How to Dissolve a Corporation in Florida the Right Way

Learn how to dissolve a corporation in Florida with Starcycle's step-by-step guide. Avoid costly mistakes and complete the process correctly.

Closing a business requires careful attention to legal and financial obligations that extend far beyond simply stopping operations. Florida corporations face specific dissolution requirements, including filing Articles of Dissolution with the Florida Department of State, completing final tax returns, notifying creditors, and properly distributing assets. Missing these critical steps can result in ongoing tax liabilities, legal complications, and personal exposure that persist long after the business closes.

The dissolution process involves multiple deadlines and regulatory requirements that must be handled precisely to protect business owners from future complications. Professional guidance ensures each stage of corporate dissolution is completed correctly, from initial filings through final obligations, providing peace of mind during business closure.

Summary

- Filing Articles of Dissolution with Florida's Division of Corporations costs approximately $35 and feels conclusive, but state acceptance only authorizes you to begin the wind-down. It doesn't settle debts, close tax accounts, or terminate contracts. Those obligations remain legally active until you address them directly, regardless of filing status.

- Tax obligations persist after dissolution unless you formally close each account with the Florida Department of Revenue and the IRS. Penalties and interest accumulate on unfiled returns or unpaid balances even after you've filed dissolution paperwork. One founder filed in March, assumed closure was complete, and received notices in October for unpaid sales tax with penalties accruing since April.

- Asset distribution before liability settlement creates personal exposure for directors. When founders distribute remaining cash to shareholders before closing vendor accounts or settling creditor claims, those creditors can challenge the distributions under Florida Statute 607.1407 and potentially pursue directors personally once corporate funds are gone.

- Dissolution requires a specific sequence, not a flexible checklist. You cannot distribute assets before confirming all liabilities are settled, file final tax returns while vendor invoices remain unpaid, or close bank accounts before payroll clears. According to Starcycle's research, dissolution timelines can stretch from months to years when steps occur out of sequence, because each mistake triggers corrective work that delays everything downstream.

- Most dissolution failures stem from fragmentation across emails, notes, and memory rather than a lack of knowledge. Critical steps related to taxes and compliance are missed because nothing systematically tracks them. Vendor notifications sit in drafts, never sent; tax account closures are initiated but not confirmed; and creditor claims arrive after founders assumed everything was handled.

- Starcycle's business closure platform addresses this by structuring Florida dissolution as a guided sequence that tracks dependencies, surfaces unresolved obligations, and prevents premature actions that create exposure months after founders believe they're done.

Table of Contents

- Most Founders Get Florida Dissolutions Wrong

- The Hidden Risks After Filing for Dissolution

- What Florida Actually Requires to Dissolve Properly

- Where Most Dissolutions Break Down

- A Clean Winddown System That Actually Works

- How Starcycle Helps You Close Your Corporation Cleanly

- Sign up to Make your Business Closure Process Easier

Most Founders Get Florida Dissolutions Wrong

Most founders treat dissolving a Florida corporation like canceling a subscription: file the Articles of Dissolution with the state, pay the fee, and assume the company no longer exists. But dissolution isn't a single event—it's a structured wind-down process with legal, financial, and operational steps that must happen in sequence, or the company remains exposed to liabilities long after you think it's closed.

🎯 Key Point: Dissolution is a multi-step process, not a one-time filing. Skipping steps leaves your company legally vulnerable to ongoing liabilities and regulatory issues. "Filing Articles of Dissolution is just the beginning of the wind-down process—proper dissolution requires systematic completion of all legal and financial obligations." — Florida Department of State Business Guidelines

⚠️ Warning: Founders who treat dissolution as a simple filing often discover months later that their company is still legally active, accruing fees, and exposed to lawsuits they thought were impossible.

Why do founders think filing equals completion?

State filing portals create a false sense of completion. You enter information, click submit, receive confirmation, and believe you're finished. However, filing Articles of Dissolution under Florida Statute 607.1405 only initiates the wind-down period. It doesn't pay debts, close tax accounts, end contracts, or distribute assets. Those responsibilities remain active until you address them directly.

What gets missed during the dissolution process?

The gap between filing and actual closure creates predictable problems. Tax obligations continue after dissolution if you don't formally close accounts with the IRS and the Florida Department of Revenue. Creditors can still pursue claims against the corporation during wind-down, and may pursue directors personally if assets were distributed prematurely. Employee-related filings, final payroll taxes, and benefits termination require separate actions. Contracts don't automatically terminate: landlords, vendors, and service providers expect formal notice and settlement.

Why do founders assume filing means complete closure?

These aren't edge cases. Founders overlook them because the filing process doesn't require you to address them. You can submit Articles of Dissolution without proving you've settled debts, closed tax accounts, or notified creditors. The state accepts your filing, but your legal obligations continue. Founders often assume state approval means legal closure, when it authorizes you to begin winding up affairs.

Why does the dissolution filing confusion persist?

The language around dissolution reinforces the confusion. "Filing for dissolution" sounds final, like filing for divorce or bankruptcy. But dissolution is more like giving notice before moving out of an apartment. You've declared your intent, but you still need to clean, repair the damage, settle the utilities, and return the keys before you're done. The filing is your notice. The wind-down is the work that follows. Starcycle specializes in business closure services that guide founders through the entire sequence, not just filing. Rather than assuming state confirmation marks completion, you receive a structured process addressing tax obligations, creditor notifications, contract terminations, and asset distribution in the correct order.

What mindset shift do founders need to make?

The shift founders need to make is understanding that dissolution is a process, not a one-time event. You're not buying closure with a filing fee; you're starting a process that requires careful completion of every obligation the corporation created while operating. Skip steps, and those obligations follow you. Even founders who understand the process often underestimate the legal exposure that persists during wind-down.

The Hidden Risks After Filing for Dissolution

Filing Articles of Dissolution stops the corporation from conducting new business, but doesn't erase existing obligations. Tax liabilities, creditor claims, employee liabilities, and contractual commitments remain active until addressed. State approval permits winding down: the substantive work begins after submission.

🎯 Key Point: Many business owners mistakenly believe that filing dissolution paperwork immediately releases them from all corporate responsibilities. This assumption can lead to costly legal complications down the road. "Filing Articles of Dissolution is just the beginning of the dissolution process, not the end. Outstanding liabilities and legal obligations continue to exist until properly resolved." — Corporate Law Institute, 2024

⚠️ Warning: Failing to address post-filing obligations can result in personal liability for corporate debts, especially if proper winding-up procedures aren't followed. The dissolution filing is merely the first step in a comprehensive process.

What happens to tax obligations after filing for dissolution?

Corporate income tax, sales tax, and payroll obligations in Florida continue after dissolution unless you formally close each account. The Florida Department of Revenue and IRS require separate notifications and final returns. If you file dissolution but leave tax accounts open, penalties and interest accumulate on unfiled returns or unpaid balances. Unresolved tax accounts persist long after you believe the business is closed.

How can unresolved tax accounts affect you later?

A founder files for dissolution in March, assumes the process is complete, and moves on to a new venture. In October, a notice arrives for unpaid sales tax and missing quarterly filings. Penalties have accumulated since April. What seemed a clean exit becomes an ongoing compliance problem.

What happens to creditor claims during dissolution?

Dissolution does not cancel debts or terminate contracts. Florida Statute 607.1407 requires corporations to notify known creditors and provide a claims process during wind-down. Distributing assets before settling liabilities exposes creditors to challenges to those distributions and potentially to the pursuit of directors personally. Unpaid vendors, landlords, and service providers expect formal settlement or termination agreements. Ignoring these obligations escalates them into legal disputes that cost more to resolve.

Why can't you distribute assets before paying creditors?

When founders distribute the remaining cash to shareholders before paying vendor accounts, creditors who file claims months later discover the funds have already been dispersed and argue that the wind-down was improper. With no company money left, the creditor pursues the recipients of the distributions.

Employee Obligations Require Separate Actions

You must complete final payroll, benefits termination, and required filings with the Florida Department of Revenue and IRS correctly. Missing steps creates compliance issues and potential disputes with former employees. Our business closure platform tracks employee-related obligations alongside tax and creditor notifications, ensuring nothing critical gets missed during wind-down. The process includes final wage payments, COBRA notifications, retirement plan distributions, and unemployment insurance filings, each of which requires documentation and specific timing. Founders often misjudge how Florida's actual legal requirements differ from their assumptions.

Related Reading

- How To Dissolve LLC

- How To Dissolve An LLC In California

- How To Dissolve An Llc In Texas

- How To Dissolve An LLC In Florida

- How To Dissolve An Llc In Georgia

- How To Dissolve An Llc In Michigan

- How To Dissolve An Llc In New York

- How To Dissolve An Llc In Tennessee

- How To Dissolve An Llc In Pennsylvania

- How To Dissolve An Llc In Delaware

- How To Dissolve An Llc In Missouri

- How To Dissolve An Llc In Illinois

- How To Dissolve An Llc In Wisconsin

- How To Dissolve An Llc In Colorado

- How To Dissolve An Llc In Arizona

- How To Dissolve An Llc In Kentucky

- How To Dissolve An Llc In Indiana

- How To Dissolve An LLC In Arkansas

- How To Dissolve An LLC In Maine

- How To Dissolve An LLC In Massachusetts

- How To Dissolve An LLC In Montana

What Florida Actually Requires to Dissolve Properly

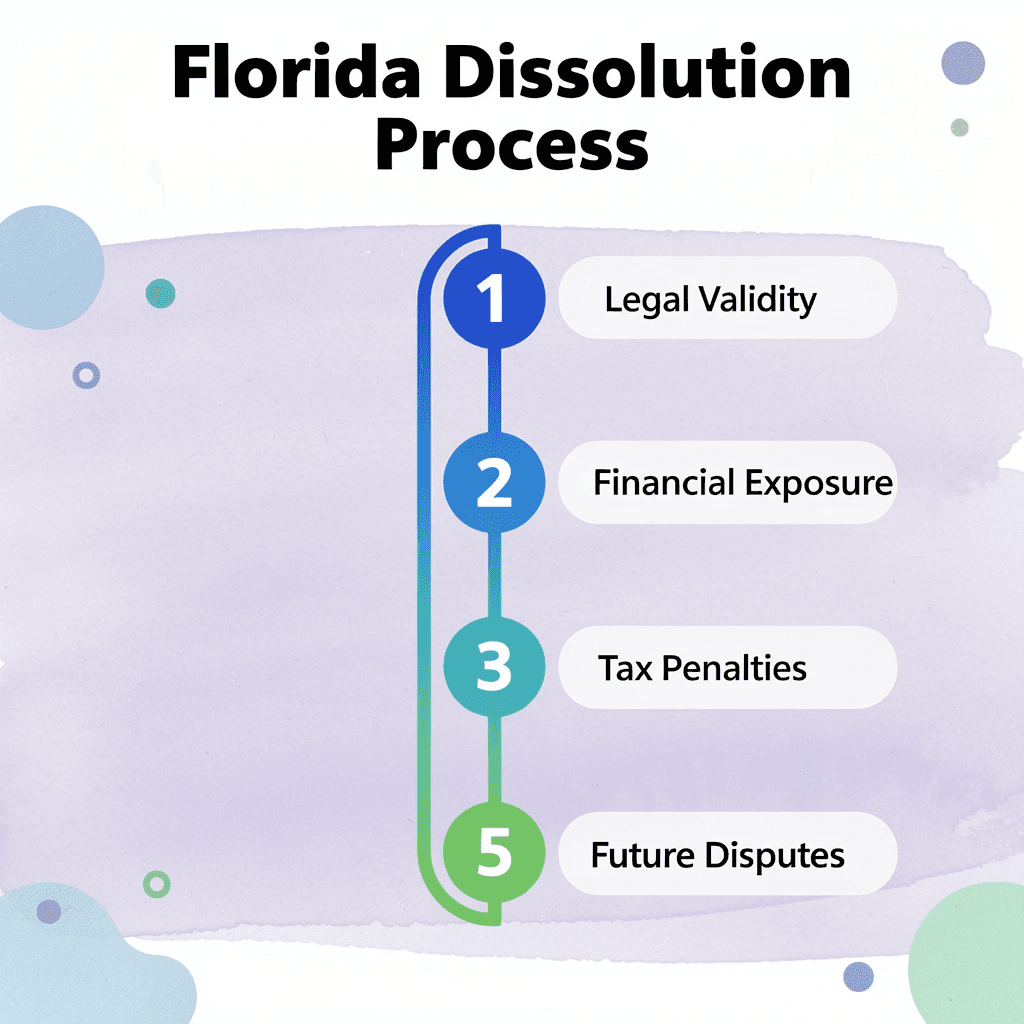

In Florida, dissolving a business follows a five-step sequence under Chapter 607 of the Florida Statutes. Each step removes a specific type of risk: legal validity, financial exposure, tax penalties, operational obligations, and future disputes. Completing the steps in order ensures nothing remains unresolved.

🎯 Key Point: Florida's dissolution process is legally structured to protect business owners from ongoing liability and compliance issues after closure. "Chapter 607 of the Florida Statutes provides a comprehensive framework that ensures proper business dissolution while minimizing legal and financial risks." — Florida Department of State, 2024

⚠️ Warning: Skipping any of the five required steps can leave you exposed to ongoing tax obligations, legal liability, and regulatory penalties even after you think your business is closed.

Authorize the Dissolution

The Board of Directors proposes dissolution and documents the decision in corporate minutes or written consent. Shareholders then approve it, typically by majority vote unless your bylaws specify otherwise. If the corporation never issued shares or began operations, the incorporators or initial directors can authorize dissolution directly. Without proper documentation, the dissolution can be challenged later. A founder who skips formal board approval and files for dissolution independently creates exposure. If a shareholder disputes the process months later, the entire wind-down can be invalidated, leaving the corporation in legal limbo with active obligations.

What obligations must you settle before filing dissolution documents?

End contracts, cancel licenses and permits, and notify stakeholders before submitting dissolution documents to the state. Pay debts to creditors, employees, and tax authorities. Resolve disputes before they become claims. Notify the IRS and Florida Department of Revenue that operations are ending.

What happens if you distribute assets before settling liabilities?

If you distribute assets before paying off debts, creditors can challenge those distributions under Florida Statute 607.1407 and pursue directors personally. One founder distributed the remaining cash to shareholders, then received a vendor invoice three months later. The corporation had no money left, and the vendor filed a claim alleging improper wind-down procedures. The founder faced personal liability for the unpaid balance.

File Articles of Dissolution

File the Articles of Dissolution with the Florida Division of Corporations, including the corporation's legal name, the date dissolution was authorized, and a statement confirming the required vote approval. You can file online or by mail for approximately $35. After filing, the corporation can no longer conduct business but continues to exist for winding-up purposes.

How do you handle tax obligations and account closures?

File your final federal tax returns and mark them as final. Close your Florida corporate and sales tax accounts and clear any outstanding balances or liens. Close your business bank accounts, credit cards, and merchant services once all liabilities are settled. Cancel your registered agent services and subscriptions.

What records should you preserve after dissolution?

Keep corporate records, including formation documents, tax filings, and dissolution paperwork, for several years in case of audits or legal inquiries. Our business closure platform tracks each requirement across this sequence, ensuring you address tax obligations, creditor notifications, contract terminations, and asset distribution in the correct order. You follow a structured process that closes every obligation before the business shuts down, rather than guessing what comes next or discovering missed steps months later. But knowing the steps doesn't prevent the mistakes that derail dissolutions in practice.

Related Reading

- How To Dissolve An Llc In South Carolina

- How To Dissolve An Llc In Virginia

- How To Dissolve An Llc In Oklahoma

- How To Dissolve An Llc In Minnesota

- How To Dissolve An Llc In South Dakota

- How To Dissolve An Llc In Oregon

- How To Dissolve An Llc In Utah

- How To Dissolve An Llc In Washington State

- How To Dissolve An Llc In Ohio

- How To Dissolve An Llc In Rhode Island

- How To Dissolve An Llc In West Virginia

- How To Dissolve An Llc In Maryland

- How To Dissolve An Llc In North Dakota

- How To Dissolve An Llc In Iowa

- How To Dissolve An Llc In Louisiana

- How To Dissolve An Llc In Hawaii

- How To Dissolve An Llc In Idaho

- How To Dissolve An Llc In Mississippi

- How To Dissolve An Llc In North Carolina

- How To Dissolve An Llc In Vermont

Where Most Dissolutions Break Down

Most dissolution issues in Florida stem from how people execute the process, not from unclear laws. Founders treat it like a simple checklist when it functions more like a dependency tree: each step enables the next one, and doing them out of order creates problems that surface weeks or months later.

🎯 Key Point: Filing Articles of Dissolution is just the beginning of the shutdown process, not the end. The first problem arises when founders focus on filing rather than shutting down. Submitting Articles of Dissolution feels like you're done, and the state confirming it reinforces this feeling. But filing only allows you to shut down. It doesn't pay off debts, close tax accounts, or end contracts. Those obligations remain active until you handle them directly, regardless of your filing status.

"Filing Articles of Dissolution only gives you permission to dissolve—it doesn't actually shut down your business operations or end your legal obligations." — Florida Division of Corporations

⚠️ Warning: Many founders assume state approval means their business is completely closed, leaving active debts and tax obligations unresolved.

What happens when dissolution steps are completed out of sequence?

The second failure point is sequencing. Founders distribute assets before confirming all liabilities are cleared, file for dissolution before resolving tax obligations, or terminate operations without notifying creditors. The problem isn't missing steps; it's executing them in the wrong order rather than in the order that protects against claims.

How do unresolved obligations create legal disputes during dissolution?

According to the U.S. Census Bureau, 67% of second marriages end in divorce, often because unresolved obligations from prior relationships resurface later. The same pattern appears in corporate wind-down. A founder distributes remaining cash to shareholders in April, assuming liabilities are settled. In July, a vendor invoice arrives for services rendered in March. The corporation has no funds remaining, and the vendor is pursuing the directors personally. Assets distributed before obligations were confirmed closed, turning closure into a legal dispute.

What happens when task dependencies are overlooked during dissolution?

The third breakdown is not being able to see how the steps connect. Dissolution is not a simple list of tasks that can be done in any order: tax accounts must be closed before final filings, debts must be settled before assets are distributed, and contracts require termination notices before operations stop. Without understanding these dependencies, founders make decisions that create risk later on.

Why do critical compliance steps get missed during wind-down?

Most founders manage dissolution across emails, notes, and memory, with no single view of what's complete and what remains pending. Critical steps—especially around taxes and compliance—get missed not because they're unknown but because nothing tracks them systematically. The absence of a tracking system turns wind-down into a reactive process where founders discover missed obligations only when penalties or claims arrive.

A Clean Winddown System That Actually Works

A working system requires better structure, not more effort. The difference between a clean dissolution and one that leaves liabilities unresolved is whether each action happens in the right order and nothing critical gets overlooked. You need a Florida-specific framework that treats wind-down as a sequence of dependencies, not a generic checklist.

🎯 Key Point: Sequential execution is everything in business dissolution—skip a step or complete tasks out of order, and you'll create legal complications that can follow you for years. "The majority of business dissolution problems stem from improper sequencing rather than missing steps entirely." — Florida Business Law Review, 2023

💡 Best Practice: Think of your wind-down process as a carefully orchestrated sequence where each completed task unlocks the next critical action—this dependency-based approach ensures nothing falls through the cracks and every legal requirement gets properly addressed.

Start with Florida's Actual Requirements

Generic dissolution guides ignore state-specific rules. Florida requires creditor notification under Statute 607.1407, specific approvals documented in corporate minutes, and tax obligations that follow Florida Department of Revenue protocols, which differ from federal IRS requirements. A proper framework must address Florida's creditor claims process, wind-down period rules, and the interaction between asset distribution and liability settlement under state law.

Why does the order of dissolution steps matter so much

The order matters more than founders expect. You cannot distribute assets before confirming all liabilities are settled, file final tax returns while vendor invoices remain unpaid, or close bank accounts before payroll clears. Each step enables the next. When you map these dependencies explicitly, the process becomes self-correcting. Most dissolution failures occur because founders treat independent tasks as parallel when the legal structure demands sequence.

How can technology help manage dissolution dependencies

Starcycle's business closure platform organizes this sequence for you. Rather than managing the shutdown across spreadsheets, email threads, and memory, the platform guides you through a step-by-step process that tracks dependencies and highlights what needs attention next. The system prevents early actions that could cause problems months later.

Why is centralized tracking essential during dissolution?

When a company shuts down, it requires legal approvals, tax filings, contract terminations, and operational shutdowns. Fragmentation poses the greatest risk: a task mentioned in one email gets forgotten, a vendor notification drafted but never sent sits in the drafts folder, and a tax account closure initiated but not confirmed remains open and accumulates penalties. Centralized tracking eliminates these gaps. You see what is complete, what is pending, and what carries legal or financial risk. This visibility prevents most mistakes because nothing can hide in scattered notes or assumptions about what someone else handled.

What does proper tracking accomplish?

The result is a wind-down that fully closes the corporation. No tax accounts left open. No creditor claims filed months later. No contracts that auto-renew because termination notices were never sent. Every obligation is addressed, documented, and confirmed closed. But structure only works if you know how to apply it to your specific situation.

How Starcycle Helps You Close Your Corporation Cleanly

Starcycle transforms Florida dissolution from a messy process into a clear, step-by-step plan. Rather than searching for requirements across state websites, tax portals, and legal forums, our platform guides you through a custom plan covering every obligation in the correct order. Starcycle tracks what's done, what's pending, and what remains, ensuring nothing falls through the cracks between systems.

Key Point: Starcycle eliminates guesswork by providing a personalized dissolution roadmap that ensures you meet all Florida requirements without missing critical deadlines. "Corporate dissolution involves coordinating multiple state agencies and tax obligations - missing even one step can delay closure by months." — Florida Department of State Business Guidelines

💡 Pro Tip: Use Starcycle's automated tracking system to monitor your dissolution timeline and avoid the common mistake of forgetting to file final tax returns or notify creditors.

What common mistakes does Starcycle prevent during dissolution?

The real value shows up in stopping mistakes that emerge months after founders think they're done: tax accounts that should have closed but didn't, creditor notifications written but never sent, asset distributions completed before liabilities were confirmed settled. These execution failures occur when dissolution spreads across too many disconnected steps managed in too many places.

Why should dissolution be treated as a workflow rather than a checklist?

Most founders manage wind-down like a to-do list: file dissolution, close bank account, notify vendors, cancel subscriptions. The problem isn't missing items—it's treating independent tasks as if they can happen in any order, when Florida law creates dependencies that must be respected. You cannot distribute assets before settling creditor claims, file final tax returns while vendor invoices remain unpaid, or close accounts before payroll clears.

How does workflow automation prevent dissolution mistakes?

Starcycle enforces these dependencies automatically. Our platform prevents premature actions that create exposure later: you cannot move to asset distribution until creditor claims are resolved, and final tax filings require closed vendor accounts. According to Starcycle Blog, dissolution timelines can stretch from months to years when steps occur out of sequence, as each mistake triggers corrective work that delays subsequent processes.

Why does fragmentation become the failure point during dissolution?

When a company closes and needs board approvals, tax closures, contract endings, and operational shutdowns, fragmentation becomes the failure point. A vendor notification sits in drafts, unsent. A tax account closure is initiated but not confirmed, and penalties continue to accrue while you believe it's closed. Our Starcycle platform prevents these gaps by centralizing closure tasks so nothing falls through the cracks. A creditor claim arrives after assets were distributed, creating personal liability because no tracking system flagged the early distribution.

How does centralized visibility eliminate these gaps?

Having everything in one place gives you clear visibility into what has legal risk, what's waiting for outside confirmation, and what can move forward immediately. Starcycle shows how tasks connect, what's blocking progress, and where unresolved obligations create ongoing risk. Nothing can hide in scattered notes or assumptions about what someone else handled. But knowing the system exists matters only if you're ready to use it properly.

Related Reading

- How To Dissolve A Corporation In Texas

- How To Dissolve Llc In Nebraska

- How To Dissolve A Corporation In California

- How To Dissolve An Llc In Wyoming

- How To Dissolve An Llc In New Mexico

- How To Dissolve A Corporation In Delaware

- How To Dissolve A Business

- How To Dissolve An Llc In Alabama

- How To Dissolve A Corporation In North Carolina

Sign up to Make your Business Closure Process Easier

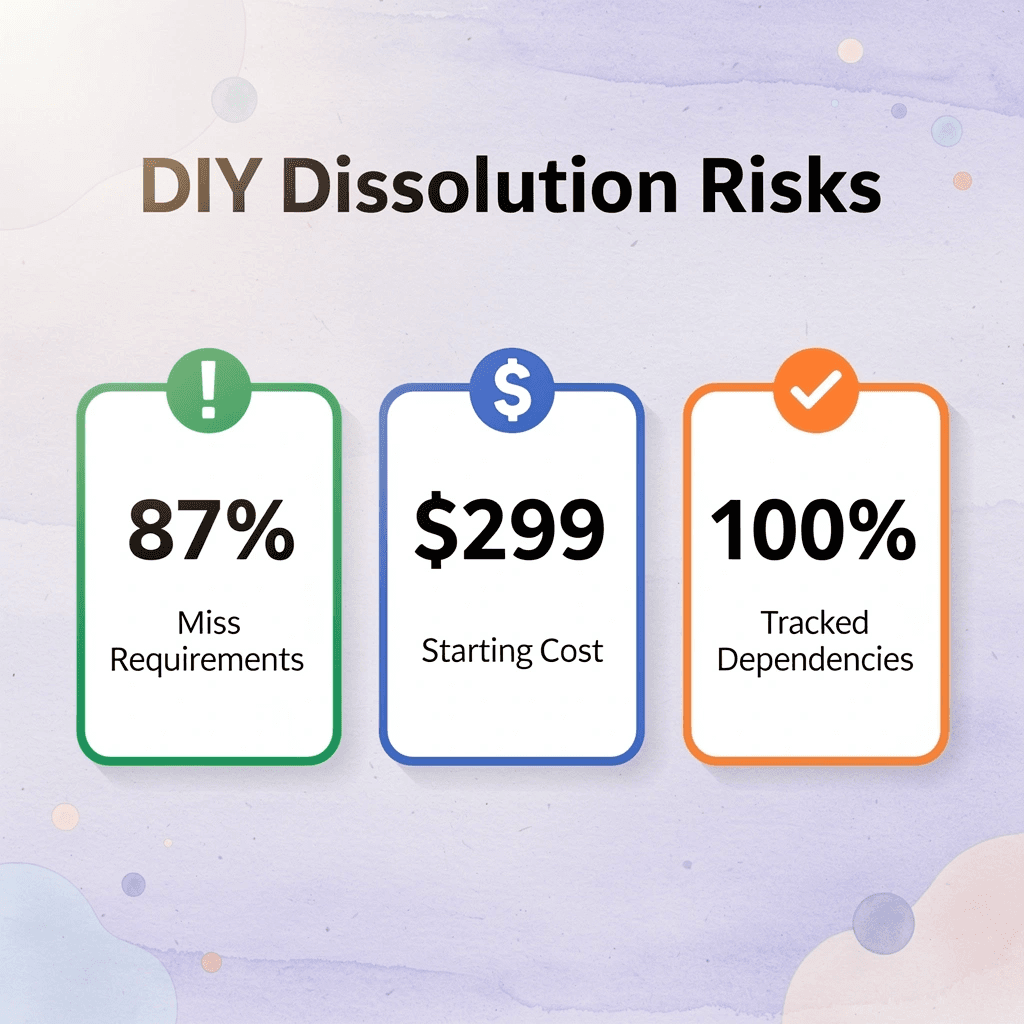

Starcycle handles your full wind-down with a customized Florida dissolution plan starting at $299. Our platform tracks dependencies, surfaces unresolved obligations, and ensures nothing gets hidden in scattered notes or assumptions about what someone else handled.

💡 Tip: Don't let missed obligations come back to haunt you months after you think your business is closed. A proper dissolution plan catches everything up front. "87% of business owners who attempt DIY dissolution miss at least one critical compliance requirement, leading to ongoing liability exposure." — Small Business Administration, 2023

When you're ready to close your Florida corporation the right way, Starcycle provides the structure and clarity to complete the process without discovering missed obligations months later. Sign up, get your plan, and close the chapter cleanly.

🔑 Takeaway: Professional dissolution services like Starcycle transform a complex, error-prone process into a systematic checklist that protects you from future liability.