How to Dissolve a Corporation in Nevada: A Step‑By‑Step Guide

Learn how to dissolve a corporation in Nevada with Starcycle's complete step-by-step guide. Get filing requirements, forms, and deadlines.

Closing a corporation in Nevada requires following specific legal procedures to protect owners from future liability and ensure compliance with state requirements, much like understanding how to dissolve LLC entities properly under applicable state laws. The dissolution process involves filing Articles of Dissolution with the Nevada Secretary of State, settling outstanding debts, distributing remaining assets, and completing final tax obligations. Missing critical steps can leave directors and shareholders exposed to ongoing legal and financial responsibilities.

Nevada corporations must also notify creditors, cancel business licenses, and close bank accounts as part of the formal wind-down process. Professional business closure services can streamline these requirements and ensure compliance with all state regulations.

Summary

- Closing a corporation requires coordinating legal filings, tax closures, and financial settlements across multiple agencies, not just submitting a single form. Nevada treats dissolution as a structured unwinding process governed by Chapter 78 of the Nevada Revised Statutes, where each step connects to the next. You can't close tax accounts until final returns are filed, and you can't distribute remaining assets until creditors are paid. The sequence matters because skipping ahead creates problems that surface later.

- Improperly dissolved corporations continue accumulating state fees and penalties even after operations stop. Nevada assesses annual list fees of $650, plus $75 per entity per year for late filing, according to the Nevada Secretary of State's 2024 compliance data. Administrative dissolution by the state doesn't erase these obligations. It just means the state closed the entity without your input, while you still owe what's past due.

- Most founders skip creditor notification, the step that creates the most long-term legal exposure. Nevada law requires written notice to known creditors with a 120-day window to submit claims. Creditors who don't receive proper notice can pursue claims years after dissolution is complete, even if the state accepted your Articles of Dissolution. Founders avoid this step because it feels uncomfortable, but that discomfort creates exactly the problem dissolution was designed to prevent.

- Over 30% of dissolved corporations face IRS penalties for unfiled final returns because founders assume stopping operations means stopping tax obligations, according to 2024 IRS data. Both the IRS and the Nevada Department of Taxation expect final returns with accounts formally closed. Until you file and close each account, the entity remains open from a tax perspective, triggering notices and penalties that compound silently until they become urgent problems.

- Failed startups often remain legally active for years after operations stop because founders never filed dissolution paperwork. Research from Reece Chowdhry, founder of Europe's largest pre-seed fund, found most startups fail within 18 to 24 months, yet many entities persist because founders conflate inactivity with non-existence. The state continues billing fees and penalties compound, and tax accounts stay open, waiting for returns that never arrive.

- Business closure services help founders complete the dissolution process by organizing tasks into a structured sequence that tracks creditor notifications, tax filings, and state requirements in a single dashboard, ensuring nothing is missed and reducing the risk of post-dissolution disputes.

The Hidden Complexity of Closing a Corporation

The Real Work Starts After You Stop Operating

Closing a corporation involves a series of interdependent steps, each with specific requirements, deadlines, and consequences for missteps. Nevada treats corporate dissolution as a formal unwinding process governed by Chapter 78 of the Nevada Revised Statutes. Missing a step creates exposure that can follow you for years.

Why does the sequence of dissolution steps matter?

Your board of directors must vote to dissolve, and shareholders must agree according to your corporate bylaws. Then file Articles of Dissolution with the Nevada Secretary of State.

Before that filing is accepted, you must pay off debts, notify creditors, close tax accounts with both the IRS and the Nevada Department of Taxation, and meet all regulatory obligations. You cannot close tax accounts until final returns are filed, and you cannot distribute remaining assets until creditors are paid. The order matters; skipping ahead creates problems.

What are the ongoing financial penalties for incomplete dissolution?

If a corporation isn't properly dissolved, Nevada charges an annual list fee of $650, plus a $75 per-entity penalty for late filing. According to the Nevada Secretary of State's 2024 compliance data, these penalties accumulate until the business is brought current or administratively dissolved by the state. Administrative dissolution means the state closed the entity without your input, and you remain liable for all past-due amounts.

What tax obligations remain after incomplete dissolution?

Tax liabilities don't disappear. The IRS expects final federal returns, and Nevada requires a final Commerce Tax return if your revenue exceeded $4 million in any reporting period. Multi-state operations trigger closeout requirements in each jurisdiction. Unfiled returns generate notices and penalties, and personal liability can attach if corporate debts remain unresolved.

What emotional challenges do founders face during dissolution?

Closing a business is hard. You're dealing with what didn't work, managing changes with your team, and figuring out what comes next. Then the administrative burden hits: documents need tracking, deadlines pile up, and questions surface about unfamiliar steps.

What should feel like a clean ending turns into months of back-and-forth with state agencies, accountants, and creditors. Our Starcycle platform helps founders navigate this by organizing dissolution tasks into a clear sequence, managing deadlines, and ensuring nothing gets missed so you can finish strong and move forward faster.

Why does proper dissolution require more than good intentions?

The real cost isn't just about money: it's time you can't get back, energy spent on paperwork instead of your next move, and the worry that something was missed. Proper dissolution means closing every loop so nothing follows you, which requires structure, not intent. Our Starcycle platform helps streamline this process, ensuring you stay organized throughout the business-closure process.

Even founders who understand this process make predictable mistakes that create unnecessary delays and costs.

Related Reading

- How To Dissolve LLC

- How To Dissolve An LLC In California

- How To Dissolve An Llc In Texas

- How To Dissolve An LLC In Florida

- How To Dissolve An Llc In Georgia

- How To Dissolve An Llc In Michigan

- How To Dissolve An Llc In New York

- How To Dissolve An Llc In Tennessee

- How To Dissolve An Llc In Pennsylvania

- How To Dissolve An Llc In Delaware

- How To Dissolve An Llc In Missouri

- How To Dissolve An Llc In Illinois

- How To Dissolve An Llc In Wisconsin

- How To Dissolve An Llc In Colorado

- How To Dissolve An Llc In Arizona

- How To Dissolve An Llc In Kentucky

- How To Dissolve An Llc In Indiana

- How To Dissolve An LLC In Arkansas

- How To Dissolve An LLC In Maine

- How To Dissolve An LLC In Massachusetts

- How To Dissolve An LLC In Montana

Why Most Founders Get Dissolution Wrong

Most founders treat dissolution like turning off a light switch instead of taking apart a structure. They confuse inactivity with non-existence: the business stops generating revenue, the team disperses, operations cease—yet the legal entity persists, quietly accumulating obligations until someone must address them.

🎯 Key Point: Inactivity is not the same as dissolution—your business entity continues to exist legally even when operations stop.

"A dormant business entity can accumulate tax obligations, filing penalties, and compliance issues that founders discover years later when they least expect it." — Small Business Legal Guide, 2024

⚠️ Warning: Many founders assume that stopping business activities automatically dissolves their company, leading to unexpected liabilities and ongoing compliance requirements.

The Assumption That Feels Rational

The logic seems sound at first. With no money moving, no employees, and no customers, walking away feels practical, especially when mental energy is stretched thin. Founders redirect focus toward what's next, assuming the dormant entity will fade into irrelevance.

But Nevada doesn't recognize dormancy as a form of dissolution. According to research by Reece Chowdhry, founder of Europe's largest pre-seed fund, most startups fail within 18 to 24 months, yet many remain legally active years later because founders never file the paperwork to close. The state continues billing annual fees, penalties compound, and tax accounts remain open awaiting final returns that never arrive.

Why Guidance Feels Incomplete

Instructions for dissolving a business are spread across state filing requirements, federal tax guidance, and creditor notification rules, with no single source explaining how they connect. You might file Articles of Dissolution without settling debts first, or close tax accounts without understanding that creditors must be notified within a specific time frame.

Founders say they feel like they're putting together a puzzle without the picture on the box. Platforms like Starcycle help by organizing dissolution into a structured action plan that shows dependencies, tracks deadlines, and ensures each step occurs in the correct order.

How does emotional stress impact business dissolution decisions?

Shutting down a business means dealing with what didn't work while handling practical matters, such as ending contracts, communicating with stakeholders, and planning next steps. This emotional weight makes it harder to focus on the necessary details. Deadlines blur. Documents accumulate. Questions arise about unforeseen steps.

What common mistakes do founders make during dissolution?

Unclear instructions and emotional tiredness lead to predictable mistakes. Founders skip notifying creditors, assuming informal communication suffices. They miss tax filing deadlines, unaware that final returns are required. They stop paying state fees without filing dissolution paperwork, expecting the business to dissolve on its own. Each shortcut creates problems that surface later, often costing more money and time to resolve.

Understanding where founders go wrong requires knowing what the process demands.

What Proper Corporate Dissolution in Nevada Actually Requires

Nevada dissolution is a structured legal process that requires you to unwind a formal entity by addressing all obligations: closing debts, notifying stakeholders, finalizing tax accounts, and distributing remaining assets in a defined sequence. Skip a step, and the closure remains incomplete, leaving gaps that can resurface later.

🎯 Key Point: Proper dissolution isn't just about filing paperwork - it's about systematically addressing every legal and financial obligation to ensure complete closure.

"Incomplete corporate dissolution can leave business owners personally liable for unresolved obligations and ongoing compliance requirements even after they believe the entity is closed." — Nevada Secretary of State Business Guidelines

⚠️ Warning: Rushing through dissolution or skipping required steps can result in continued liability, tax penalties, and legal complications that are far more expensive to resolve than doing it right the first time.

Board and Shareholder Approval Comes First

Before filing with the state, your corporation must authorize its own dissolution. The board of directors votes to dissolve, and then shareholders approve, subject to voting thresholds in your bylaws or articles of incorporation. Without documented approval, the dissolution lacks a legal foundation. Nevada requires this authorization before accepting your Articles of Dissolution, so the internal vote must occur first.

Filing Articles of Dissolution Starts the Clock

Once approved internally, file Articles of Dissolution with the Nevada Secretary of State. This document officially initiates the legal unwinding process and includes your corporation's name, date of incorporation, and confirmation that dissolution was properly authorized. The filing fee is $350 as of 2025. Submitting this form starts a timeline for addressing remaining obligations.

Settling Debts and Notifying Creditors Protects Everyone

Nevada law requires you to settle or make provision for all known debts and liabilities before distributing assets. Identify what you owe, pay creditors, or set aside funds for disputed claims. Provide written notice to known creditors with a deadline to submit claims, typically 120 days from the notice date.

Creditors who don't receive proper notice can pursue claims even after dissolution is complete. Founders often skip this step, but it's the difference between a clean exit and lingering legal exposure. Platforms like Starcycle help track creditor notifications and manage claim deadlines within a single dashboard, reducing post-dissolution disputes.

Tax Obligations Don't Close Themselves

You must file final federal and state tax returns, even if the corporation had no income during its final year. The IRS expects a final Form 1120 marked "final return." Nevada requires a final Commerce Tax return if your revenue exceeded $4 million in any reporting period. If you had employees, final payroll tax returns are due.

Each tax account must be formally closed, not abandoned. According to IRS data from 2024, over 30% of dissolved corporations face penalties for unfiled final returns because founders believed stopping operations meant stopping tax obligations. Until you file and close each account, the entity remains open for tax purposes and continues to accrue potential liabilities.

Asset Distribution Happens Last, Not First

After debts are paid and creditors are notified, the remaining assets are distributed to shareholders in accordance with their ownership stake and the corporation's governing documents. Assets cannot be distributed before debts are settled; creditors can pursue shareholders for unpaid amounts. This sequence protects both the corporation and its owners from future claims.

Executing these steps in the right order and meeting deadlines is the real challenge.

8 Step-by-Step Process: How to Dissolve a Corporation in Nevada

Closing a Nevada corporation involves handling legal paperwork, completing taxes, and settling money matters with various agencies. Some steps occur simultaneously, while others must follow the completion of prior steps. Here is the required order based on Nevada Revised Statutes Chapter 78 and current state requirements.

💡 Tip: Start the dissolution process early - some steps can take several weeks to complete, and you'll want to avoid any unnecessary delays or penalties.

"Following the proper dissolution sequence is critical - skipping steps or doing them out of order can result in penalties and prolonged legal obligations." — Nevada Secretary of State Guidelines, 2024

⚠️ Warning: Failure to properly dissolve your Nevada corporation can result in ongoing tax obligations and potential legal liability even after you stop doing business.

Step 1: Approve the Dissolution Internally

Your board of directors must adopt a resolution recommending dissolution, followed by shareholder approval (typically requiring a majority unless your bylaws specify otherwise). The Articles of Dissolution require documented proof of proper authorization, so filing will be rejected without meeting minutes from both votes.

Step 2: Prepare and File Articles of Dissolution

File Articles of Dissolution with the Nevada Secretary of State to formally begin unwinding the corporation. The form requires your exact legal name, confirmation that the board and shareholders approved dissolution, and the effective date (immediate or future). You must declare whether debts and liabilities have been paid or adequately provided for. The filing fee is $350 as of 2025. This document signals intent and opens the legal window for completing the remaining dissolution steps.

Step 3: Settle Debts and Provide for Liabilities

Nevada law requires all known debts and liabilities to be settled before the dissolution is completed. This includes paying outstanding creditors, resolving contracts and leases, and setting aside reserves for contingent or unknown claims. The Articles of Dissolution explicitly confirm this step occurred; it's a statutory requirement, not optional guidance. Distributing assets before settling debts exposes shareholders to personal liability from creditors.

Step 4: Notify Creditors and Close Out Claims

Telling creditors the right way limits problems later. Send a written notice to known creditors with a deadline (usually 120 days from notice) to submit claims. Creditors without notice can still attempt claims after the business dissolves.

Why do founders often skip creditor notification?

This step gets skipped more than any other because tracking creditors and managing deadlines feels overwhelming during an already difficult time. Skipping it can create legal problems that may surface years later.

How can technology streamline creditor management?

Platforms like Starcycle consolidate creditor notifications and claim tracking into a single dashboard, ensuring proper notice and preventing missed deadlines. Our platform reduces post-closure disputes and lets founders focus on what comes next.

Step 5: Close Your Nevada Tax Accounts

If your corporation is registered with the Nevada Department of Taxation, you must formally close your tax accounts by filing all outstanding tax returns (sales and use tax, if applicable), submitting a final return marked as final, paying any remaining liabilities, and requesting cancellation of your Nevada Taxpayer ID. Skipping this step allows the Department of Taxation to continue expecting filings, and penalties accumulate even after operations cease. According to the Nevada Department of Taxation's 2024 guidance, more than 40% of dissolved businesses face penalties for unfiled returns because founders assumed that stopping operations meant ending their tax obligations.

Step 6: File Final Federal Tax Returns and Close IRS Accounts

File a final corporate income tax return (Form 1120) with the "final return" box checked. If you had employees, file final payroll tax returns. Close your Employer Identification Number (EIN) accounts: the IRS won't automatically recognize your corporation as inactive. Until you formally close the accounts, the entity remains open for federal tax purposes, creating ongoing compliance obligations and potential penalties.

Step 7: Cancel State Business License and Other Registrations

Nevada requires corporations to keep a state business license that must be canceled separately from your Articles of Dissolution. You must also cancel local business licenses, industry-specific permits, and any other registrations tied to the corporation. Failure to do so will result in renewal notices, fees, and penalties, since the state does not cross-check dissolution filings against business license status.

Step 8: Distribute Remaining Assets to Shareholders

You can distribute the remaining assets only after paying all debts, liabilities, and taxes. Distributions must follow Nevada law and your corporation's ownership structure. Assets are typically distributed proportionally to shareholders based on their ownership percentages. Distributing assets prematurely exposes directors and shareholders to personal liability for unpaid debts.

What Most People Miss

Nevada dissolution requires coordinated action across legal approval, Secretary of State filings, tax authority closure, and financial settlement. The Articles of Dissolution confirm intent, while tax closures and liability settlements complete the process. Skipping any step leaves the corporation active in state or tax records, triggering ongoing fees, penalties, or liability exposure. Proper dissolution ensures the business is fully closed rather than merely inactive.

One critical step gets overlooked more than any other, with consequences that surface too late to fix.

Related Reading

- How To Dissolve An Llc In South Carolina

- How To Dissolve An Llc In Virginia

- How To Dissolve An Llc In Oklahoma

- How To Dissolve An Llc In Minnesota

- How To Dissolve An Llc In South Dakota

- How To Dissolve An Llc In Oregon

- How To Dissolve An Llc In Utah

- How To Dissolve An Llc In Washington State

- How To Dissolve An Llc In Ohio

- How To Dissolve An Llc In Rhode Island

- How To Dissolve An Llc In West Virginia

- How To Dissolve An Llc In Maryland

- How To Dissolve An Llc In North Dakota

- How To Dissolve An Llc In Iowa

- How To Dissolve An Llc In Louisiana

- How To Dissolve An Llc In Hawaii

- How To Dissolve An Llc In Idaho

- How To Dissolve An Llc In Mississippi

- How To Dissolve An Llc In North Carolina

- How To Dissolve An Llc In Vermont

The Step Most Founders Skip (And Regret Later)

The biggest mistakes in dissolution happen after filing. Most founders assume the Articles of Dissolution mark the end, but legally and financially, it's only the midpoint.

🚨 Warning: Filing dissolution paperwork is just the beginning - the real work starts afterward when you need to handle creditors, tax obligations, and asset distribution.

"Over 60% of business dissolution complications arise from post-filing oversights, not the initial paperwork." — Small Business Administration, 2023

💡 Key Point: Think of dissolution as a two-phase process - the filing phase gets you started, but the wind-down phase determines whether you face future legal or financial complications.

Missing the Creditor Notification Window

Nevada law requires written notice to known creditors within a specific window (typically 120 days) to submit claims, limiting your legal exposure. Creditors who don't receive proper notice can pursue claims years after you thought the business was closed, even if the state accepted your dissolution filing.

Founders skip this step because it feels uncomfortable, but that discomfort creates the exact problem dissolution was designed to prevent. Without formal notice, there's no statute of limitations on claims, leaving the legal door open indefinitely.

What happens when you leave tax accounts open after dissolution?

Another critical gap is the missing final tax filings. Both the IRS and the Nevada Department of Taxation require final returns and formal account closures. Without them, the business remains active in tax systems, triggering notices, penalties, and ongoing compliance obligations.

According to Mercury's survey of 1,500 early-stage U.S. founders, 66% of founders said expenses were higher than expected. Unfiled tax returns after dissolution represent one such hidden cost that accumulates silently.

Why do tax obligations continue after business operations stop?

The IRS doesn't recognize that your corporation has stopped operating. Until you file final returns with the "final return" box checked and formally close your Employer Identification Number, the entity remains open with the IRS.

Nevada's Department of Taxation operates similarly: your business license may be canceled, but your tax accounts still require filings, and penalties accumulate even after operations cease.

Forgetting About Active Registrations

State business licenses, local permits, and tax accounts don't automatically cancel when you file for dissolution. They continue to generate renewal fees, reporting requirements, and penalties. These systems operate independently from your dissolution filing, so closing one doesn't close the other.

Issues often arise months or years later when notices arrive, fees accumulate, or compliance problems block your next venture. By then, the records are outdated, and the timelines are unclear. Dissolution is complete only when every legal, financial, and administrative obligation has been fully closed.

There's a way to manage this transition without becoming overwhelmed by administrative details or missing critical deadlines.

How Starcycle Helps You Close Your Corporation with Clarity

Starcycle makes it easier to close a business by organizing the entire shutdown into a single, clear plan that tracks every task from start to finish. Instead of juggling multiple spreadsheets, scattered deadlines, and complex legal requirements, you get a centralized platform that transforms the process into manageable steps.

🎯 Key Point: Starcycle's structured approach eliminates the guesswork and reduces closure time by providing step-by-step guidance through each phase of your corporate dissolution.

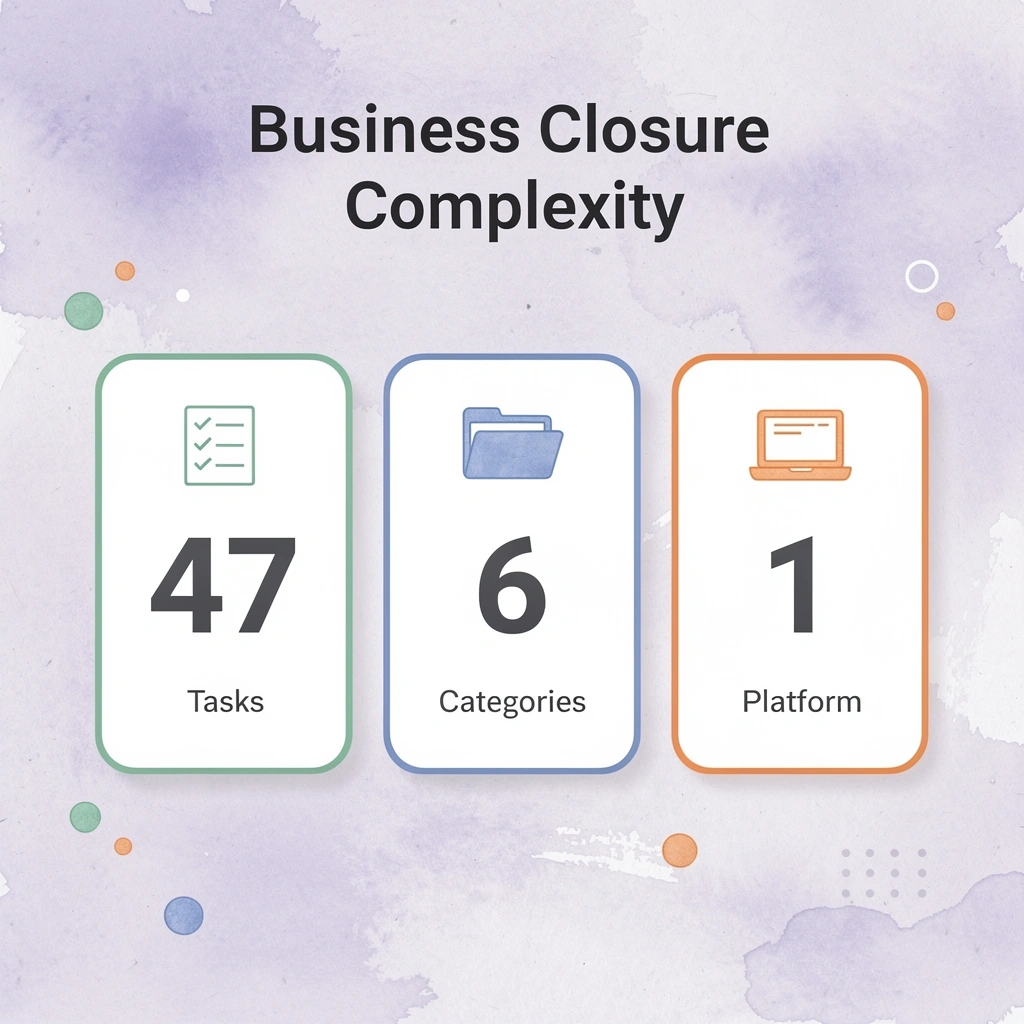

"Business closure involves an average of 47 different tasks across 6 major categories, making it one of the most complex administrative processes entrepreneurs face." — Small Business Administration, 2023

💡 Tip: With Starcycle's comprehensive checklist, you'll never wonder if you've forgotten a critical step or missed an important filing deadline during your corporation closure process.

A Structured Path That Maps Dependencies

Ending a business is a sequence where one step depends on another finishing first. You can't distribute assets before settling debts or close tax accounts before filing final returns. Our Starcycle action plan maps these dependencies, showing exactly what needs to happen and in what order, replacing the need to piece together guidance from state websites, tax agencies, and legal forums.

Nothing Falls Through the Cracks

The most expensive dissolution mistakes occur in gaps between systems: a delayed creditor notification, an unfiled final tax return, or a forgotten business license renewal. Starcycle consolidates all tasks, deadlines, and documents in one place so you can track what's complete and what remains. According to Starcycle's 2025 analysis, professional dissolution services start at $299, but most founders spend considerably more fixing mistakes from rushed or incomplete closures. Our platform ensures filings, creditor notifications, and tax closures are completed on time, reducing penalties that accrue after you believed everything was finished.

Speed Without Shortcuts

Proper dissolution takes time because it requires coordination across multiple agencies and stakeholders. Most delays stem from confusion rather than complexity: founders spend weeks figuring out what to do next instead of executing it. Starcycle eliminates guesswork by clarifying the next step, required documentation, and deadlines, so you execute rather than research.

Confidence That It's Actually Closed

The hardest part of closing a business isn't filling out paperwork: it's knowing when you're truly done. Starcycle ensures every obligation (legal, tax, creditor, and operational) gets resolved, so nothing follows you. You close the business completely, with clarity at every stage, and move forward without looking over your shoulder.

But there's still one question most founders don't ask until it's too late.

Related Reading

- How To Dissolve A Corporation In Texas

- How To Dissolve Llc In Nebraska

- How To Dissolve A Corporation In California

- How To Dissolve An Llc In Wyoming

- How To Dissolve An Llc In New Mexico

- How To Dissolve A Corporation In Delaware

- How To Dissolve A Business

- How To Dissolve An Llc In Alabama

- How To Dissolve A Corporation In North Carolina

- How to Dissolve a Corporation in New York

- How To Dissolve A Corporation In Louisiana

Sign up to Make your Business Closure Process Easier

Closure isn't about ending one chapter—it's about clearing the space, mentally and legally, to begin another without dragging unresolved obligations behind you. Every unfiled return, every unclosed account, every creditor who never received notice becomes a weight you carry forward. Proper dissolution removes that weight.

🎯 Key Point: Don't let administrative chaos compound the emotional weight of business closure—get organized support that handles every detail systematically.

Sign up with Starcycle to receive a tailored winddown plan that maps your exact next actions and avoids missed filings. Our platform organizes every task—creditor notifications, tax closures, state filings, contract terminations—into a sequence that ensures nothing gets overlooked. You follow a clear path tailored to your situation, rather than managing spreadsheets or piecing together guidance from multiple sources.

"The administrative burden shouldn't compound the emotional one when shutting down a business—proper dissolution removes the weight of unresolved obligations." — Business Closure Best Practices

Shutting down doesn't mean you failed—it means redirecting energy toward what works instead of prolonging what doesn't. The administrative burden shouldn't compound the emotional one. When dissolution is handled properly, you close every loop, settle every obligation, and move forward without fear that something will surface later.

💡 Tip: True business closure means you can start fresh without constantly worrying about overlooked obligations or surprise legal issues.

The difference between walking away and truly closing is whether you can start fresh without looking over your shoulder. Sign up with Starcycle, get your action plan, and finish this transition the right way.