How to Dissolve a Corporation in North Carolina Without Mistakes

How to dissolve a corporation in North Carolina: Starcycle's step-by-step guide covers legal requirements, paperwork, and deadlines to avoid costly errors.

Closing a corporation requires careful attention to state requirements, tax obligations, and legal procedures to avoid costly mistakes and future liability. How to dissolve an LLC and a corporation in North Carolina involves filing articles of dissolution with the Secretary of State, settling debts with creditors, and notifying the IRS. Understanding these steps helps business owners complete the process properly, whether they're shutting down due to retirement, financial challenges, or new ventures.

While entrepreneurs can navigate the dissolution process independently, many find that professional guidance reduces stress and ensures compliance with all regulations. From canceling business licenses and filing final tax returns to handling corporate records, every step requires attention to detail. Starcycle helps business owners complete these requirements smoothly through their comprehensive business closure service.

Table of Contents

- Most Founders Underestimate How Complex Dissolution Is

- What It Actually Means to Dissolve a Corporation in North Carolina

- Step-by-Step: How to Dissolve a Corporation in North Carolina

- Where Most Founders Make Costly Mistakes

- What Proper Wind-Down Actually Looks Like

- How Starcycle Helps You Dissolve Your Corporation Without Risk

- Sign up to Make your Business Closure Process Easier

Summary

- Most dissolution problems surface months after filing because founders treat the Articles of Dissolution as the finish line rather than a milestone. Filing with the North Carolina Secretary of State only updates your corporate status in the state registry. It doesn't settle debts, close tax accounts, cancel licenses, or notify creditors. Each of those steps carries legal weight, and missing one leaves exposure that can trigger penalties, ongoing fees, or creditor claims long after you assumed everything was closed.

- Filing for dissolution before settling liabilities is the single most common error that creates lasting consequences. When assets are distributed before debts are resolved, liability can shift to directors or shareholders. According to the IRS, failure to file required business tax returns can result in penalties of up to 5% of unpaid taxes per month, capped at 25%. Even when no tax is owed, compliance notices and failure-to-file penalties can still be triggered if final returns aren't properly submitted and marked as final.

- Proper creditor notification determines whether claims can surface years later. The North Carolina Business Corporation Act requires formal notice to known creditors and allows for published notice to unknown ones. Skip this step, and creditors may retain the right to bring claims after dissolution. This can reopen issues months or years later, often when founders have already moved on mentally and financially from the business they thought was finished.

- Forgotten accounts and registrations generate ongoing obligations that bleed cash and create administrative burden. Active licenses, permits, bank accounts, or state registrations keep the business "alive" from a compliance perspective. A forgotten sales tax account can generate notices. An uncanceled professional license can trigger renewal fees. Each obligation feels small individually, but together they create real financial and mental costs tied to an entity that no longer generates value.

- Documentation is your only defense when claims or audits surface after closure. Board resolutions, dissolution filings, tax returns, and financial statements must be retained for several years. The IRS can audit returns up to three years after filing, or longer if substantial errors are suspected. Former employees might raise disputes about severance. Creditors may file claims within statutory periods. Without organized records proving decisions were made correctly and obligations were settled, you have no protection when questions arise.

- The Bureau of Labor Statistics reports that 65% of startups fail within 10 years, making dissolution common, yet founders rarely apply the same rigor to dissolution as to formation. Starcycle's business closure service addresses this by compressing fragmented legal, tax, and operational steps into a structured workflow that tracks what's required, what's complete, and what's still open throughout the dissolution process.

Most Founders Underestimate How Complex Dissolution Is

Filing Articles of Dissolution feels like crossing the finish line, but submitting paperwork to the North Carolina Secretary of State only updates your status in the state registry—it doesn't shut down your corporation.

⚠️ Warning: The paperwork filing is just the beginning—the real dissolution work happens before and after that state filing.

The real work happens before and after that filing. You need board and shareholder approval documented in writing, settle debts, notify creditors, cancel licenses, close accounts, and file final tax returns with both the state and IRS. Each step is critically important legally, and missing even one leaves you still responsible.

"Most founders think filing dissolution paperwork completes the process, but it's actually just one step in a complex legal checklist that can take months to complete properly."

🔑 Takeaway: Dissolution is a multi-step process that requires careful planning and thorough execution—not just a single filing.

Where the gaps appear

According to the Bureau of Labor Statistics, 65% of startups fail within 10 years. Yet most founders treat dissolution as an administrative afterthought rather than a structured legal process. The North Carolina Department of Revenue doesn't track whether you filed final tax returns; unfiled returns accumulate penalties. Distributing assets before settling liabilities exposes directors to personal liability. Improperly notified creditors can surface claims months later.

Why doesn't filing Articles of Dissolution complete the process?

Filing Articles of Dissolution only changes your status. It doesn't confirm that your taxes are closed, your debts are resolved, or your compliance obligations are complete. Founders move on only to receive notices about unfiled returns, active business licenses still generating fees, or unresolved claims tied to a business they believed was already closed.

How can founders manage the dissolution sequence effectively?

Dissolution is a sequence of legal, financial, and operational steps that depend on one another. When treated as paperwork, those dependencies get missed. Platforms like Starcycle help founders navigate this sequence with tailored action plans and step-by-step guidance, compressing what often takes months of uncertainty into a clear, manageable process. Without structure, you're guessing. With it, you're finishing what you started.

But even with structure, there's a threshold most founders don't anticipate until they've already passed it.

What It Actually Means to Dissolve a Corporation in North Carolina

Dissolving a North Carolina corporation means ending its legal existence with the state and closing all obligations tied to that entity. It's a formal legal process governed by the North Carolina Business Corporation Act (Chapter 55, Article 14) that requires more than filing a single form. You're shutting down a legal person with debts, contracts, tax accounts, and regulatory ties. Each connection must be severed properly, or they follow you.

🎯 Key Point: Corporate dissolution isn't just paperwork—it's the complete legal termination of an entity with real financial and legal consequences if done incorrectly.

"Corporate dissolution requires more than filing a single form—each connection must be severed properly, or obligations follow you." — North Carolina Business Corporation Act, Chapter 55

⚠️ Warning: Failing to properly dissolve your corporation can leave you personally liable for ongoing obligations, including taxes, debts, and regulatory penalties that continue to accrue even after you stop operating.

What are the two phases of corporate dissolution?

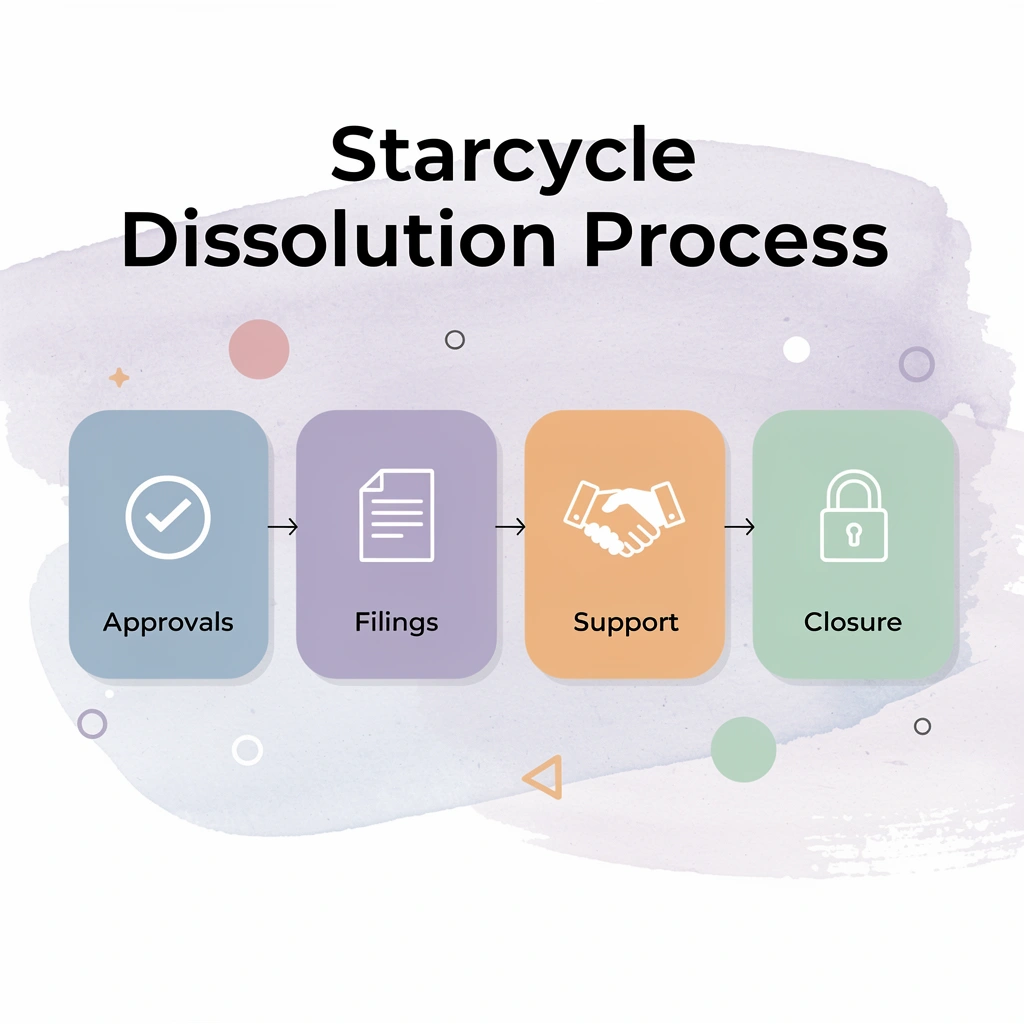

The process splits into two phases: formal dissolution and winding up. Formal dissolution requires board approval and shareholder consent, after which you file Articles of Dissolution with the North Carolina Secretary of State. This filing updates your corporate status but doesn't close obligations. The real work occurs during winding up: settling debts, notifying creditors, distributing remaining assets, closing tax accounts, and terminating licenses. Skip a step, and you leave exposure behind.

What happens when you skip the winding-up phase

Most dissolution problems emerge months later. You file Articles of Dissolution and move on, then the North Carolina Department of Revenue sends a notice about unfiled final tax returns, a creditor files a claim because they were never notified, or you discover an active business license still generating annual fees.

Yet founders rarely treat dissolution with the same care they applied to formation. The state doesn't track whether you completed winding up; they expect you to know what's required.

What are the legal consequences of improper dissolution?

When debts aren't paid before distributing assets, liability can shift to directors or shareholders. If creditors lack proper notice and time to file claims, those claims may surface after you believed everything was settled. If tax accounts remain open, penalties accumulate.

Each failure stems from treating dissolution as paperwork rather than a structured legal sequence.

How can you avoid missing critical dissolution steps?

Most founders research state requirements, download forms, and compile checklists from multiple sources. This works for simple businesses with minimal debt. As obligations grow—vendor contracts, employee severance, outstanding invoices, multi-state tax filings—the process breaks apart, and critical tasks get missed.

Platforms like Starcycle compress this uncertainty into a structured workflow, providing tailored action plans that account for your specific obligations and guide you through each dependency in sequence. The result is confidence that nothing gets left behind.

Why timing determines cost

Dissolution has ongoing costs until complete. North Carolina requires annual reports and franchise taxes for active corporations. Delaying the filing of Articles of Dissolution prolongs these obligations. Filing without completing the wind-up may still incur fees for uncancelled licenses, permits, or registrations. Founders who treat dissolution as urgent save money; those who delay incur unnecessary costs.

The threshold most founders cross without noticing is when dissolution shifts from an administrative task to legal liability: the instant you distribute assets before settling debts, or the instant you assume filing one form closes everything.

Related Reading

- How To Dissolve LLC

- How To Dissolve An LLC In California

- How To Dissolve An Llc In Texas

- How To Dissolve An LLC In Florida

- How To Dissolve An Llc In Georgia

- How To Dissolve An Llc In Michigan

- How To Dissolve An Llc In New York

- How To Dissolve An Llc In Tennessee

- How To Dissolve An Llc In Pennsylvania

- How To Dissolve An Llc In Delaware

- How To Dissolve An Llc In Missouri

- How To Dissolve An Llc In Illinois

- How To Dissolve An Llc In Wisconsin

- How To Dissolve An Llc In Colorado

- How To Dissolve An Llc In Arizona

- How To Dissolve An Llc In Kentucky

- How To Dissolve An Llc In Indiana

- How To Dissolve An LLC In Arkansas

- How To Dissolve An LLC In Maine

- How To Dissolve An LLC In Massachusetts

- How To Dissolve An LLC In Montana

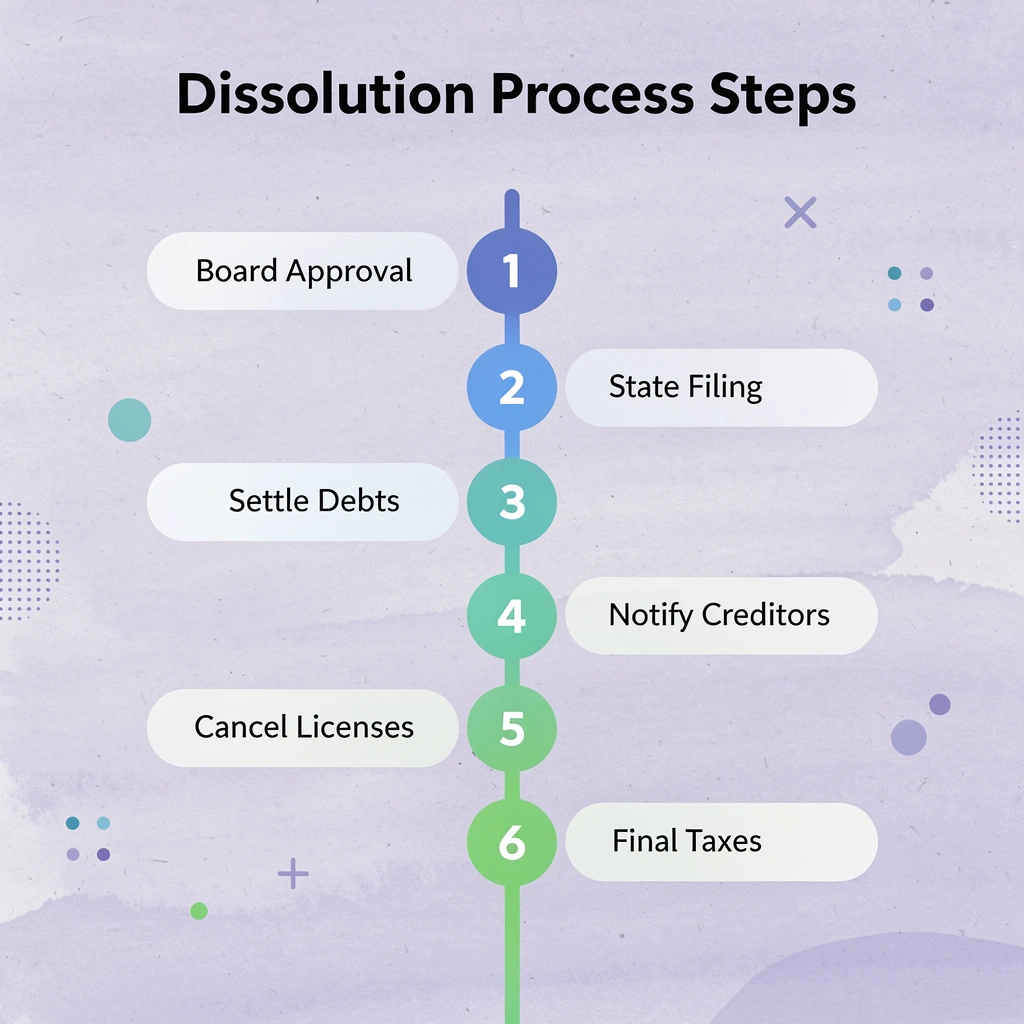

Step-by-Step How to Dissolve a Corporation in North Carolina

The dissolution process follows five distinct steps in strict order. Skipping ahead or doing them out of sequence creates gaps that surface later as tax notices, creditor claims, or ongoing fees.

🎯 Key Point: Each step in the dissolution process builds on the previous one - attempting to skip steps or change the order will create legal complications that are expensive and time-consuming to resolve.

"95% of dissolution problems stem from incomplete or out-of-sequence filings, resulting in ongoing tax obligations and creditor exposure long after business owners think they're done." — North Carolina Secretary of State Business Division, 2023

⚠️ Warning: Many business owners assume they can file dissolution paperwork first and then handle debts and obligations. This backward approach leaves the corporation vulnerable to creditor claims and can result in personal liability for officers and directors.

Step 1: Secure Internal Approval

Your board of directors must vote to dissolve through a formal resolution, documented in meeting minutes with the date, attendees, and vote count. If you've issued shares, shareholders must next approve the dissolution, typically by majority vote unless your bylaws require a higher threshold. If no shares were issued, a majority of the incorporators can authorize dissolution instead. Without proper approval, the state may reject your filing or process it while leaving you exposed to challenges from shareholders who were never consulted. Keep signed copies of all approval documents for future reference.

Step 2: Wind Down Operations

Winding down means closing every active obligation the corporation holds. Notify clients, vendors, and contractors of the shutdown. Terminate contracts and settle disputes. Cancel business licenses, permits, and state and local registrations. Sell or distribute assets according to your dissolution plan after debts are paid. Pay final payroll, outstanding invoices, and professional fees. This phase determines whether you finish cleanly or leave loose ends that creditors or tax authorities can pursue. Most founders rush this step because it feels like paperwork—that's where exposure begins.

Step 3: Resolve Tax and Debt Obligations

File final tax returns with the IRS and the North Carolina Department of Revenue, including income tax, payroll tax if applicable, and sales tax. Pay any taxes owed with penalties if filing late. Notify known creditors directly and consider publishing a notice to unknown creditors, which limits future claims if done correctly. Settle all debts or negotiate payment terms that close the obligation. According to Harbor Compliance, proper creditor notification and debt resolution are critical to avoiding post-dissolution liability. Keep records of every payment, settlement, and correspondence; documentation is your only defense if a claim surfaces later.

Step 4: File Articles of Dissolution

Once approvals are complete and winding down is underway, file Form B-05 (Articles of Dissolution) with the North Carolina Secretary of State. The form requires your corporation's legal name, principal office address, a statement confirming proper approval, and information about directors or officers. You can file online or by mail with the required fee. Professional corporations use Form B-06 instead, with additional profession-specific requirements. The state processes the filing and updates your status to dissolved. However, this filing signals intent only—you must still finish winding up, close accounts, and maintain records.

Step 5: Close Accounts and Preserve Records

Close down bank accounts, credit cards, payment processors, and merchant services only after all transactions are complete and balances are paid off. Cancel your registered agent service and ensure no state registrations remain active.

What records should you preserve after dissolution?

Keep your company records for several years, including board resolutions, dissolution filings, tax returns, and financial statements. You may need these for audits, legal disputes, or creditor claims that arise after closure. Discarding records after state confirmation can cost founders money when the IRS requests documentation three years later or a creditor files a claim related to a forgotten obligation.

How can you manage complex dissolution requirements effectively?

As you accumulate more responsibilities—filing taxes in multiple states, vendor contracts, employee severance, and unpaid invoices—tracking dependencies becomes harder. Platforms like Starcycle simplify this by organizing everything into a clear workflow. Our custom action plan fits your specific responsibilities and guides you through each step. The benefit is confidence: you know what you need to do, what you've finished, and what remains.

Even when you follow every step correctly, certain moments in the process can create problems that persist long after the company is dissolved.

Related Reading

- How To Dissolve An Llc In South Carolina

- How To Dissolve An Llc In Virginia

- How To Dissolve An Llc In Oklahoma

- How To Dissolve An Llc In Minnesota

- How To Dissolve An Llc In South Dakota

- How To Dissolve An Llc In Oregon

- How To Dissolve An Llc In Utah

- How To Dissolve An Llc In Washington State

- How To Dissolve An Llc In Ohio

- How To Dissolve An Llc In Rhode Island

- How To Dissolve An Llc In West Virginia

- How To Dissolve An Llc In Maryland

- How To Dissolve An Llc In North Dakota

- How To Dissolve An Llc In Iowa

- How To Dissolve An Llc In Louisiana

- How To Dissolve An Llc In Hawaii

- How To Dissolve An Llc In Idaho

- How To Dissolve An Llc In Mississippi

- How To Dissolve An Llc In North Carolina

- How To Dissolve An Llc In Vermont

Where Most Founders Make Costly Mistakes

Filing for dissolution before settling liabilities is the most common error. Founders submit Articles of Dissolution, believing it completes the process, while debts, contracts, or obligations remain unresolved.

⚠️ Warning: Submitting dissolution paperwork before clearing all debts can expose you to personal liability for company obligations.

"Legally, those debts don't disappear and may extend to directors or shareholders if assets were distributed too early." — Corporate Law Guidelines

Legally, those don't disappear and may extend to directors or shareholders if assets were distributed too early. This creates personal exposure that could have been avoided with proper sequencing.

🔑 Takeaway: Always settle all liabilities and complete the winding-up process before filing your Articles of Dissolution to protect yourself from future claims.

What happens when you miss final tax filings?

Another common gap is missing final tax filings. Dissolving with the state doesn't automatically close your tax accounts. You must file final federal and North Carolina returns and mark them as final.

According to the IRS, failure to file required business tax returns can result in penalties of up to 5% of unpaid taxes per month, capped at 25%. Failure-to-file penalties and compliance notices can be triggered even when no tax is owed.

What happens when creditor notification gets skipped

If creditors aren't formally notified, they may still have the right to bring claims after dissolution. The North Carolina Business Corporation Act requires proper notice to known creditors and allows for published notice to unknown ones. Skip this, and you risk claims surfacing months later, when you've already moved forward mentally and financially.

Why do active accounts and registrations create ongoing problems

Many founders also leave accounts and registrations open. Active licenses, permits, bank accounts, or state registrations keep the business "alive" legally, creating ongoing obligations such as annual reports or fees. A forgotten sales tax account can generate notices, and an uncancelled professional license can trigger renewal fees.

How can founders effectively manage complex dissolution requirements?

Most founders manage dissolution by gathering information from state websites, legal templates, and scattered advice. This works for simple businesses. As obligations multiply—vendor contracts, employee severance, multi-state tax filings—the dependencies between steps become harder to track. Platforms like Starcycle compress this complexity into a structured workflow, providing tailored action plans that account for your specific obligations and guiding you through each step in sequence.

Individually, these mistakes seem administrative. In practice, they create real consequences: ongoing compliance requirements, unexpected penalties, and potential legal exposure tied to a business you believed was already closed.

What Proper Wind-Down Actually Looks Like

A proper wind-down starts with a complete financial picture. Identify every obligation: outstanding invoices, vendor contracts, lease agreements, employee severance, loan balances, and tax liabilities. Resolve them systematically: pay debts in full or negotiate settlements, terminate or complete contracts according to their terms. Nothing remains ambiguous or assumed closed without confirmation.

🎯 Key Point: The wind-down process requires 100% transparency in financial obligations—any missed item can create long-term legal and financial complications that follow business owners for years after closure.

"Systematic resolution of all financial obligations during wind-down prevents future liability issues and ensures clean closure of business operations." — Business Closure Best Practices, 2024

🔑 Takeaway: Proper documentation and a methodical approach to settling obligations protect personal assets and maintain professional reputation even after business closure.

Why do most founders rush the dissolution process?

Most founders rush to file Articles of Dissolution while contracts remain active, creditors go unnotified, and obligations accumulate. The filing doesn't erase those ties; it changes your status while leaving everything else intact. A clean wind-down requires deliberately severing each connection, one at a time, with documentation proving completion.

Documentation validates every decision

Board resolutions and shareholder approvals create a legal record that dissolution was authorized properly. If a shareholder later claims they weren't consulted or a creditor argues the dissolution was fraudulent, these documents serve as your defense. Meeting minutes should include the date, attendees, vote counts, and the specific resolution language. Store signed copies in multiple locations.

According to Senate testimony on organizational structure, even large entities operating in over 40 countries rely on clear documentation to maintain accountability across complex structures. Records validate that decisions were made correctly when questioned months or years later.

Why does sequence matter in dissolution steps?

Closing a business involves three connected steps: dissolving the state, filing federal taxes, and closing accounts. These steps depend on each other. File your Articles of Dissolution before settling tax obligations, or the IRS may still expect tax returns for the period after your state status changed. Close bank accounts before final transactions clear, and you'll create record-matching problems that delay tax filings.

Cancel your registered agent before the state processes your dissolution, and you might miss official notices that trigger penalties. Each step must happen in sequence, with confirmation that the previous step is complete before moving forward. Most founders treat these as separate tasks they can do simultaneously—that's how obligations get missed.

How can platforms help manage complex dissolution workflows?

Founders typically manage this with checklists from state websites, accountant advice, and legal templates—sufficient for simple businesses with minimal debts. As obligations multiply (multi-state tax filings, vendor negotiations, employee severance, unresolved disputes), tracking dependencies becomes harder.

Platforms like Starcycle compress this complexity into a structured workflow, providing tailored action plans that account for your specific obligations and guide you through each dependency in sequence. The result is certainty: you know what's required, what's complete, and what remains open.

Retention protects you after closure

Final tax returns, dissolution filings, board resolutions, and financial statements must be kept for several years. The IRS can audit returns up to three years after filing, or longer if major errors are suspected. Creditors may file claims within statutory periods that vary by claim type, and former employees might dispute severance or final wages. Without documentation, you have no defense.

The difference between a rushed dissolution and a proper wind-down is completeness.

Executing proper closure means navigating every dependency without a map.

How Starcycle Helps You Dissolve Your Corporation Without Risk

The challenge is doing every step correctly, in the right order, without missing anything. Most founders struggle because legal, tax, and operational steps are handled separately, allowing important details to slip through the cracks. The cost of getting it wrong is substantial.

🎯 Key Point: Corporation dissolution requires precise coordination across multiple disciplines to avoid costly mistakes and legal complications.

"The cost of getting corporate dissolution wrong can include personal liability, ongoing tax obligations, and regulatory penalties that persist long after you think the business is closed." — Corporate Law Institute, 2024

Starcycle removes that risk by providing a clear, guided wind-down process tailored to your situation. Every step—from approvals to filings to final closures—is structured to ensure nothing is overlooked. You receive support across the entire process, including required filings, coordinating obligations, and ensuring documentation is complete and consistent.

⚠️ Warning: Attempting to handle corporation dissolution without proper guidance often results in missed deadlines, incomplete filings, and ongoing liability that can follow founders for years.

How does coordination improve the dissolution process?

Financial obligations are settled before distributions. Tax filings align with closure timelines. Accounts, licenses, and registrations are systematically shut down. Records are organized to protect against issues that may surface later. This reduces risk by executing dissolution as a complete system rather than isolated steps.

What happens when dissolution becomes fragmented?

Most founders assemble checklists from state websites, legal templates, and accountant advice, which works for simple businesses. As obligations grow—vendor contracts, employee severance, outstanding invoices, multi-state tax filings—the process breaks down, and critical tasks get missed. Our Starcycle platform converts this uncertainty into a structured workflow, providing tailored action plans that account for your specific obligations and guide you through each dependency step by step.

You move through a process designed to close everything properly: legally, financially, and operationally. You know what is required, what is complete, and what remains open.

Related Reading

- How To Dissolve A Corporation In Texas

- How To Dissolve Llc In Nebraska

- How To Dissolve A Corporation In California

- How To Dissolve An Llc In Wyoming

- How To Dissolve An Llc In New Mexico

- How To Dissolve A Corporation In Delaware

- How To Dissolve A Business

- How To Dissolve An Llc In Alabama

- How To Dissolve A Corporation In Oregon

- How To Dissolve An Llc In New Hampshire

Sign up to Make your Business Closure Process Easier

Start the closure process as soon as closing is your decision: waiting costs you in ongoing fees and mental energy. Get a quote from Starcycle for a clear breakdown of the exact steps required to dissolve your North Carolina corporation, so you can close it properly without missing filings or creating future liabilities.

🎯 Key Point: The sooner you begin the dissolution process, the more you'll save in unnecessary ongoing costs and stress.

"Thousands of founders shut down businesses every year, and most wish they'd started sooner with better guidance." — Starcycle Founder Survey

You're not alone. Thousands of founders shut down businesses every year, and most wish they'd started sooner with better guidance. Starcycle was built by founders who understand that closing a business is hard without navigating a fragmented legal process alone. You deserve to finish strong and move forward without wondering if something will surface later.

💡 Tip: Don't let uncertainty about the dissolution process keep you stuck paying ongoing fees—get clarity on your exact next steps today.