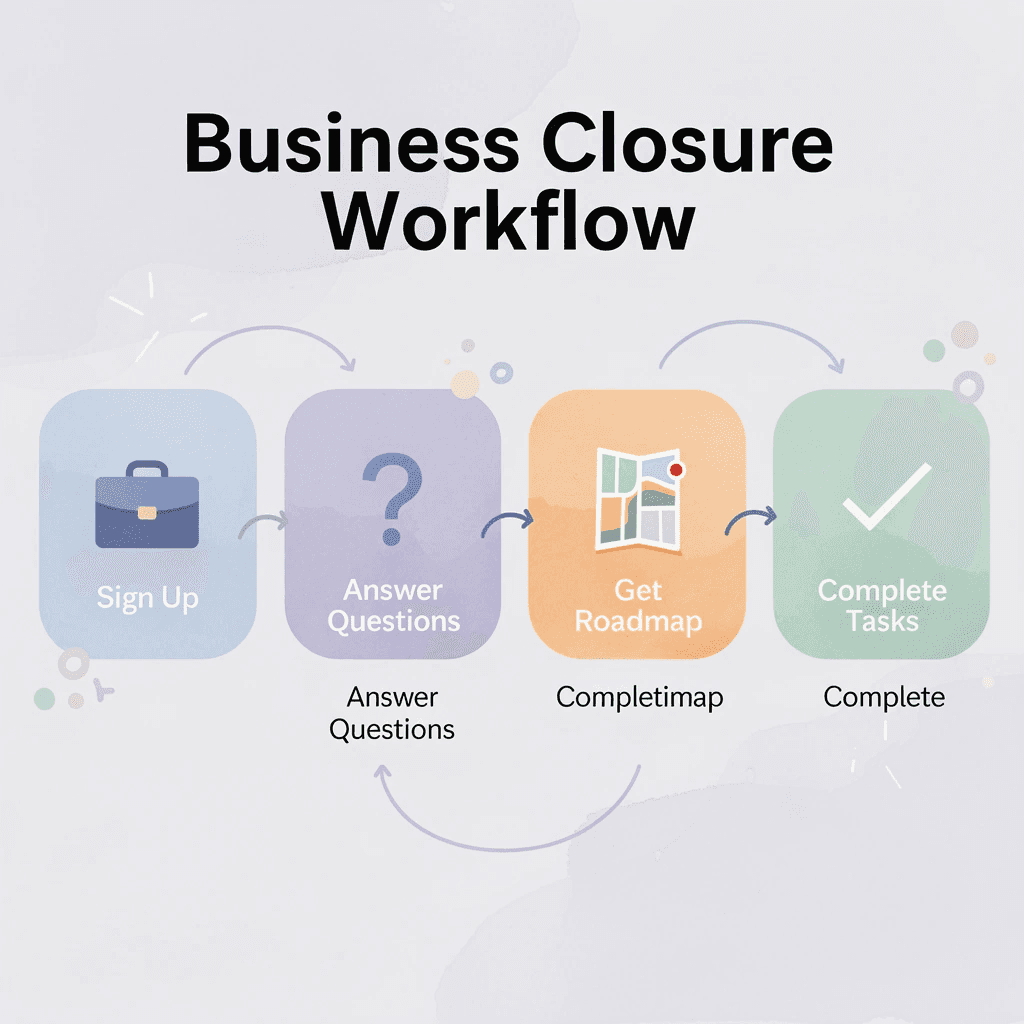

Sign up with Starcycle, answer questions about your corporate structure, outstanding obligations, and state registrations, and receive a tailored dissolution roadmap. The plan accounts for shareholders requiring formal votes, contracts needing termination, and multi-state registrations that must be withdrawn before Massachusetts accepts your dissolution filing.

💡 Tip: Our platform delivers a state-specific timeline with required filings, tax clearance procedures, and creditor notification requirements in the correct sequence. You see what must happen before filing Articles of Dissolution, what follows after, and which agencies need separate closure confirmations. This eliminates the guesswork about whether you handled everything or missed an obligation that surfaces months later.

"Starcycle prevents costly mistakes by structuring dependencies into the workflow—you cannot mark a step complete until prerequisites are verified."

⚠️ Warning: Our system tracks status across IRS accounts, Massachusetts Department of Revenue filings, registered agent services, and business licenses, so nothing falls through the cracks between agencies that don't communicate with each other. This comprehensive tracking prevents the costly oversights that typically plague business closures.

Documentation Type | Purpose | Storage Location |

|---|---|---|

Articles of Dissolution | Legal closure proof | Starcycle Platform |

Tax Clearance Confirmations | Revenue compliance | Starcycle Platform |

Closed Account Letters | Financial closure | Starcycle Platform |

Creditor Notification Records | Liability protection | Starcycle Platform |

🔑 Takeaway: You finish with documentation proving closure: accepted Articles of Dissolution, tax clearance confirmations, closed account letters, and creditor notification records stored in one place. When someone asks if your company is fully dissolved, you have proof. That finality means you start your next project without wondering if compliance gaps will resurface during background checks or investor reviews.